|

市場調査レポート

商品コード

1755208

溶接消耗品の市場機会と促進要因、業界動向分析、2025年~2034年予測Welding Consumables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 溶接消耗品の市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年05月27日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

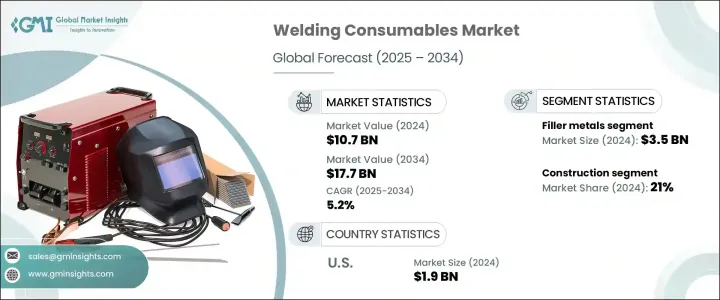

溶接消耗品の世界市場規模は、2024年に107億米ドルとなり、CAGR 5.2%で成長し、2034年には177億米ドルに達すると予測されています。

この成長を牽引しているのは、産業用途における自動化やロボット導入の増加に伴う、インフラや建設プロジェクトにおける溶接消耗品需要の増加です。さらに、環境に優しい溶接材料への嗜好の高まりや、新興市場における自動車セクターの拡大も市場成長に寄与しています。開発途上国では、都市化と可処分所得の増加により、インフラへの大規模な投資が見込まれ、溶接消耗品の需要に拍車がかかります。

これらの地域の産業部門が繁栄を続けるにつれて、溶接の必要性が高まり、市場に新たな機会が生まれます。より強く耐久性のある材料の開発など、溶接技術の進歩も市場の成長を支えています。特に自動車分野では、先進経済諸国と新興経済諸国の両方において、メーカーがよりカスタムメイドの製品を求めるようになり、溶接プロセスの適用が増加しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 107億米ドル |

| 予測金額 | 177億米ドル |

| CAGR | 5.2% |

フィラーメタルの2024年の市場シェアは35億米ドルと最も大きく、2025年から2034年にかけてCAGR 5.6%で成長すると予測されます。フィラーメタルの需要は、パイプライン敷設、重機械生産、海洋加工などの業界の進化するニーズに対応するため、メーカーが革新的な製品を導入するにつれて高まっています。これらの業界では、製品の耐久性と性能を向上させるために、より強度の高い材料を採用する傾向が強まっています。

建設分野は2024年に21%のシェアを占め、2025年から2034年にかけてCAGR 5.9%で成長すると予想されています。溶接は建設、特に構造用金属骨組みの製造において不可欠なプロセスです。大規模な建設プロジェクトや金属使用量の増加に伴い、溶接は建物やインフラの構造的完全性を確保する上で重要な役割を果たしています。この分野における溶接消耗品の需要は、建設業界全体の成長と密接に結びついており、溶接はプレハブでも現場での組み立て作業でも重要な役割を果たしています。

米国の溶接消耗品市場は77%のシェアを占め、2024年の市場規模は19億米ドルでした。インフラ整備の急増と製造業におけるロボット工学と自動化の導入が相まって、この市場の成長を後押ししています。ロボット工学に加え、協働溶接ロボット(cobot)は、人間の溶接工を補助するために製造施設で使用されることが増えており、溶接工程をより効率的で正確なものにしています。環境に優しい消耗品の需要や、新興地域における自動車セクターの拡大も、米国の市場成長に寄与しています。

溶接消耗品世界市場で事業を展開する主要企業には、リンカーン・エレクトリック、パナソニック、ESAB、D&H Secheron、ミラー・エレクトリック、神戸製鋼所、現代ウェルディング、Ador Welding、Hobart Welding Products、Berkenhoff、EWM、Welding Alloys、Diffusion Engineers、Hilco Welding、Nouveauxなどがあります。溶接消耗品市場での地位を強化するため、各社は機械的・化学的特性を強化した新しい溶加材の開発など、製品提供における技術的進歩に注力しています。また、製造業における持続可能な慣行に対する需要の高まりに対応するため、環境に優しいソリューションを重視しています。加えて、メーカーは、特に自動車や建設分野で高まるカスタマイズ・ソリューションのニーズを満たす製品を開発するため、研究開発に多額の投資を行っています。新興市場でのプレゼンスを拡大し、自動化とロボット工学に注力することも重要な戦略であり、企業は人件費を削減しながら生産効率を向上させることができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- サプライヤーの情勢

- 主なニュースと取り組み

- 規制情勢

- 価格動向分析

- 影響要因

- 促進要因

- インフラと建設プロジェクトの急増

- 自動車および製造業の成長

- 業界の潜在的リスク&課題

- 原材料価格の変動

- 地政学的および貿易障壁

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 電極

- シールドメタルアーク溶接電極

- ガスメタルアーク溶接電極

- その他

- フラックス

- サブマージアーク溶接フラックス

- 酸素燃料溶接フラックス

- その他(ろう付け用フラックス等)

- ガス

- シールドガス

- 補助ガス

- その他

- フィラーメタル

- 単線

- フラックス入りワイヤ

- 金属芯線

- 溶接棒

- その他(特殊フィラー金属など)

- その他

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 軟鋼

- ステンレス鋼

- アルミニウム

- ニッケル合金

- 銅合金

- その他(コバルト合金等)

第7章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 建設

- 自動車

- エネルギー

- 造船

- 航空宇宙

- 重工業

- その他(防衛など)

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Ador Welding

- Berkenhoff

- D&H Secheron

- Diffusion Engineers

- ESAB

- EWM

- Hilco Welding

- Hobart Welding Products

- Hyundai Welding

- Kobe Steel

- Lincoln Electric

- Miller Electric

- Nouveaux

- Panasonic

- Welding Alloys

The Global Welding Consumables Market was valued at USD 10.7 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 17.7 billion by 2034. This growth is driven by the increasing demand for welding consumables in infrastructure and construction projects with the rising adoption of automation and robotics in industrial applications. Additionally, the growing preference for eco-friendly welding materials and the expansion of the automotive sector in emerging markets are further contributing to market growth. In developing nations, urbanization and rising disposable incomes are expected to lead to significant investments in infrastructure, which in turn will fuel the demand for welding consumables.

As the industrial sector in these regions continues to thrive, the need for welding will grow, creating new opportunities in the market. Advances in welding technology, such as the development of stronger, more durable materials, are also supporting market growth. The automotive sector, particularly in both developed and emerging economies, is seeing a rise in the application of welding processes as manufacturers demand more custom-made products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.7 Billion |

| Forecast Value | $17.7 Billion |

| CAGR | 5.2% |

Filler metals held the largest market share in 2024, generating USD 3.5 billion, and is expected to grow at a CAGR of 5.6% between 2025 and 2034. The demand for filler metals is rising as manufacturers introduce innovative products to meet the evolving needs of industries like pipeline installation, heavy machinery production, and offshore fabrication. These industries are increasingly turning to higher-strength materials to improve the durability and performance of their products.

The construction segment held a 21% share in 2024 and is expected to grow at a CAGR of 5.9% from 2025 to 2034. Welding is an essential process in construction, especially in the fabrication of structural metal frameworks. With large-scale construction projects and increasing metal usage, welding plays a critical role in ensuring the structural integrity of buildings and infrastructure. The demand for welding consumables in this sector is closely tied to the growth of the overall construction industry, with welding playing a significant role in both prefabricated and on-site assembly work.

United States Welding Consumables Market held a 77% share and was valued at USD 1.9 billion in 2024. The surge in infrastructure development, coupled with the adoption of robotics and automation in manufacturing, is propelling the growth of this market. In addition to robotics, collaborative welding robots (cobots) are increasingly being used in manufacturing facilities to assist human welders, making welding processes more efficient and precise. The demand for eco-friendly consumables and the automotive sector's expansion in emerging regions are also contributing to market growth in the U.S.

Key players operating in the Global Welding Consumables Market include Lincoln Electric, Panasonic, ESAB, D&H Secheron, Miller Electric, Kobe Steel, Hyundai Welding, Ador Welding, Hobart Welding Products, Berkenhoff, EWM, Welding Alloys, Diffusion Engineers, Hilco Welding, and Nouveaux. To strengthen their position in the welding consumables market, companies are focusing on technological advancements in their product offerings, such as the development of new filler metals with enhanced mechanical and chemical properties. They are also emphasizing eco-friendly solutions to cater to the growing demand for sustainable practices in manufacturing. Additionally, manufacturers are investing heavily in R&D to develop products that meet the increasing need for customized solutions, especially in the automotive and construction sectors. Expanding their presence in emerging markets and focusing on automation and robotics are also key strategies, enabling companies to improve production efficiency while reducing labor costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Pricing trend analysis

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Surge in infrastructure and construction projects

- 3.6.1.2 Growth in automotive and manufacturing sectors

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Fluctuating raw material prices

- 3.6.2.2 Geopolitical and trade barriers

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Billion, Million Units)

- 5.1 Key trends

- 5.2 Electrodes

- 5.2.1 Shielded metal arc welding electrodes

- 5.2.2 Gas metal arc welding electrodes

- 5.2.3 Others

- 5.3 Fluxes

- 5.3.1 Submerged arc welding flux

- 5.3.2 Oxy-fuel welding flux

- 5.3.3 Others (brazing flux etc.)

- 5.4 Gases

- 5.4.1 Shielding Gases

- 5.4.2 Backing Gases

- 5.4.3 Others

- 5.5 Filler metals

- 5.5.1 Solid wire

- 5.5.2 flux-cored wire

- 5.5.3 Metal cored wire

- 5.5.4 Welding rods

- 5.5.5 Others (specialty filler metals etc.)

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Material Type, 2021 - 2034 ($Billion, Million Units)

- 6.1 Key trends

- 6.2 Mild steel

- 6.3 Stainless steel

- 6.4 Aluminum

- 6.5 Nickel alloys

- 6.6 Copper alloys

- 6.7 Others (cobalt alloys etc.)

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Billion, Million Units)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Automobile

- 7.4 Energy

- 7.5 Shipbuilding

- 7.6 Aerospace

- 7.7 Heavy engineering

- 7.8 Others (defense etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Million Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Ador Welding

- 10.2 Berkenhoff

- 10.3 D&H Secheron

- 10.4 Diffusion Engineers

- 10.5 ESAB

- 10.6 EWM

- 10.7 Hilco Welding

- 10.8 Hobart Welding Products

- 10.9 Hyundai Welding

- 10.10 Kobe Steel

- 10.11 Lincoln Electric

- 10.12 Miller Electric

- 10.13 Nouveaux

- 10.14 Panasonic

- 10.15 Welding Alloys