|

市場調査レポート

商品コード

1750575

住宅用ソーラー発電機市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Residential Solar Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 住宅用ソーラー発電機市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年05月15日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

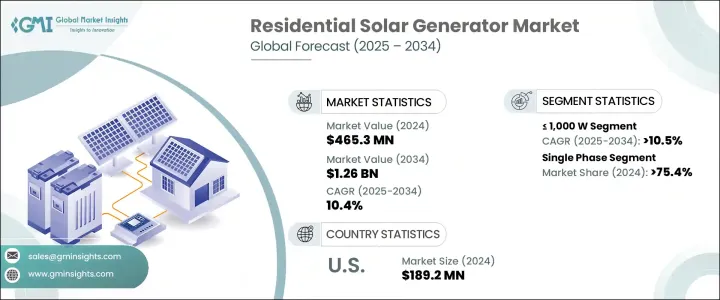

世界の住宅用ソーラー発電機市場は、2024年に4億6,530万米ドルと評価され、クリーンで再生可能なエネルギーソリューションに対する需要の高まりと住宅所有者の環境意識の高まりにより、CAGR 10.4%で成長し、2034年には12億6,000万米ドルに達すると予測されています。

世界がより持続可能なエネルギー選択肢へとシフトする中、太陽光発電機は住宅用途の最重要選択肢となりつつあります。エネルギー自給の推進に加え、送電網システムの頻繁な不安定化と電力途絶の増加が、このシフトを加速させています。リチウムイオン電池や固体電池技術の継続的な改良、家庭におけるエネルギー管理システムの統合が、住宅用ソーラー・ソリューションの魅力を高めています。こうした進歩により、太陽光発電機はより効率的で耐久性があり、使いやすいものとなっています。

再生可能エネルギー導入のための排出削減と税制優遇措置に焦点を当てた政府の政策は、重要な役割を果たしています。スマートホームシステムの継続的な採用は、エネルギー節約を優先し、市場拡大に貢献しています。製造コストの上昇や輸入部品への関税といった課題があるにせよ、この分野では国内製造と技術革新への注目が高まっているため、長期的な見通しは依然として強いです。住宅用ソーラー発電機は、電気料金の削減や二酸化炭素排出量の削減が可能であることも評価されており、よりクリーンなエネルギー源の導入を目指す住宅所有者にとっては魅力的な投資先となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 4億6,530万米ドル |

| 予測金額 | 12億6,000万米ドル |

| CAGR | 10.4% |

1,000W以上2,000W未満の発電機は、2024年に1億5,000万米ドルを生み出し、住宅環境における重要性の高まりを反映しています。このようなミッドレンジのシステムは、停電が頻発する地域で特に好まれており、インフラの大幅なアップグレードを必要とせずに、信頼性が高く効率的なバックアップ電源を住宅所有者に提供しています。コンパクトなサイズで、必要な電化製品に十分な出力があるため、中小規模の住宅に最適です。この分野は、消費者が電力容量と携帯性のバランスが取れた費用対効果の高いエネルギー・ソリューションを求めているため、引き続き牽引力を増しています。

三相ソーラー発電機分野は、2034年までのCAGRが10%と予測されており、力強い成長が見込まれています。この動向は、より大きな電気負荷に対応し、再生可能エネルギーの枠組みとシームレスに統合できるシステムに対するニーズの高まりが原動力となっています。ソーラーパネル、電気自動車充電ステーション、エネルギー管理システムを組み込む住宅が増えるにつれ、三相構成の需要が高まる。これらの発電機は、高効率のエネルギー使用をサポートするように設計されているため、安定性と拡張性が重要なスマートホームや大規模な住宅設備には不可欠です。

米国の住宅用ソーラー発電機2024年の市場規模は1億8,920万米ドルで、世界で最も先進的なエネルギー市場の1つである米国に力強い勢いがあることを示しています。異常気象や送電網インフラの老朽化による停電の増加に伴い、住宅所有者はこれまで以上にエネルギーの安全性を優先するようになっています。この変化は、オフグリッドの信頼性と長期的な節約を提供する太陽光発電バックアップ・システムの採用を後押ししています。税額控除、リベート、クリーン・エネルギー・プロジェクトへの資金援助といった米国政府のイニシアチブは、特に電気料金が高く停電が頻発する州において、市場浸透を加速させています。

EcoFlow、Powerenz、Jackery、GROWATT、Bluetti、Nature's Generator、Inergy、HomeGrid、Aton Solar、PowerOak、Anern、Renogy、Humless、ACOPOWER、Milesolar、Goal Zero、Generac Power Systems、Lion Energy、Anker、OUPESなどの企業は、市場での地位を確保するために戦略的イニシアチブを展開しています。これには、大容量ポータブル・ユニットの開発、eコマース・チャネルの拡大、スマート・バッテリーのイノベーションの活用、カスタマーサービス・ネットワークの強化などが含まれます。多くのブランドは、流通パートナーシップの拡大と、多様な住宅ニーズに合わせたカスタマイズ可能なエネルギー・ソリューションの提供に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業の市場シェア分析

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 1,000W未満

- 1,000W~2,000W以上

- 2,000W~3,000W以上

- 3,000W以上

第6章 市場規模・予測:フェーズ別、2021年~2034年

- 主要動向

- 単相

- 三相

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- イタリア

- ポーランド

- オランダ

- オーストリア

- フランス

- スペイン

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- フィリピン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- ナイジェリア

- イスラエル

- ラテンアメリカ

- ブラジル

- チリ

- メキシコ

第8章 企業プロファイル

- ACOPOWER

- Anern

- Anker

- Aton Solar

- Bluetti

- EcoFlow

- Generac Power Systems

- Goal Zero

- GROWATT

- HomeGrid

- Humless

- Inergy

- Jackery

- Lion Energy

- Milesolar

- Nature's Generator

- OUPES

- Powerenz

- PowerOak

- Renogy

The Global Residential Solar Generator Market was valued at USD 465.3 million in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 1.26 billion by 2034, driven by the rising demand for clean, renewable energy solutions and increasing environmental awareness among homeowners. As the world shifts toward more sustainable energy options, solar generators are becoming a top choice for residential applications. The push for energy independence, along with the frequent instability in grid systems and increasing power disruptions, is accelerating this shift. Ongoing improvements in lithium-ion and solid-state battery technologies, as well as the integration of energy management systems in households, are enhancing the appeal of residential solar solutions. These advancements make solar generators more efficient, durable, and user-friendly.

Government policies focused on emission reductions and tax incentives for renewable adoption play a critical role. The ongoing adoption of smart home systems prioritizes energy savings and contributes to market expansion. Even with challenges like rising production costs and tariffs on imported components, the long-term outlook remains strong due to a growing focus on domestic manufacturing and innovation in the sector. Residential solar generators are also valued for their ability to reduce electricity bills and lower carbon footprints, making them an attractive investment for homeowners aiming to adopt cleaner energy sources.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $465.3 Million |

| Forecast Value | $1.26 Billion |

| CAGR | 10.4% |

Generators with power ratings between >1,000 W and 2,000 W generated USD 150 million in 2024, reflecting their growing importance in residential settings. These mid-range systems are particularly favored in areas facing recurrent power interruptions, offering homeowners a dependable and efficient backup power source without requiring significant infrastructure upgrades. Their compact size, combined with sufficient output for essential appliances, makes them ideal for small to medium-sized homes. This segment continues to gain traction as consumers seek cost-effective energy solutions that balance power capacity and portability.

The three-phase solar generator segment is set to experience robust growth, with projections indicating a CAGR of 10% through 2034. This trend is driven by a rising need for systems capable of handling larger electrical loads and integrating seamlessly with renewable energy frameworks. As more homes incorporate solar panels, electric vehicle charging stations, and energy management systems, the demand for three-phase configurations will grow. These generators are designed to support high-efficiency energy usage, making them essential in smart homes and larger residential setups where stability and scalability are crucial.

United States Residential Solar Generator Market was valued at USD 189.2 million in 2024, signaling strong momentum in one of the world's most advanced energy markets. With increasing power outages caused by extreme weather events and aging grid infrastructure, homeowners prioritize energy security more than ever. This shift encourages the adoption of solar-powered backup systems that provide off-grid reliability and long-term savings. U.S. government initiatives such as tax credits, rebates, and funding for clean energy projects are accelerating market penetration, particularly in states with high electricity costs and frequent outages.

Companies such as EcoFlow, Powerenz, Jackery, GROWATT, Bluetti, Nature's Generator, Inergy, HomeGrid, Aton Solar, PowerOak, Anern, Renogy, Humless, ACOPOWER, Milesolar, Goal Zero, Generac Power Systems, Lion Energy, Anker, and OUPES are deploying strategic initiatives to secure their market position. These include developing high-capacity, portable units, expanding e-commerce channels, leveraging smart battery innovations, and enhancing customer service networks. Many brands focus on expanding distribution partnerships and offering customizable energy solutions tailored to diverse residential needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiatives

- 4.4 Company market share analysis, 2024

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 1,000 W

- 5.3 > 1,000 W - 2,000 W

- 5.4 > 2,000 W - 3,000 W

- 5.5 > 3,000 W

Chapter 6 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Single phase

- 6.3 Three phase

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Poland

- 7.3.4 Netherlands

- 7.3.5 Austria

- 7.3.6 France

- 7.3.7 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Philippines

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.5.4 Egypt

- 7.5.5 Nigeria

- 7.5.6 Israel

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Chile

- 7.6.3 Mexico

Chapter 8 Company Profiles

- 8.1 ACOPOWER

- 8.2 Anern

- 8.3 Anker

- 8.4 Aton Solar

- 8.5 Bluetti

- 8.6 EcoFlow

- 8.7 Generac Power Systems

- 8.8 Goal Zero

- 8.9 GROWATT

- 8.10 HomeGrid

- 8.11 Humless

- 8.12 Inergy

- 8.13 Jackery

- 8.14 Lion Energy

- 8.15 Milesolar

- 8.16 Nature's Generator

- 8.17 OUPES

- 8.18 Powerenz

- 8.19 PowerOak

- 8.20 Renogy