|

市場調査レポート

商品コード

1755207

物流・サプライチェーンにおけるAIの市場機会、成長促進要因、産業動向分析、2025年~2034年予測AI in Logistics and Supply Chain Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 物流・サプライチェーンにおけるAIの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月20日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

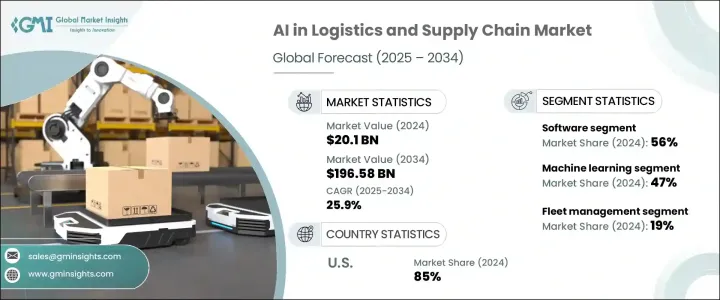

物流・サプライチェーンにおけるAIの世界市場規模は2024年に201億米ドルとなり、リアルタイムのサプライチェーン可視化、最適化されたルートプランニング、正確な需要推計・予測、倉庫における自動化のニーズの高まりにより、CAGR 25.9%で成長し、2034年には1,965億8,000万米ドルに達すると推定・予測されています。

企業は、意思決定プロセスを強化し、運用コストを削減し、複雑な物流ネットワークを管理するために、ますますAIを業務に取り入れています。予測分析、ロボットによるプロセス自動化、自律走行車などのAI対応ソリューションは、従来のサプライチェーンをインテリジェントで適応可能なエコシステムに変えつつあります。

世界のサプライチェーンの複雑化により、予測分析とリアルタイム・データのニーズが生まれ、企業はセンサー、GPS、企業資源計画(ERP)システムからの膨大なデータを分析して在庫管理を最適化し、コストを削減できるようになりました。AIは、企業が市場環境の変化に迅速に適応し、混乱を防ぎ、顧客満足度を向上させるのに役立ちます。eコマースとオムニチャネル小売の拡大は、スピード、正確性、柔軟性の必要性をさらに強調しており、AI技術は注文処理の合理化、配送スケジュールの自動化、顧客行動の予測に役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 201億米ドル |

| 予測金額 | 1,965億8,000万米ドル |

| CAGR | 25.9% |

2024年には、ソフトウェア部門が56%のシェアで市場をリードし、2034年までのCAGRは26%で成長すると予測されます。ソフトウェアは、サプライチェーン全体のインテリジェントな意思決定、自動化、リアルタイムのデータ分析を強化するのに役立ちます。ルート最適化、需要予測、倉庫自動化を含むAI主導のソフトウェアソリューションは、業務を最適化し、コストを削減し、効率を高めるために物流プロバイダーによって広く採用されています。これらのソリューションは、計画の精度を高め、人的ミスを最小限に抑え、市場の変動に迅速に対応するための鍵となります。予測分析とリアルタイムの可視性の重視は、AIを搭載したソフトウェア・アプリケーションの需要拡大に大きく貢献しています。

機械学習(ML)セグメントは2024年に47%のシェアを占めました。膨大なデータセットを処理し、実用的な洞察をリアルタイムで生成するその能力は、IoTデバイス、GPSシステム、顧客とのやり取りから得られる構造化データおよび非構造化データの分析に不可欠です。MLアルゴリズムは、在庫管理を最適化し、需要パターンを明らかにし、オペレーションのボトルネックを解消することで、効率性と費用対効果を高める。これらのアルゴリズムは継続的に進化し、従来のシステムを凌駕する予測的洞察と自動化の機会を提供します。

米国の物流・サプライチェーン市場におけるAIのシェアは85%で、2024年には62億米ドルに達します。米国を拠点とする物流企業は、ルートの最適化、需要予測、倉庫の自動化、予知保全などのソリューションにAIをいち早く組み込んでいます。米国の主要企業の地位は、大手ハイテク企業やAIプロバイダーの存在によってさらに強化され、物流におけるAIの採用を加速させています。AIの研究開発に対する官民セクターの投資は、国家AIイニシアチブ法のような政府のイニシアティブと相まって、物流とサプライチェーンのランドスケープ全体でAI技術の採用をサポートしています。

物流・サプライチェーンにおけるAI市場における著名な企業には、Amazon Web Services、Oracle、Blue Yonder、SAP SE、FourKites、C3.ai、Google、Microsoft、IBM、Manhattan Associatesが含まれます。市場での地位を強化するため、各社は戦略的提携や買収に注力し、AI能力を強化し、サービス提供の幅を広げています。最先端技術を活用することで、これらの企業は機械学習、ロボット工学、自動化を物流やサプライチェーン業務に統合し、効率性の向上とコスト削減を図っています。多くの企業は、リアルタイム分析、ルート最適化、需要予測のためにAI主導のソフトウェア・ソリューションに投資し、急速に進化する市場で競争力を維持できるようにしています。さらに、AIソリューション・プロバイダーはeコマース分野への注力を強めており、消費者の期待の高まりに応えるため、迅速かつ柔軟で正確な配送システムを確保しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- テクノロジープロバイダー

- システムインテグレーターおよびコンサルティング会社

- 物流技術プロバイダー

- ハードウェアおよびロボット企業

- マネージドサービスプロバイダー(MSP)

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 他国による報復措置

- 業界への影響

- 主要原材料の価格変動

- サプライチェーンの再構築

- 提供コストの影響

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と提供戦略

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 価格動向s

- コスト内訳分析

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- リアルタイムのサプライチェーン可視化に対する需要の高まり

- eコマースとオムニチャネル小売業の成長

- 予測分析と機械学習の進歩

- スマート倉庫のためのIoTとAIの統合

- 自律走行車とドローンの導入

- 業界の潜在的リスク&課題

- 初期導入コストが高め

- データのプライバシーとセキュリティに関する懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- センサー

- ロボット(例:無人搬送車、ドローン)

- ソフトウェア

- 予測分析

- 輸送管理システム

- 在庫管理

- 倉庫管理

- サービス

- マネージドサービス

- 専門サービス

- 展開と統合

- コンサルティング

- サポートとメンテナンス

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 機械学習

- 自然言語処理(NLP)

- コンピュータービジョン

- コンテキストアウェアコンピューティング

- ロボティクス・プロセス・オートメーション(RPA)

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 車両管理

- サプライチェーン計画

- 在庫および倉庫管理

- 貨物仲介およびリスク管理

- 需要予測

- カスタマーサービス(チャットボット、バーチャルアシスタント)

- 注文処理とラストマイル配送

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 小売・eコマース

- 製造業

- 自動車

- 食品・飲料

- ヘルスケアと医薬品

- 運輸・物流

- エネルギー・公益事業

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Amazon Web Services

- Blue Yonder

- C3.ai

- ClearMetal

- Fetch Robotics

- FourKites

- GE Digital

- Honeywell International

- Infor

- Korber Supply Chain

- Llamasoft

- Manhattan Associates

- Microsoft Corporation

- NVIDIA Corporation

- SAP SE

- Siemens AG

- Zebra Technologies

The Global AI in Logistics and Supply Chain Market was valued at USD 20.1 billion in 2024 and is estimated to grow at a CAGR of 25.9% to reach USD 196.58 billion by 2034, driven by the increasing need for real-time supply chain visibility, optimized route planning, accurate demand forecasting, and automation in warehouses. Companies are increasingly incorporating AI into their operations to enhance decision-making processes, reduce operational costs, and manage complex logistics networks. AI-enabled solutions such as predictive analytics, robotic process automation, and autonomous vehicles are transforming traditional supply chains into intelligent, adaptable ecosystems.

The growing intricacy of global supply chains has created a need for predictive analytics and real-time data, allowing businesses to analyze massive amounts of data from sensors, GPS, and enterprise resource planning (ERP) systems to optimize inventory management and reduce costs. AI helps companies adapt quickly to shifts in market conditions, prevent disruptions, and improve customer satisfaction. The expansion of e-commerce and omnichannel retail further emphasizes the need for speed, accuracy, and flexibility, where AI technologies help streamline order processing, automate delivery schedules, and forecast customer behavior.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.1 Billion |

| Forecast Value | $196.58 Billion |

| CAGR | 25.9% |

In 2024, the software sector led the market with a share of 56%, anticipated to grow at a CAGR of 26% through 2034. Software helps in empowering intelligent decision-making, automation, and real-time data analysis throughout the supply chain. AI-driven software solutions, including route optimization, demand forecasting, and warehouse automation, are widely adopted by logistics providers to optimize operations, reduce costs, and enhance efficiency. These solutions are key to improving planning accuracy, minimizing human error, and quickly adjusting to market fluctuations. The emphasis on predictive analytics and real-time visibility significantly contributes to the growing demand for AI-powered software applications.

The machine learning (ML) segment held a 47% share in 2024. Its capability to process massive datasets and generate actionable insights in real time makes it essential for analyzing structured and unstructured data from IoT devices, GPS systems, and customer interactions. ML algorithms optimize inventory management, uncover demand patterns, and eliminate operational bottlenecks, thus enhancing efficiency and cost-effectiveness. These algorithms evolve continuously, providing predictive insights and automation opportunities that outperform traditional systems.

United States AI in the Logistics and Supply Chain Market held an 85% share and generated USD 6.2 billion in 2024 due to its advanced digital infrastructure and widespread adoption of emerging technologies. U.S.-based logistics firms are among the first to integrate AI for solutions such as route optimization, demand forecasting, warehouse automation, and predictive maintenance. The country's leading position is further bolstered by the presence of major tech companies and AI providers, accelerating AI adoption in logistics. Public and private sector investments in AI research and development, coupled with government initiatives like the National AI Initiative Act, support the adoption of AI technologies across the logistics and supply chain landscape.

Prominent players in the AI in Logistics and Supply Chain Market include Amazon Web Services, Oracle, Blue Yonder, SAP SE, FourKites, C3.ai, Google, Microsoft, IBM, and Manhattan Associates. To strengthen their market position, companies are focusing on strategic partnerships and acquisitions to enhance their AI capabilities and broaden service offerings. Leveraging cutting-edge technologies, these companies are integrating machine learning, robotics, and automation into logistics and supply chain operations to improve efficiency and reduce costs. Many firms invest in AI-driven software solutions for real-time analytics, route optimization, and demand forecasting, allowing them to stay competitive in a rapidly evolving market. Additionally, AI solution providers are increasing their focus on the e-commerce sector, ensuring quick, flexible, and accurate delivery systems to meet growing consumer expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 System integrators and consulting firms

- 3.2.3 Logistics technology providers

- 3.2.4 Hardware and robotics companies

- 3.2.5 Managed service providers (MSPs)

- 3.3 Profit margin analysis

- 3.4 Impact of Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Offering cost implications

- 3.4.3 Strategic industry responses

- 3.4.3.1 Supply chain reconfiguration

- 3.4.3.2 Pricing and Offering strategies

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Price trends

- 3.7 Cost breakdown analysis

- 3.8 Patent analysis

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rising demand for real-time supply chain visibility

- 3.11.1.2 Growth of e-commerce and omnichannel retailing

- 3.11.1.3 Advancements in predictive analytics and machine learning

- 3.11.1.4 Integration of IoT and AI for smart warehousing

- 3.11.1.5 Adoption of autonomous vehicles and drones

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High initial implementation costs

- 3.11.2.2 Data privacy and security concerns

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 Robots (e.g., automated guided vehicles, drones)

- 5.3 Software

- 5.3.1 Predictive analytics

- 5.3.2 Transportation management systems

- 5.3.3 Inventory management

- 5.3.4 Warehouse management

- 5.4 Services

- 5.4.1 Managed services

- 5.4.2 Professional services

- 5.4.2.1 Deployment & integration

- 5.4.2.2 Consulting

- 5.4.2.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Machine learning

- 6.3 Natural language processing (NLP)

- 6.4 Computer vision

- 6.5 Context-aware computing

- 6.6 Robotics process automation (RPA)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Fleet management

- 7.3 Supply chain planning

- 7.4 Inventory & warehouse management

- 7.5 Freight brokerage & risk management

- 7.6 Demand forecasting

- 7.7 Customer service (chatbots, virtual assistants)

- 7.8 Order fulfillment & last-mile delivery

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Retail & e-commerce

- 8.3 Manufacturing

- 8.4 Automotive

- 8.5 Food & beverage

- 8.6 Healthcare & pharmaceuticals

- 8.7 Transportation & logistics

- 8.8 Energy & utilities

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Amazon Web Services

- 10.2 Blue Yonder

- 10.3 C3.ai

- 10.4 ClearMetal

- 10.5 Fetch Robotics

- 10.6 FourKites

- 10.7 GE Digital

- 10.8 Google

- 10.9 Honeywell International

- 10.10 Infor

- 10.11 Korber Supply Chain

- 10.12 Llamasoft

- 10.13 Manhattan Associates

- 10.14 Microsoft Corporation

- 10.15 NVIDIA Corporation

- 10.16 SAP SE

- 10.17 Siemens AG

- 10.18 Zebra Technologies