|

市場調査レポート

商品コード

1755202

コンポスタブル包装フィルムの市場機会と促進要因、業界動向分析、2025年~2034年予測Compostable Packaging Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| コンポスタブル包装フィルムの市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年05月20日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

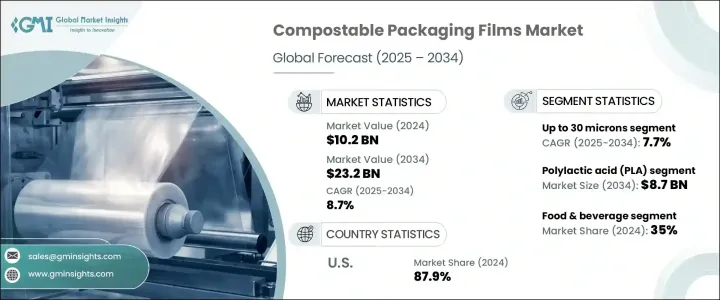

コンポスタブル包装フィルムの世界市場規模は、2024年には102億米ドルとなり、活況を呈するeコマース部門と飲食品産業の成長に牽引され、CAGR 8.7%で成長し、2034年には232億米ドルに達すると予測されています。

しかし、米国の前政権下でバイオポリマーと必須加工機器に関税が導入されたことで、コンポスタブル包装フィルムの現地メーカーにコスト圧力が生じた。これらの関税は、世界のサプライチェーンを混乱させ、投入コストを高騰させ、持続可能なパッケージング・ソリューションに投資するメーカーに不確実性をもたらしています。追加されたコスト負担は、特に輸入原料や製造技術に依存している中小企業にとって、堆肥化可能なフィルムの拡大を制限する可能性があります。さらに、他国からの報復関税は国際貿易をより困難にし、輸出機会を損ない、業界全体の競合力を低下させています。

eコマースの成長は、持続可能な包装の需要に大きな影響を与えています。オンラインで出荷される製品の量が増えているため、消費者の嗜好と規制基準の両方を満たす包装が必要とされているからです。堆肥化可能なフィルムは、軽量で柔軟性があり、生分解性があるため、eコマース・ロジスティクスで支持を集めています。コンポスタブル包装フィルム市場の開拓者は、eコマース分野に合わせた耐久性、軽量性、生分解性フィルムの開発に注力すべきです。これにより、消費者の需要を満たし、特にインドのような新興市場において持続可能なパッケージングに対する規制圧力の高まりに対応することができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 102億米ドル |

| 予測金額 | 232億米ドル |

| CAGR | 8.7% |

コンポスタブル包装フィルム市場は、厚さ別に30ミクロンまで、30~60ミクロン、60ミクロン以上の3セグメントに分類されます。30ミクロンまでのフィルム市場は、2034年までCAGR 7.7%で成長すると予測されています。これらの薄いフィルムは、ベーカリー製品、スナック菓子、ティーバッグなどの軽い食品の包装や、ラベルやオーバーラップの用途によく使われます。材料の使用量を最小限に抑えることができるため、コスト効率に優れ、賞味期限の短い製品では堆肥化可能な基準に適合します。

素材別に見ると、市場はポリ乳酸(PLA)、竹、ポリヒドロキシアルカノエート(PHA)、デンプン系フィルム、セルロース系フィルム、その他などのカテゴリーに分けられます。PLA市場は2034年までに87億米ドルに達すると予想されています。PLAベースのフィルムは、その優れた印刷適性、透明性、堆肥化性により、食品包装分野で特に人気があります。PLAフィルムは化石燃料ベースのプラスチックに代わる実行可能な代替品であり、既存の加工装置との互換性があるため、商業的な採用が急速に進んでいます。

米国のコンポスタブル包装フィルム2024年の同市場のシェアは87.9%であったが、これはプラスチック廃棄物の削減を目的とした強力な規制支援と、企業による持続可能性への取り組みの高まりによるものです。特にオーガニック食品業界や環境意識の高い消費者からの堆肥化可能フィルムへの需要が高まっており、これが家庭で堆肥化可能なパッケージング・ソリューションの技術革新を促進しています。開発企業は、商業的に実行可能な生分解性代替品を開発するため、材料技術者と積極的に協力しています。

世界のコンポスタブル包装フィルム市場の注目すべき企業は、BioBag International、BASF、Biome Bioplastics、Amtrex Nature Care、Baroda Rapidsなどです。市場ポジションを強化するため、各社は堆肥化可能な包装分野における技術力を強化するため、提携や買収などの戦略を採用しています。多くの企業は、持続可能なパッケージングに対する消費者の需要の高まりに対応した、高品質な生分解性フィルムの開発に注力しています。製造工程を改善し、堆肥化可能な材料の利用可能性を高めることで、企業は市場での競争力を獲得しようとしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 持続可能な包装に対する消費者の需要

- 食品・飲料業界でのアプリケーションの成長

- 使い捨てプラスチックに対する規制の強化

- オーガニック・ナチュラル製品ブランドからの需要

- eコマースと環境に優しい配送ニーズの拡大

- 業界の潜在的リスク&課題

- 高い生産コストと材料コスト

- 限られた産業用堆肥化インフラ

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- ポリ乳酸(PLA)

- 竹

- ポリヒドロキシアルカン酸(PHA)

- デンプン系フィルム

- セルロース系フィルム

- その他

第6章 市場推計・予測:厚さ別、2021年~2034年

- 主要動向

- 最大30ミクロン

- 30~60ミクロン

- 60ミクロン以上

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 食品・飲料

- ヘルスケアと医薬品

- 小売・eコマース

- ホーム&パーソナルケア

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Amtrex Nature Care

- Baroda Rapids

- BASF

- BI-AX International

- BioBag International

- Biome Bioplastics

- Cortec Corporation

- Easy Flux

- Futamura Group

- Novamont

- Plascon Group

- Polynova Industries

- Polystar Plastics

- Taghleef Industries

- TIPA

The Global Compostable Packaging Films Market was valued at USD 10.2 billion in 2024 and is estimated to grow at a CAGR of 8.7% to reach USD 23.2 billion by 2034 driven by the booming e-commerce sector and the growing food and beverage industry. However, the introduction of tariffs on biopolymers and essential processing equipment under the previous administration in the U.S. has created cost pressures for local manufacturers of compostable packaging films. These tariffs have disrupted global supply chains, inflated input costs, and generated uncertainty for those investing in sustainable packaging solutions. The added cost burden could limit the expansion of compostable films, especially for smaller businesses that rely on imported feedstock or manufacturing technologies. Additionally, retaliation tariffs from other countries have made international trade more difficult, hurting export opportunities and reducing the overall competitiveness of the industry.

E-commerce growth is significantly impacting the demand for sustainable packaging, as the increasing volume of products being shipped online requires packaging that meets both consumer preferences and regulatory standards. Compostable films are gaining traction in e-commerce logistics because they are lightweight, flexible, and biodegradable. Manufacturers in the compostable packaging films market should focus on developing durable, lightweight, and biodegradable films tailored to the e-commerce sector. This will help meet consumer demand and address the growing regulatory pressures for sustainable packaging, particularly in emerging markets like India.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.2 Billion |

| Forecast Value | $23.2 Billion |

| CAGR | 8.7% |

The compostable packaging films market is categorized by thickness into three segments: up to 30 microns, 30-60 microns, and above 60 microns. The market for films up to 30 microns is projected to grow at a CAGR of 7.7% through 2034. These thin films are commonly used for packaging light food items such as bakery products, snacks, or tea bags, as well as for label and overwrap applications. Their minimal material usage makes them cost-effective while ensuring compliance with compostable standards for short-shelf-life products.

By material, the market is divided into several categories, including polylactic acid (PLA), bamboo, polyhydroxyalkanoate (PHA), starch-based films, cellulose-based films, and others. The PLA market is expected to reach USD 8.7 billion by 2034. PLA-based films are particularly popular in the food packaging sector due to their excellent printability, transparency, and compostability. PLA films present a viable alternative to fossil-fuel-based plastics, and their compatibility with existing converting equipment facilitates their rapid commercial adoption.

U.S. Compostable Packaging Films Market held a share of 87.9% in 2024 attributed to strong regulatory support aimed at reducing plastic waste and the growing commitment to sustainability by businesses. There is a rising demand for compostable films, particularly from the organic food industry and environmentally conscious consumers, which is driving innovation in home-compostable packaging solutions. Companies are actively collaborating with material engineers to develop commercially viable biodegradable alternatives.

Notable players in the Global Compostable Packaging Films Market include BioBag International, BASF, Biome Bioplastics, Amtrex Nature Care, and Baroda Rapids. To strengthen their market position, companies are adopting strategies such as forming partnerships and acquisitions to enhance their technical capabilities in the compostable packaging sector. Many companies are focusing on the development of high-quality, biodegradable films that meet the growing consumer demand for sustainable packaging. By improving their manufacturing processes and increasing the availability of compostable materials, businesses are seeking to gain a competitive edge in the market.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Consumer demand for sustainable packaging

- 3.3.1.2 Growth in food & beverage industry applications

- 3.3.1.3 Increasing restrictions on single-use plastics

- 3.3.1.4 Demand from organic and natural product brands

- 3.3.1.5 Growth of e-commerce and eco-friendly shipping needs

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High production and material costs

- 3.3.2.2 Limited industrial composting infrastructure

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 Pestel analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Polylactic acid (PLA)

- 5.3 Bamboo

- 5.4 Polyhydroxyalkanoate (PHA)

- 5.5 Starch-based films

- 5.6 Cellulose-based films

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Thickness, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Up to 30 microns

- 6.3 30–60 microns

- 6.4 Above 60 microns

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Healthcare & pharmaceuticals

- 7.4 Retail & e-commerce

- 7.5 Home & personal care

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amtrex Nature Care

- 9.2 Baroda Rapids

- 9.3 BASF

- 9.4 BI-AX International

- 9.5 BioBag International

- 9.6 Biome Bioplastics

- 9.7 Cortec Corporation

- 9.8 Easy Flux

- 9.9 Futamura Group

- 9.10 Novamont

- 9.11 Plascon Group

- 9.12 Polynova Industries

- 9.13 Polystar Plastics

- 9.14 Taghleef Industries

- 9.15 TIPA