電気通信におけるビッグデータ分析の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Big Data Analytics in Telecom Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755191

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

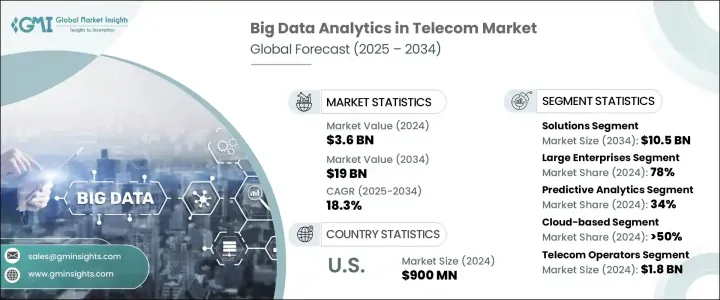

電気通信におけるビッグデータ分析の世界市場規模は、2024年に36億米ドルとなり、CAGR 18.3%で成長し、2034年には190億米ドルに達すると予測されています。

ビジネス上の意思決定を促進するためのデータへの依存が原動力となり、リアルタイム分析への需要が拡大しています。この拡大には、膨大な量の顧客データやネットワークデータを分析してネットワーク効率を高め、顧客体験を向上させ、データ主導の戦略的意思決定を行う通信会社のニーズが高まっていることが背景にあります。デジタルリテラシーと接続性の向上を目指す欧州委員会の「デジタルの10年」構想も、通信インフラにおける高度なアナリティクスの需要を促進しています。

スマートシティやモノのインターネット(IoT)の需要の高まりに対応するために通信ネットワークが拡大するにつれ、予測的でリアルタイムなアナリティクスの必要性がますます高まっています。通信事業者は、ネットワークパフォーマンスの強化、リソース配分の最適化、複数のプラットフォームにわたるシームレスなユーザー体験の確保を、こうした高度なアナリティクスに依存しています。潜在的なサービス破壊の状況を予測し、顧客に影響が及ぶ前に対処する能力は、急速に進化する通信情勢の中で競合優位性を維持するための重要な要因です。リアルタイムデータ分析により、事業者はネットワーク・トラフィックを監視し、問題を特定し、即座に是正措置を講じることができるため、高品質のサービス提供と顧客満足度の向上が実現します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 36億米ドル |

| 予測金額 | 190億米ドル |

| CAGR | 18.3% |

2024年には、ソリューション部門が55%のシェアで市場を席巻し、2034年には105億米ドルの売上が見込まれています。ソリューションセグメントには、データ管理ツール、分析ソフトウェア、データ可視化プラットフォーム、レポーティングシステムが含まれ、通信事業者が膨大なデータセットから貴重な洞察を得られるよう支援します。これらのプラットフォームにより、通信事業者はネットワークのパフォーマンスをリアルタイムで監視し、ネットワークの中断を予測・防止し、顧客分析を改善することができます。クラウドベースのアナリティクス・ソリューションの採用拡大がこの拡大をさらに後押ししており、通信事業者はサービス提供を改善しながら運用コストを削減できます。

大企業セグメントは2024年に78%のシェアを占める。大手通信事業者は、膨大な顧客ベースを扱い、複雑なネットワークインフラを管理し、優れたサービスを提供するためにビッグデータ分析を活用しています。予測分析を活用することで、こうした大手企業はネットワークの混雑や停止、その他の問題を予測し、サービスの中断を回避するための事前対策を講じることができます。この予測能力は、大量のデータをリアルタイムで分析する能力と相まって、通信事業者が十分な情報に基づいたデータ主導の戦略的意思決定を行うことを可能にします。

米国の電気通信におけるビッグデータ分析市場は2024年に9億米ドルを創出。米国は、その確立された通信インフラとデータ分析への多大な投資により、この分野での支配的なプレーヤーであり続けています。米国では消費者のデータ消費量が多いため、アナリティクス・ソリューションに対するニーズが高く、通信事業者は顧客の行動をよりよく理解し、解約を減らし、サービスをパーソナライズすることができます。米国の通信事業者はビッグデータ・アナリティクスを活用して、顧客に合わせたサービス・パッケージの提供、顧客満足度の向上、ロイヤルティの醸成を図っています。

電気通信におけるビッグデータ分析市場の主要企業には、Accenture, Amazon Web Services (AWS), ATOS, Alphabet, IBM, Huawei Technologies, Microsoft, Oracle, SAP, and Tencentなどがあります。市場ポジションを強化するため、通信分野のビッグデータ分析に携わる企業は、高度な分析機能を採用することでサービス提供の拡大に注力しています。これらの企業は、クラウドベースのアナリティクスソリューションを統合し、リアルタイムデータ処理に対する需要の高まりに対応できる、スケーラブルでコスト効率の高いサービスを提供しています。また、AIや機械学習技術を活用して、より正確な予測洞察を提供することで、通信事業者はネットワークパフォーマンスの最適化、ダウンタイムの防止、顧客体験の向上を実現しています。通信事業者との戦略的パートナーシップは、これらの企業が貴重なデータにアクセスする助けにもなっており、研究開発への投資は、通信業界の進化するニーズに応える革新的なソリューションの開発を可能にしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- クラウドプラットフォームプロバイダー

- データ統合および管理プロバイダー

- 分析ソリューションプロバイダー

- アプリケーションプロバイダー

- エンドユーザー

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 貿易への影響

- 価格設定と製品戦略

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- AIを活用したネットワーク最適化

- 5G対応エッジコンピューティング

- 通信クラウドのオーケストレーションと自動化

- 新興技術

- 通信分析のための量子コンピューティング

- AI統合型6Gネットワーク

- ブロックチェーンによるネットワークセキュリティ

- インテリジェントな仮想ネットワーク機能

- 先端材料科学

- 現在の技術動向

- 価格戦略

- 特許分析

- ユースケース

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 高速データ処理能力

- 高度なネットワーク最適化技術

- 顧客体験を向上させるリアルタイム分析

- 新興技術(AI、IoT、5G)との統合

- 業界の潜在的リスク&課題

- 高いインフラコストとメンテナンスコスト

- データ統合と管理の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- データ管理

- 分析ソフトウェア

- データの視覚化

- レポートツール

- その他

- サービス

- 専門サービス

- マネージドサービス

- コンサルティングとトレーニング

第6章 市場推計・予測:分析別、2021年~2034年

- 主要動向

- 記述的分析

- 診断分析

- 予測分析

- 処方的分析

第7章 市場推計・予測:組織規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

- パブリッククラウド

- プライベートクラウド

- ハイブリッドクラウド

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 顧客分析

- 顧客離脱予測

- 顧客生涯価値分析

- 顧客セグメンテーション

- ネットワーク分析

- ネットワーク最適化

- 障害管理

- 交通管理

- 運用分析

- リソースの最適化

- プロセス自動化

- マーケティング分析

- キャンペーン管理

- ソーシャルメディア分析

- 収益分析

- 不正行為検出

- 収益保証

- その他

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 通信サービスプロバイダー

- インターネットサービスプロバイダー(ISP)

- 仮想移動体通信事業者(MVNO)

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Accenture

- Alibaba

- Alphabet

- Altair Engineering

- Amazon Web Services(AWS)

- ATOS SE

- Databricks

- Hewlett Packard Enterprise Development

- Huawei Technologies

- IBM

- Informatica

- Infosys

- L&T

- Microsoft

- Oracle

- SAP

- Snowflake

- TATA Consultancy Services

- Tencent

- Wipro

目次

The Global Big Data Analytics in Telecom Market was valued at USD 3.6 billion in 2024 and is estimated to grow at a CAGR of 18.3% to reach USD 19 billion by 2034, driven by the dependency on data to drive business decisions, the demand for real-time analytics is growing. This expansion is fueled by the increasing need for telecom companies to analyze massive amounts of customer and network data to enhance network efficiencies, improve customer experience, and make data-driven strategic decisions. The European Commission's Digital Decade initiative, aiming to increase digital literacy and connectivity, is also driving the demand for advanced analytics in telecom infrastructure.

As telecom networks expand to accommodate the growing demands of smart cities and the Internet of Things (IoT), the need for predictive and real-time analytics has become increasingly essential. Telecom operators are relying on these advanced analytics to enhance network performance, optimize resource allocation, and ensure seamless user experience across multiple platforms. The ability to predict and address potential service disruptions before they impact customers is a key factor in maintaining a competitive edge in the rapidly evolving telecom landscape. Real-time data analytics allow operators to monitor network traffic, identify issues, and implement corrective measures instantly, ensuring high-quality service delivery and greater customer satisfaction.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $19 Billion |

| CAGR | 18.3% |

In 2024, the solutions segment dominated the market with a 55% share, and it is expected to generate USD 10.5 billion in revenue by 2034. The solutions segment includes data management tools, analytics software, data visualization platforms, and reporting systems, which help telecom operators gain valuable insights from their vast data sets. These platforms enable operators to monitor network performance in real-time, predict and prevent network disruptions, and improve customer analytics. The growing adoption of cloud-based analytics solutions further supports this expansion, helping telecom companies reduce operational costs while improving service delivery.

The large enterprises segment accounted for a 78% share in 2024. Major telecom giants leverage big data analytics to handle vast customer bases, manage complex network infrastructures, and deliver superior services. By utilizing predictive analytics, these large companies can anticipate network congestion, outages, or other issues and take proactive measures to avoid service disruptions. This predictive capability, coupled with the ability to analyze large volumes of data in real time, enables telecom operators to make well-informed, data-driven strategic decisions.

U.S. Big Data Analytics in Telecom Market generated USD 900 million in 2024. The U.S. continues to be a dominant player in this space due to its established telecommunications infrastructure and significant investment in data analytics. High data consumption levels by consumers in the U.S. create a strong need for analytics solutions, allowing telecom companies to better understand customer behavior, reduce churn, and personalize services. Telecom operators in the U.S. are leveraging big data analytics to offer tailored service packages, enhance customer satisfaction, and foster loyalty.

Major players in the Big Data Analytics in Telecom Market include Accenture, Amazon Web Services (AWS), ATOS, Alphabet, IBM, Huawei Technologies, Microsoft, Oracle, SAP, and Tencent. To strengthen their market position, companies in big data analytics for the telecom sector are focusing on expanding their service offerings by adopting advanced analytics capabilities. These players are integrating cloud-based analytics solutions to offer scalable, cost-effective services that can handle the growing demand for real-time data processing. They are also leveraging AI and machine learning technologies to deliver more accurate predictive insights, allowing telecom operators to optimize network performance, prevent downtimes, and enhance customer experience. Strategic partnerships with telecom operators are also helping these companies access valuable data, while R&D investments are enabling them to develop innovative solutions that cater to the evolving needs of the telecommunications industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model.

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Cloud platform providers

- 3.1.1.2 Data integration and management providers

- 3.1.1.3 Analytics solution providers

- 3.1.1.4 Application provider

- 3.1.1.5 End users

- 3.1.2 Profit margin analysis.

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring.

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets.

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration.

- 3.2.1 Impact on trade

- 3.3 Pricing and product strategies

- 3.4 Technology & innovation landscape

- 3.4.1 Current technological trends

- 3.4.1.1 AI-powered network optimization

- 3.4.1.2 5G-enabled edge computing

- 3.4.1.3 Telecom cloud orchestration and automation

- 3.4.2 Emerging Technologies

- 3.4.2.1 Quantum computing for telecom analytics

- 3.4.2.2 6G networks with AI integration

- 3.4.2.3 Blockchain-driven network security

- 3.4.2.4 Intelligent virtual network functions

- 3.4.3 Advanced material sciences

- 3.4.1 Current technological trends

- 3.5 Pricing strategies

- 3.6 Patent analysis

- 3.7 Use cases.

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 High-speed data processing capabilities

- 3.10.1.2 Advanced network optimization techniques

- 3.10.1.3 Real-time analytics for enhanced customer experience

- 3.10.1.4 Integration with emerging technologies (AI, IoT, 5G)

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High infrastructure and maintenance costs

- 3.10.2.2 Complexity of data integration and management

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Data management

- 5.2.2 Analytics software

- 5.2.3 Data visualization

- 5.2.4 Reporting tools

- 5.2.5 Others

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

- 5.3.3 Consulting & training

Chapter 6 Market Estimates & Forecast, By Analytics, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Descriptive analytics

- 6.3 Diagnostic analytics

- 6.4 Predictive analytics

- 6.5 Prescriptive analytics

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Small & medium-sized enterprises (SME)

- 7.3 Large Enterprises

Chapter 8 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 On-premises

- 8.3 Cloud-based

- 8.3.1 Public cloud

- 8.3.2 Private cloud

- 8.3.3 Hybrid cloud

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Customer analysis

- 9.2.1 Customer churn prediction

- 9.2.2 Customer lifetime value analysis

- 9.2.3 Customer segmentation

- 9.3 Network analysis

- 9.3.1 Network optimization

- 9.3.2 Fault management

- 9.3.3 Traffic management

- 9.4 Operational analysis

- 9.4.1 Resource optimization

- 9.4.2 Process automation

- 9.5 Marketing analysis

- 9.5.1 Campaign management

- 9.5.2 Social media analytics

- 9.6 Revenue analysis

- 9.6.1 Fraud detection

- 9.6.2 Revenue assuranc

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 Telecom service providers

- 10.3 Internet service providers (ISPs)

- 10.4 Mobile virtual network operators (MVNOs)

- 10.5 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 11.1 North America

- 11.1.1 U.S.

- 11.1.2 Canada

- 11.2 Europe

- 11.2.1 UK

- 11.2.2 Germany

- 11.2.3 France

- 11.2.4 Italy

- 11.2.5 Spain

- 11.2.6 Belgium

- 11.2.7 Sweden

- 11.3 Asia Pacific

- 11.3.1 China

- 11.3.2 India

- 11.3.3 Japan

- 11.3.4 Australia

- 11.3.5 Singapore

- 11.3.6 South Korea

- 11.3.7 Southeast Asia

- 11.4 Latin America

- 11.4.1 Brazil

- 11.4.2 Mexico

- 11.4.3 Argentina

- 11.5 MEA

- 11.5.1 South Africa

- 11.5.2 Saudi Arabia

- 11.5.3 UAE

Chapter 12 Company Profiles

- 12.1 Accenture

- 12.2 Alibaba

- 12.3 Alphabet

- 12.4 Altair Engineering

- 12.5 Amazon Web Services (AWS)

- 12.6 ATOS SE

- 12.7 Databricks

- 12.8 Hewlett Packard Enterprise Development

- 12.9 Huawei Technologies

- 12.10 IBM

- 12.11 Informatica

- 12.12 Infosys

- 12.13 L&T

- 12.14 Microsoft

- 12.15 Oracle

- 12.16 SAP

- 12.17 Snowflake

- 12.18 TATA Consultancy Services

- 12.19 Tencent

- 12.20 Wipro

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日