|

市場調査レポート

商品コード

1755192

気管内チューブの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Endotracheal Tube Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 気管内チューブの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月27日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

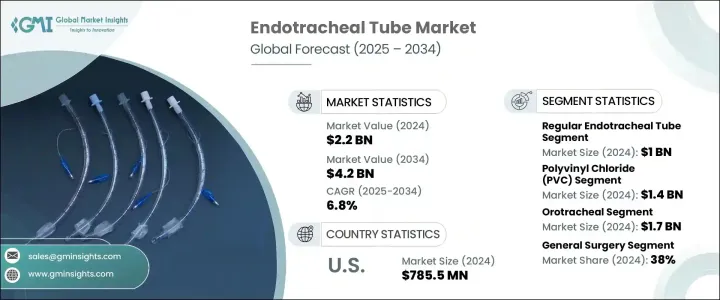

気管内チューブの世界市場は、2024年には22億米ドルと評価され、CAGR 6.8%で成長し、2034年には42億米ドルに達すると推定されています。

この市場拡大の背景には、挿管を必要とする手術件数の増加、ICU入室や重症患者の増加、新興地域におけるヘルスケアインフラの成長など、いくつかの要因があります。さらに、喘息や慢性閉塞性肺疾患(COPD)などの慢性呼吸器疾患の世界の増加、特に高齢者の増加が気管内チューブの需要に寄与しています。

メーカーは、人工呼吸器関連肺炎(VAP)のような合併症を減らすために、抗菌コーティング、新しいカフ設計、声門下吸引のような機能を組み込むことによって、これらの製品を強化しています。このような改良は患者に恩恵をもたらすだけでなく、世界中のヘルスケアセンターでこれらの機器の採用を促進し、市場の成長に寄与しています。気管内チューブは、手術や麻酔、クリティカルケアの際に、口や鼻から気管に通して気道を確保するために使用される柔軟なデバイスです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 22億米ドル |

| 予測金額 | 42億米ドル |

| CAGR | 6.8% |

ETTは、人工呼吸を可能にし、手技中の気道保護を維持するのに役立ちます。ETTの需要は、呼吸器疾患の有病率の上昇、使い捨てチューブへのシフト、ビデオ喉頭鏡検査などの先進的挿管手技の採用の増加により伸びています。さらに、救急医療や院外の環境では、抗菌剤や薬剤溶出コーティングを施したチューブの需要が高まっています。

2024年には、通常の気管内チューブセグメントは10億米ドルを生み出しました。これらのチューブは、先進的な代替品と比較して手ごろな価格であるため、特に資源が限られた環境において、日常的な外科手術や緊急処置に好ましい選択肢であり続けています。シンプルなデザインで使いやすく、ほとんどのヘルスケア専門家が効率的に操作できるよう訓練されているため、臨床現場で広く使用されています。

気管挿管チューブセグメントは、2024年に17億米ドルを生み出し、2034年にはCAGR 7%で成長すると予想されています。気管挿管は、その速さと実行のしやすさから、緊急時の気道管理として最も一般的な方法です。数分以内に気道を確保することが重要な外傷、心停止、重篤な状況において有用です。この方法は、鼻出血や副鼻腔感染などの合併症を回避でき、多くの成人患者にとってより安全であると考えられているため、経鼻気管挿管よりも好まれています。

米国気管内チューブ 2024年の市場規模は7億8,550万米ドル。COPD、肺炎、急性呼吸窮迫症候群(ARDS)などの呼吸器疾患の有病率の上昇が、同国における気管内チューブの需要を大幅に押し上げています。メディケア、メディケイド、民間保険会社が挿管や機械的換気手技をカバーする施策により、病院や手術センターは財政的制約に直面することなくETTを採用する可能性が高まっています。これらの償還施策は、ベストプラクティスを奨励し、気管内チューブの使用を増加させ、市場成長を促進する上で極めて重要な役割を果たしています。

世界の気管内チューブ市場の主要企業は以下の通り:Flexicare、Ambu、Fuji Systems、Medtronic、Medline、STERIMED、Teleflex、Romed HOLLAND、ANGIPLAST、Mercury Medical、INTERRACIAL、icumedical、VIGGOMEDICAL DEVICES、Wellead、TUORenなどです。市場での地位を強化するため、各社はいくつかの重要な戦略に注力しています。抗菌コーティングや声門下吸引などの先進的機能を開発し、患者の安全性を向上させ合併症を減らすことで、製品のイノベーションに投資しています。また、ヘルスケアプロバイダとの提携や新興市場での流通チャネルの拡大も、より多くの患者にリーチするために重要です。さらに、企業は医療従事者に自社製品の特典を教育し、普及を促進するために投資を行っています。さらに、病院やヘルスケアシステムとの提携は、製品へのアクセスや認知度の向上に役立ちます。これらの戦略は、市場への浸透を高め、競合を維持することを目的としています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 挿管を必要とする手術の増加

- 気管内チューブ技術の進歩

- ICU入院患者数と重症患者数の増加

- 新興市場におけるヘルスケアインフラの拡大

- 産業の潜在的リスク・課題

- 特殊な気管内チューブに関連する高コスト

- 挿管後合併症のリスク

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- 技術

- 償還シナリオ

- ポーター分析

- PESTEL分析

- ギャップ分析

- 将来の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- 標準気管内チューブ

- 強化気管内チューブ

- プレフォーム気管内チューブ

- ダブルルーメン気管内チューブ

第6章 市場推定・予測:材料別、2021~2034年

- 主要動向

- ポリ塩化ビニル(PVC)

- シリコン

- ポリウレタン

- その他

第7章 市場推定・予測:挿管経路別、2021~2034年

- 主要動向

- 経口気管

- 経鼻気管

第8章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 一般手術

- 緊急治療

- 治療

- 新生児と小児科ケア

- その他

第9章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 外来手術センター

- その他

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- ANGIPLAST

- Ambu

- Flexicare

- Fuji Systems

- icumedical

- INTERSURGCIAL

- Medline

- Medtronic

- Mercury Medical

- Romed HOLLAND

- STERIMED

- Teleflex

- TUORen

- VIGGOMEDICAL DEVICES

- Wellead

The Global Endotracheal Tube Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 4.2 billion by 2034. This expansion can be attributed to several factors, including the rising number of surgeries requiring intubation, the increasing incidence of ICU admissions and critical care cases, and the growth of healthcare infrastructure in emerging regions. Additionally, the global rise in chronic respiratory conditions such as asthma and chronic obstructive pulmonary disease (COPD), particularly among older adults, is contributing to the demand for endotracheal tubes.

Manufacturers are enhancing these products by incorporating features like antimicrobial coatings, new cuff designs, and subglottic suction to reduce complications like ventilator-associated pneumonia (VAP). These improvements are not only benefiting patients but are also driving the adoption of these devices in healthcare centers worldwide, contributing to market growth. An endotracheal tube is a flexible device used to secure the airway during surgeries, anesthesia, or critical care by passing through the mouth or nose into the trachea.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $4.2 Billion |

| CAGR | 6.8% |

It enables mechanical ventilation and helps maintain airway protection during procedures. The demand for ETTs is growing due to the rising prevalence of respiratory disorders, the shift toward disposable tubes, and the rising adoption of advanced intubation techniques such as video laryngoscopy. Additionally, there's a growing demand for tubes with antimicrobial and drug-eluting coatings in emergency care and out-of-hospital settings.

In 2024, the regular endotracheal tubes segment generated USD 1 billion. These tubes remain the preferred choice for routine surgical and emergency procedures, especially in resource-limited settings, due to their affordability compared to advanced alternatives. Their simple design makes them easy to use, and most healthcare professionals are trained to operate them efficiently, ensuring their widespread use in clinical settings.

The orotracheal tube segment generated USD 1.7 billion in 2024 and is expected to grow at a CAGR of 7% during 2034. Orotracheal intubation is the most common method for airway management in emergencies due to its speed and ease of execution. It is useful in trauma, cardiac arrest, and critical care situations, where securing the airway within minutes is crucial. The method is preferred over nasotracheal intubation, as it avoids complications like nasal bleeding and sinus infections and is considered safer for many adult patients.

U.S. Endotracheal Tube Market was valued at USD 785.5 million in 2024. The rising prevalence of respiratory diseases such as COPD, pneumonia, and acute respiratory distress syndrome (ARDS) has significantly boosted the demand for endotracheal tubes in the country. With policies from Medicare, Medicaid, and private insurers covering intubation and mechanical ventilation procedures, hospitals and surgery centers are more likely to adopt ETTs without facing financial constraints. These reimbursement policies play a pivotal role in encouraging best practices and increasing the use of endotracheal tubes, driving market growth.

Leading companies in the Global Endotracheal Tube Market include: Flexicare, Ambu, Fuji Systems, Medtronic, Medline, STERIMED, Teleflex, Romed HOLLAND, ANGIPLAST, Mercury Medical, INTERRACIAL, icumedical, VIGGOMEDICAL DEVICES, Wellead, and TUORen. To strengthen their market position, companies are focusing on several key strategies. They invest in product innovation by developing advanced features such as antimicrobial coatings and subglottic suction to improve patient safety and reduce complications. Partnerships with healthcare providers and expanding distribution channels in emerging markets are also critical for reaching a broader audience. Additionally, companies are investing in educating healthcare professionals about the benefits of their products to drive adoption. Furthermore, collaborations with hospitals and healthcare systems help ensure better product accessibility and visibility. These strategies aim to improve market penetration and maintain a competitive edge.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of surgeries requiring intubation

- 3.2.1.2 Advancements in endotracheal tube technology

- 3.2.1.3 Growth in ICU admissions and critical care patients

- 3.2.1.4 Expansion of healthcare infrastructure in emerging markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with specialized endotracheal tube

- 3.2.2.2 Risk of post-intubation complications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Gap analysis

- 3.10 Future market trends

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Regular endotracheal tube

- 5.3 Reinforced endotracheal tube

- 5.4 Performed endotracheal tube

- 5.5 Double lumen endotracheal tube

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Polyvinyl chloride (PVC)

- 6.3 Silicon

- 6.4 Polyurethane

- 6.5 Other materials

Chapter 7 Market Estimates and Forecast, By Route of Intubation, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Orotracheal

- 7.3 Nasotracheal

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 General surgery

- 8.3 Emergency treatment

- 8.4 Therapy

- 8.5 Neonatal and pediatric care

- 8.6 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ANGIPLAST

- 11.2 Ambu

- 11.3 Flexicare

- 11.4 Fuji Systems

- 11.5 icumedical

- 11.6 INTERSURGCIAL

- 11.7 Medline

- 11.8 Medtronic

- 11.9 Mercury Medical

- 11.10 Romed HOLLAND

- 11.11 STERIMED

- 11.12 Teleflex

- 11.13 TUORen

- 11.14 VIGGOMEDICAL DEVICES

- 11.15 Wellead