産業用コネクタ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Industrial Connector Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 137 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750595

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

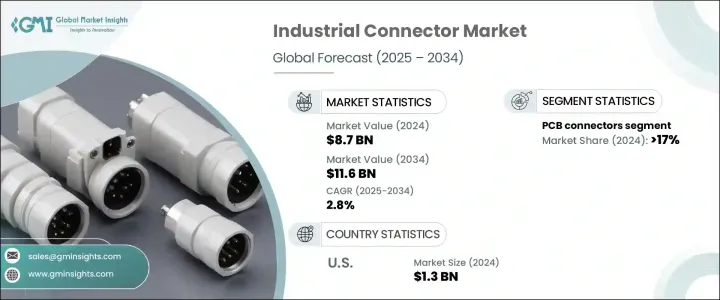

産業用コネクタの世界市場規模は、2024年に87億米ドルとなり、産業オートメーションの成長、技術の進歩、インダストリー4.0の下でのスマートファクトリーコンセプトの広範な統合により、CAGR 2.8%で成長し、2034年には116億米ドルに達すると推定されています。

これらのコネクタは、センサー、アクチュエーター、制御ユニットなどの重要なコンポーネントを接続し、多くのオートメーションシステム全体で信頼性の高い通信と機能性を確保するために不可欠です。工場や製造環境のスマート化に伴い、高速データ交換、高速伝送、精密な自動化をサポートする高性能コネクタの必要性が高まっています。産業用コネクタは、堅牢なシステム性能を確保する上で極めて重要であるだけでなく、継続的なデータフローにますます依存するようになっている機械の効率的な運転にも貢献しています。

コネクター分野における技術の進歩は、産業用コネクターの範囲を広げ、機能性を強化した小型軽量設計を導入しています。高速データ転送、防振機能、極端な温度に対する耐性などの機能により、さまざまな産業でこれらのコネクターに対する需要が高まっています。この分野の重要な動向は、温度、圧力、接続性などのパラメーターを測定し、システム全体の性能と信頼性を向上させるセンサーをコネクターに内蔵することです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 87億米ドル |

| 予測金額 | 116億米ドル |

| CAGR | 2.8% |

PCB(プリント基板)コネクタセグメントは、製造、エネルギー、通信、自動車産業など複数の産業分野でPCBコネクタの需要が伸びていることが要因で、2024年には17%の大きなシェアを占めました。これらのコネクタは、電子機器やシステムの動作に不可欠なプリント回路基板に信頼性の高い電気接続を提供するために不可欠です。製造分野では、PCBコネクタは、異なる回路基板コンポーネント間の接続を確立し、シームレスなデータ伝送と配電を保証します。

米国の産業用コネクタ市場は2024年に13億米ドルと評価され、自動化、高度製造技術、産業用モノのインターネット(IIoT)への強い注目が高性能コネクタの需要を促進しています。スマート工場と接続された製造システムへのシフトは、信頼性が高く堅牢なコネクタの必要性に影響を与えます。オートメーションとデジタルシステムへの投資の増加は、この地域でのビジネスチャンスを拡大し続け、効率的でシームレスなオペレーションを確保するために洗練されたコネクターを必要とする産業が増えています。

世界の産業用コネクタ市場の主要企業には、TE Connectivity、Amphenol Corporation、3M、Molex, Inc.、Phoenix Contact、Aptiv PLCなどがあります。これらの業界大手は、技術的専門知識を活用してコネクター設計の革新を推進し、性能と信頼性を高めています。市場ポジションを強化するため、産業用コネクタ業界の企業は、戦略的パートナーシップやコラボレーションに重点を置き、製品提供の革新と向上を図っています。多くの企業は、高速データ転送や環境ストレス要因への耐性など、機能性を向上させたコネクタを開発するため、研究開発に多額の投資を行っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業の市場シェア

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- PCBコネクタ

- IOコネクタ

- 円形コネクタ

- 光ファイバーコネクタ

- RF同軸コネクタ

- その他

第6章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第7章 企業プロファイル

- 3M

- AMETEK Inc.

- Amphenol Corporation

- Aptiv PLC

- AVX Corporation

- Fischer Connectors

- Foxconn Technology Group

- GTK UK Ltd.

- Hirose Electric Co.、Ltd.

- Japan Aviation Electronics Industry、Ltd.

- Lapp Group

- Luxshare Precision Industry Co.、Ltd.

- Mencom Corporation

- Molex、Inc.

- Phoenix Contact

- Rosenberger Group

- TE Connectivity

- YAZAKI Corporation

目次

The Global Industrial Connector Market was valued at USD 8.7 billion in 2024 and is estimated to grow at a CAGR of 2.8% to reach USD 11.6 billion by 2034, driven by the growth of industrial automation, technological advancements, and the widespread integration of smart factory concepts under Industry 4.0. These connectors are essential for ensuring reliable communication and functionality across many automation systems, connecting critical components such as sensors, actuators, and control units. As factories and manufacturing environments become smarter, the need for high-performance connectors that support fast data exchange, high-speed transmission, and precise automation is increasing. Industrial connectors are not only pivotal in ensuring robust system performance but also contribute to the efficient operation of machines, which increasingly rely on continuous data flow.

Technology advancements in the connector space have broadened the scope of industrial connectors, introducing miniature and lightweight designs with enhanced functionality. Features like high-speed data transfer, anti-vibration capabilities, and resistance to extreme temperatures have increased the demand for these connectors across multiple industries. A significant trend in the sector is the inclusion of built-in sensors in connectors, which measure parameters like temperature, pressure, and connectivity, improving the overall system performance and reliability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.7 Billion |

| Forecast Value | $11.6 Billion |

| CAGR | 2.8% |

The PCB (Printed Circuit Board) connector segment held a significant share of 17% in 2024, attributed to the growing demand for PCB connectors across multiple industrial sectors, including manufacturing, energy, telecommunications, and automotive industries. These connectors are essential for providing reliable electrical connections on printed circuit boards integral in operating electronic devices and systems. In the manufacturing sector, PCB connectors establish connections between different circuit board components, ensuring seamless data transmission and power distribution.

U.S. Industrial Connector Market was valued at USD 1.3 billion in 2024, driven by its strong focus on automation, advanced manufacturing technologies, and the Industrial Internet of Things (IIoT), which is fueling demand for high-performance connectors. The shift toward smart factories and connected manufacturing systems impacts the need for reliable and robust connectors. Increased investment in automation and digital systems continues to expand opportunities in the region, with more industries requiring sophisticated connectors to ensure efficient and seamless operations.

Leading players in the Global Industrial Connector Market include TE Connectivity, Amphenol Corporation, 3M, Molex, Inc., Phoenix Contact, and Aptiv PLC. These industry giants leverage their technological expertise to drive innovation in connector designs, enhancing performance and reliability. To strengthen their market position, companies in the industrial connector industry are focusing on strategic partnerships and collaborations to innovate and improve their product offerings. Many companies are investing heavily in R&D to develop connectors with improved functionalities, such as high-speed data transfer and resistance to environmental stress factors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiative

- 4.4 Company market share

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (Million Units & USD Billion)

- 5.1 Key trends

- 5.2 PCB connectors

- 5.3 IO connectors

- 5.4 Circular connectors

- 5.5 Fiber optic connectors

- 5.6 RF coaxial connectors

- 5.7 Others

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034 (Million Units & USD Billion)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 France

- 6.3.3 UK

- 6.3.4 Italy

- 6.3.5 Spain

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 South Korea

- 6.4.5 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

Chapter 7 Company Profiles

- 7.1 3M

- 7.2 AMETEK Inc.

- 7.3 Amphenol Corporation

- 7.4 Aptiv PLC

- 7.5 AVX Corporation

- 7.6 Fischer Connectors

- 7.7 Foxconn Technology Group

- 7.8 GTK UK Ltd.

- 7.9 Hirose Electric Co., Ltd.

- 7.10 Japan Aviation Electronics Industry, Ltd.

- 7.11 Lapp Group

- 7.12 Luxshare Precision Industry Co., Ltd.

- 7.13 Mencom Corporation

- 7.14 Molex, Inc.

- 7.15 Phoenix Contact

- 7.16 Rosenberger Group

- 7.17 TE Connectivity

- 7.18 YAZAKI Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 137 Pages

- 納期

- 2~3営業日