経橈骨アクセスデバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Transradial Access Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750613

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

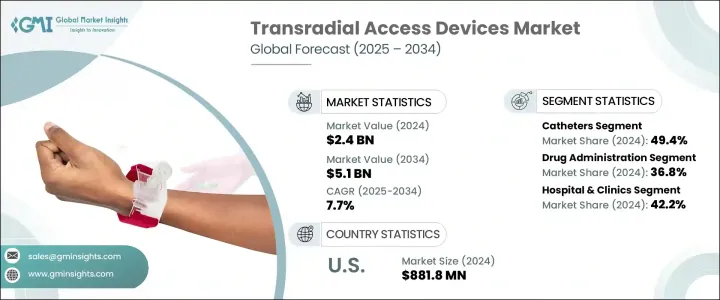

世界の経橈骨アクセスデバイス市場は、2024年には24億米ドルと評価され、心血管疾患(CVDs)の有病率の増加や低侵襲的介入手技への嗜好の高まりに牽引され、CAGR 7.7%で成長し、2034年には51億米ドルに達すると推定されています。

経橈骨動脈アクセスは、従来型方法と比較して、患者の回復が早く、出血のリスクが減少し、入院期間が短縮されることから、支持を集めています。ヘルスケアプロバイダが安全性、快適性、効率性を優先しているため、橈骨動脈アクセスへのシフトは臨床診療を再構築しています。カテーテル検査室におけるラジアルファーストアプローチの使用動向は、その臨床的信頼性と操作上の利点が実証されたことにより、さらに拍車がかかっています。

このようなラジアル手技への依存の高まりは、シース、ガイドワイヤ、止血バンド、カテーテルなどのコンポーネントを含め、経橈骨アクセスデバイスに対する世界の旺盛な需要を牽引しています。ラジアルアプローチの臨床的利点(出血リスクの低減、患者の迅速な移動、入院期間の短縮など)は、インターベンショナルカーディオロジーにおける手技プロトコルを形成し続けています。ヘルスケアプロバイダが効率と患者満足度の最適化を目指す中、ラジアルファースト戦略の採用は先進国市場だけでなく、心血管インフラが改善しつつある新興経済諸国でも勢いを増しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 24億米ドル |

| 予測金額 | 51億米ドル |

| CAGR | 7.7% |

カテーテルは現在、2024年の市場シェア49.4%で製品セグメントをリードしています。複雑な血管網を通過し、正確なデバイス送達を促進するカテーテルの有効性は、診断と治療的心臓処置において不可欠です。トルク応答の改善、柔軟性の向上、親水性コーティングなど、カテーテル設計の革新により、手技の成功率と患者の転帰全体が大幅に向上しています。さらに、経橈骨インターベンション専用に設計された次世代カテーテルは、アクセス部位の合併症軽減と手技効率の向上に寄与しています。

さらに、薬剤投与セグメントは2024年に36.8%の市場シェアを占め、2034年には18億米ドルに達すると予測されています。これらの機器では、患部に直接標的薬剤を投与できるため、治療効果が高まるだけでなく、回復時間も短縮されます。この機能は、迅速なドラッグデリバリーが救命につながる急性心血管系イベントにおいて重要です。経橈骨動脈アクセスは,その正確さと低侵襲性により,現在,より広範な応用が検討されつつあります。心臓と非心臓疾患に対する薬理学的薬剤の送達における経橈骨アクセスの役割の増大は、経橈骨ソリューションの適応性と範囲の拡大を反映しています。

米国の経橈骨アクセスデバイス 2024年の市場規模は8億8,180万米ドルで、心血管インターベンションの件数、支持的な償還施策、ラジアルアクセスを好むオペレーターが普及を加速させています。経橈骨手術の利点に対する認識が高まり、ヘルスケアシステム全体の統合が進んでいます。病院はラジアルアクセスの回復時間の短縮と手技の簡便さを利用し、外来ベースのPCIモデルに急速に移行しています。規制当局の支援、臨床トレーニングプログラム、先進的なカテ室インフラへの投資は、これらの機器の普及をさらに強化しています。このような先進的な環境は、経橈骨動脈アクセスがこの地域におけるインターベンショナルカーディオロジー技術革新の最前線にあることを保証しています。

このセグメントで事業を展開する主要企業には、Boston Scientific、Alvimedica、Becton Dickinson and Company、Terumo、Medtronic、Teleflex、Palex Medical、ICU Medical、InnoMedica、Cardinal Health、Merit Medical System、Edward Lifesciences、NIPRO Medical、Ameco Medical Industries、AngioDynamics、Oscorなどがあります。競争優位性を確保するため、主要企業は製品革新と技術アップグレードに注力しています。臨床医の使いやすさと患者の快適性を高めるため、先端材料や人間工学に基づいたデザイン、機能性の向上に投資しています。多くの企業は、戦略的パートナーシップ、合併、買収を通じて、地理的なフットプリントを拡大しています。病院やヘルスケアネットワークとの提携は、早期導入と市場浸透に役立ちます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 先進国と新興経済諸国における心血管疾患の有病率の増加

- 高齢者層の成長

- 橈骨動脈アクセスを用いた介入処置に対する好みの高まり

- 小児患者におけるラジアルアクセスデバイスの使用増加

- 産業の潜在的リスク・課題

- 厳格な規制枠組み

- 血管アクセスデバイスの高コストとメンテナンス

- 発展途上国における心臓胸部外科医の不足

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 産業への影響

- 供給側の影響(原料)

- 主要原料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原料)

- 影響を受ける主要企業

- 戦略的な産業対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 施策関与

- 展望と今後の検討事項トランプ政権の関税

- 貿易への影響

- 将来の市場動向

- ギャップ分析

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:製品別、2021~2034年

- 主要動向

- カテーテル

- ガイドワイヤ

- シースとシースイントロデューサー

- 付属品

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 薬剤投与

- 水分と栄養の投与

- 輸血

- 診断と検査

- その他

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院とクリニック

- 外来手術センター

- その他

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Alvimedica

- Ameco Medical Industries

- AngioDynamics

- Becton Dickinson and Company

- Boston Scientific

- Cardinal Health

- Edward Lifesciences

- ICU Medical

- InnoMedica

- Medtronic

- Merit Medical System

- NIPRO Medical

- Oscor

- Palex Medical

- Teleflex

- Terumo

目次

The Global Transradial Access Devices Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 5.1 billion by 2034, driven by the increasing prevalence of cardiovascular diseases (CVDs) and the rising preference for minimally invasive interventional procedures. Transradial access is gaining traction due to its ability to offer faster patient recovery, reduced risk of bleeding, and shorter hospital stays compared to traditional methods. The shift toward radial artery access has reshaped clinical practice, as healthcare providers prioritize safety, comfort, and efficiency. The trend toward using radial-first approaches in catheterization laboratories has been further fueled by its demonstrated clinical reliability and operational benefits.

This increasing reliance on radial techniques drives strong demand for transradial access devices worldwide, including components such as sheaths, guidewires, hemostasis bands, and catheters. The clinical advantages of the radial approach-such as lower bleeding risk, faster patient mobilization, and shorter hospital stays-continue to shape procedural protocols in interventional cardiology. As healthcare providers aim to optimize efficiency and patient satisfaction, adopting radial-first strategies is expanding not only in developed markets but also gaining momentum in emerging economies with improving cardiovascular infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 7.7% |

Catheters currently lead the product segment with a commanding market share of 49.4% in 2024. Their effectiveness in navigating complex vascular networks and facilitating accurate device delivery makes them vital in diagnostic and therapeutic cardiac procedures. Innovation in catheter designs, such as improved torque response, enhanced flexibility, and hydrophilic coatings, has significantly boosted procedural success rates and overall patient outcomes. Furthermore, next-generation catheters designed specifically for transradial interventions contribute to reduced access site complications and increased procedural efficiency.

Additionally, the drug administration segment holds a 36.8% market share in 2024 and is forecasted to reach USD 1.8 billion by 2034. The ability of these devices to deliver targeted medications directly to affected areas not only enhances therapeutic results but also shortens recovery times. This capability is important in acute cardiovascular events, where rapid drug delivery can be life-saving. Transradial access is now being increasingly explored for broader applications, thanks to its precision and minimally invasive nature. Its growing role in delivering pharmacological agents for cardiac and non-cardiac conditions reflects the adaptability and expanding scope of transradial solutions.

U.S. Transradial Access Devices Market generated USD 881.8 million in 2024, driven by the number of cardiovascular interventions, supportive reimbursement policies, and operator preference for radial access, which is accelerating adoption. Increased awareness of the benefits of transradial procedures is leading to greater integration across healthcare systems. Hospitals are rapidly transitioning to outpatient-based PCI models, taking advantage of the reduced recovery time and procedural simplicity of radial access. Regulatory support, clinical training programs, and investment in advanced cath lab infrastructure further reinforce the widespread use of these devices. This progressive environment ensures that transradial access remains at the forefront of interventional cardiology innovation in the region.

Key players operating in this space include Boston Scientific, Alvimedica, Becton Dickinson and Company, Terumo, Medtronic, Teleflex, Palex Medical, ICU Medical, InnoMedica, Cardinal Health, Merit Medical System, Edward Lifesciences, NIPRO Medical, Ameco Medical Industries, AngioDynamics, and Oscor. To secure a competitive edge, leading companies are focusing on product innovation and technological upgrades. They invest in advanced materials, ergonomic designs, and improved functionality to boost clinician usability and patient comfort. Many firms expand their geographic footprint through strategic partnerships, mergers, and acquisitions. Collaborations with hospitals and healthcare networks help in early adoption and market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cardiovascular disease in developed and developing economies

- 3.2.1.2 Growth in elderly age group

- 3.2.1.3 Rising preference for interventional procedures using radial artery access

- 3.2.1.4 Growing use of radial access devices in pediatric patients

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory framework

- 3.2.2.2 High cost and maintenance of vascular access devices

- 3.2.2.3 Dearth of cardiothoracic surgeons in developing nations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Trump administration tariffs

- 3.6.1 Impact on trade

- 3.6.1.1 Trade volume disruptions

- 3.6.1.2 Retaliatory measures

- 3.6.2 Impact on the Industry

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.2.1.1 Price volatility in key materials

- 3.6.2.1.2 Supply chain restructuring

- 3.6.2.1.3 Production cost implications

- 3.6.2.2 Demand-side impact (selling price)

- 3.6.2.2.1 Price transmission to end markets

- 3.6.2.2.2 Market share dynamics

- 3.6.2.2.3 Consumer response patterns

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.3 Key companies impacted

- 3.6.4 Strategic industry responses

- 3.6.4.1 Supply chain reconfiguration

- 3.6.4.2 Pricing and product strategies

- 3.6.4.3 Policy engagement

- 3.6.5 Outlook and future considerationsTrump administration tariffs

- 3.6.1 Impact on trade

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive analysis of major market players

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Catheters

- 5.3 Guidewires

- 5.4 Sheath and sheath introducers

- 5.5 Accessories

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Drug administration

- 6.3 Fluid and nutrition administration

- 6.4 Blood transfusion

- 6.5 Diagnostics and testing

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alvimedica

- 9.2 Ameco Medical Industries

- 9.3 AngioDynamics

- 9.4 Becton Dickinson and Company

- 9.5 Boston Scientific

- 9.6 Cardinal Health

- 9.7 Edward Lifesciences

- 9.8 ICU Medical

- 9.9 InnoMedica

- 9.10 Medtronic

- 9.11 Merit Medical System

- 9.12 NIPRO Medical

- 9.13 Oscor

- 9.14 Palex Medical

- 9.15 Teleflex

- 9.16 Terumo

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日