|

市場調査レポート

商品コード

1750626

電池試験装置市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)Battery Test Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電池試験装置市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年05月05日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

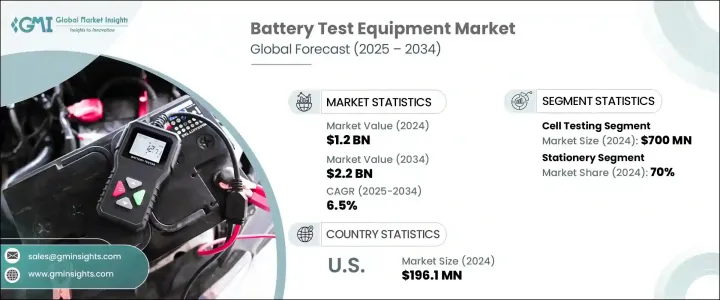

世界の電池試験装置の市場規模は、2024年に12億米ドルとなり、電動モビリティ需要の高まり、再生可能エネルギーインフラの進歩、スマート電子デバイスの成長に牽引され、6.5%のCAGRで成長し、2034年には22億米ドルに達すると予測されています。

電池システムがより複雑で高性能になるにつれて、メーカーは電池の耐久性、精度、国際安全規格への準拠を保証する試験ツールを重視するようになっています。電池の健全性、ライフサイクルの最適化、予測診断に対するこのような注目の高まりにより、試験装置は業界全体で不可欠なものとなっています。自動化、データ分析、クラウドプラットフォームの統合も、従来の試験ワークフローを変革しています。

これらのインテリジェントシステムは、リアルタイムのモニタリング、高度なデータロギング、エラー検出を可能にし、メーカーに迅速でより正確な洞察を提供します。新しい電池用化学物質やアーキテクチャが登場するにつれ、輸送、ストレージ、エレクトロニクスなどの分野で製品の信頼性を維持するために、柔軟でスケーラブル、かつスマートな試験ソリューションの必要性がますます高まっています。これらの最新システムは、診断の精度を向上させるだけでなく、試験サイクルタイムを短縮し、革新的な電池技術の市場投入までの時間を短縮します。また、幅広いセル形式や構成に対応できるため、急速に進化するエネルギー環境において、常に適切な製品であり続けることができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 12億米ドル |

| 市場規模予測 | 22億米ドル |

| CAGR | 6.5% |

機能セグメントの中では、セルレベルでのテストが2024年に優位を占め、7億米ドルを創出しました。これは、電池モジュールやパックに組み立てる前に、エネルギー容量、内部抵抗、電圧の一貫性に関連する問題を検出するために、個々のセルを詳細に分析する必要があるためです。このような基礎的な評価は、システム全体の故障を防止し、運用効率を向上させる上で極めて重要な役割を果たします。電池技術の急速な進化に伴い、セル試験は製品の寿命と安全性能を保証する上で、これまで以上に極めて重要になっています。

製品種類別では、据置型試験システムが2024年に市場の70%を占め、最大のシェアを占めています。その優れた精度、より長い試験能力、複雑な性能評価を管理する能力により、大規模エネルギー貯蔵や大型電池ユニットを含むアプリケーションに理想的なものとなっています。制御された条件下での包括的な分析の必要性から、高性能エネルギー・ソリューションの提供に注力する開発者、研究開発者、電池メーカーにとって、据置型装置は引き続き好ましい選択肢となっています。

米国の電池試験装置の2024年の市場規模は1億9,610万米ドルで、2034年までCAGR 6.8%で成長すると予測されています。継続的な技術革新、クリーンエネルギー分野の拡大、電池の生産と試験インフラへの投資の増加がその要因です。また、政府の支援政策や電動モビリティの急速な普及も、同地域全体で高度な電池試験技術に対する需要を加速させています。

Chroma ATE、Arbin、NH Research、Midtronics、Neware Technology Limitedなどの企業は、市場での地位を強化するため、製品イノベーション、世界展開、コラボレーションに重点を置いた戦略的イニシアチブを推進しています。試験精度を高め、進化する電池化学をサポートするため、多くの企業が研究開発に投資しています。MaccorやBitrodeなどの企業は、多様な顧客ニーズに対応する拡張可能なモジュール式試験プラットフォームを発表しています。さらに、複数の企業がAI主導の分析とクラウド接続を統合し、インテリジェントな診断ツールを提供しています。研究機関や市場力学との提携は、カスタマイズされたサービスの提供とともに、これらの企業がダイナミックでイノベーション主導の市場で競争上の優位性を獲得するのに役立っています。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- 技術プロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権の関税による影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳の分析

- 最新動向と主な取り組み

- 影響要因

- 促進要因

- 充電式電池の需要増加

- 電気自動車(EV)の普及の増加

- エネルギー貯蔵システムの拡張

- 電池試験における技術の進歩

- 業界の潜在的リスクと課題

- 初期投資コストが高め

- 電池技術の複雑さ

- 促進要因

- 成長可能性分析

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニング・マトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:種類別(2021~2034年)

- 主要動向

- 据置型

- 携帯型

第6章 市場推計・予測:機能別(2021~2034年)

- 主要動向

- セル試験

- モジュール試験

- パック試験

第7章 市場推計・予測:装備別(2021~2034年)

- 主要動向

- 容量テスター

- 安全性試験装置

- 温度テスター

- 抵抗テスター

- 電圧モニター

- 障害追跡

- その他

第8章 市場推計・予測:用途別(2021~2034年)

- 主要動向

- 自動車

- 家電

- エネルギー・ユーティリティ

- その他

第9章 市場推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- AMETEK

- Amprobe

- Arbin Instruments

- BatteryDAQ

- Bio-Logic Science

- Bitrode

- Cadex Electronics

- Chroma ATE

- Digatron Power Electronics

- FLIR Systems

- HIOKI E.E.

- ITECH Electronic

- Keysight Technologies

- Maccor

- Megger

- Midtronics

- Neware

- NH Research

- Pine Research

- Tenmars

The Global Battery Test Equipment Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 2.2 billion by 2034, driven by the rising demand for electric mobility, advancements in renewable energy infrastructure, and growth in smart electronic devices. As battery systems become more complex and performance-intensive, manufacturers are placing higher emphasis on testing tools that ensure battery durability, accuracy, and compliance with international safety standards. This rising focus on battery health, lifecycle optimization, and predictive diagnostics has made test equipment essential across industries. The integration of automation, data analytics, and cloud platforms is also transforming traditional testing workflows.

These intelligent systems allow for real-time monitoring, advanced data logging, and error detection, providing manufacturers with faster, more precise insights. As new battery chemistries and architectures emerge, the need for flexible, scalable, and smart testing solutions becomes increasingly critical in maintaining product reliability across sectors such as transportation, storage, and electronics. These modern systems not only improve the accuracy of diagnostics but also reduce testing cycle times, enabling quicker time-to-market for innovative battery technologies. Their adaptability to a wide range of cell formats and configurations ensures they remain relevant in a rapidly evolving energy landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 6.5% |

Among functional segments, testing at the cell level dominated in 2024, generating USD 700 million due to the need for detailed analysis of individual cells to detect issues related to energy capacity, internal resistance, and voltage consistency before assembly into battery modules or packs. Such foundational evaluation plays a pivotal role in preventing system-wide failures and improving operational efficiency. With the rapid evolution of battery technology, cell testing has become more crucial than ever in guaranteeing product longevity and safe performance.

From a product type perspective, stationary test systems held the largest share of the market, accounting for 70% in 2024. Their superior precision, longer testing capabilities, and ability to manage complex performance evaluations have made them ideal for applications involving large-scale energy storage and heavy-duty battery units. The need for comprehensive analysis under controlled conditions continues to make stationary equipment the preferred choice for developers, researchers, and battery manufacturers focused on delivering high-performance energy solutions.

United States Battery Test Equipment Market generated USD 196.1 million in 2024 and is projected to grow at a CAGR of 6.8% through 2034, driven by continuous innovation, expansion in the clean energy sector, and increasing investments in battery production and testing infrastructure. Supportive government policies and the rapid adoption of electric mobility have also accelerated the demand for advanced battery testing technologies across the region.

To strengthen their market position, companies like Chroma ATE, Arbin, NH Research, Midtronics, and Neware Technology Limited are pursuing strategic initiatives focused on product innovation, global expansion, and collaboration. Many are investing in R&D to enhance test precision and support evolving battery chemistry. Firms such as Maccor and Bitrode are launching scalable, modular testing platforms that address diverse customer needs. Additionally, several players are integrating AI-driven analytics and cloud connectivity to offer intelligent diagnostic tools. Partnerships with research institutes and OEMs, along with customized service offerings, are also helping these companies gain competitive advantages in a dynamic, innovation-driven market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for rechargeable batteries

- 3.8.1.2 Growth in electric vehicle (EV) adoption

- 3.8.1.3 Expansion of energy storage systems

- 3.8.1.4 Technological advancements in battery testing

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High Initial Investment Costs

- 3.8.2.2 Complexity of Battery Technologies

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Stationary

- 5.3 Portable

Chapter 6 Market Estimates & Forecast, By Function, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Cell testing

- 6.3 Module testing

- 6.4 Pack testing

Chapter 7 Market Estimates & Forecast, By Equipment, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Capacity tester

- 7.3 Safety testing equipment

- 7.4 Temperature tester

- 7.5 Resistance tester

- 7.6 Voltage monitor

- 7.7 Fault tracker

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Consumer electronics

- 8.4 Energy and utility

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AMETEK

- 10.2 Amprobe

- 10.3 Arbin Instruments

- 10.4 BatteryDAQ

- 10.5 Bio-Logic Science

- 10.6 Bitrode

- 10.7 Cadex Electronics

- 10.8 Chroma ATE

- 10.9 Digatron Power Electronics

- 10.10 FLIR Systems

- 10.11 HIOKI E.E.

- 10.12 ITECH Electronic

- 10.13 Keysight Technologies

- 10.14 Maccor

- 10.15 Megger

- 10.16 Midtronics

- 10.17 Neware

- 10.18 NH Research

- 10.19 Pine Research

- 10.20 Tenmars