食品加工用煙管コンデンシングボイラー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Condensing Fire-Tube Food Processing Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750573

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

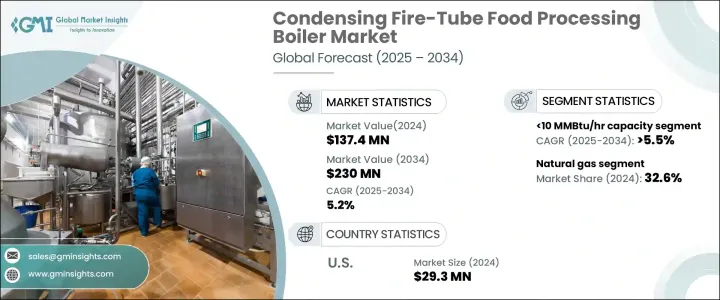

世界の食品加工用煙管コンデンシングボイラー市場は、2024年に1億3,740万米ドルと評価され、持続可能な加熱技術への注目の高まりと産業インフラの近代化により、CAGR 5.2%で成長し、2034年には2億3,000万米ドルに達すると予測されています。

排出物に対する懸念の高まりと、よりクリーンでエネルギー効率の高いシステムの必要性により、食品加工施設は高効率の煙管コンデンシングボイラーを採用するようになっています。これらのシステムは、一貫した熱出力を提供しながらエネルギー使用を最適化するよう設計されており、進化する環境規範と省エネルギー目標に合致しています。

市場は、老朽化したボイラーシステムの交換や強化を奨励する、より厳格な規制枠組みによってさらに推進されています。このような規制により、メーカーやプラント運営者は、コンプライアンスと性能の両方を重視した高度な加熱装置への投資を迫られています。また、食品製造において重要な要素である、信頼性の高い連続的な蒸気生産に対する需要の高まりも、最新のボイラー技術に対する需要を後押ししています。さらに、特に都市部や半都市部では、産業設備の拡大や近代化に伴い、コンパクトで費用対効果が高く、省エネルギーなソリューションに対するニーズが高まっており、復水式煙管ボイラーはこのニーズに対応できる立場にあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1億3,740万米ドル |

| 予測金額 | 2億3,000万米ドル |

| CAGR | 5.2% |

制御システム、遠隔監視、デジタル統合の革新は、運転効率の向上とダウンタイムの最小化に重要な役割を果たしています。スマート技術を取り入れることで、オペレーターはリアルタイムで性能を追跡し、問題を迅速に特定し、エネルギー消費を最適化することができます。これらの進歩により、高い生産性レベルを維持しながら二酸化炭素排出量の削減を目指す企業にとって、煙管コンデンシングボイラーは魅力的な選択肢となっています。

容量の面では、10 MMBtu/hrの能力を持つ食品加工用煙管コンデンシングボイラーは、2034年までに5.5%を超えるCAGRで成長すると予想されています。コンパクトな設置面積、設置の容易さ、高い運転効率により、旧式の非凝縮式ユニットからの置き換えに最適です。場所を取らずに信頼性が高く安定した性能を発揮するその能力は、大規模な空間再構成なしにアップグレードを検討している食品加工施設にとって特に魅力的です。

燃料タイプ別に区分すると、市場には天然ガス、石油、石炭、その他が含まれます。2024年には、天然ガス焚き部門が市場シェア全体の32.6%を占める。この分野は、優れたエネルギー効率、よりクリーンな燃焼、再生可能エネルギー源との互換性により、今後数年間で大きな成長が見込まれています。天然ガスへのシフトは、排出量の多い石炭・石油への依存を減らすという世界の関心の高まりにも支えられています。

米国では、食品加工用煙管コンデンシングボイラー市場は近年一貫した成長を見せています。2022年には2,610万米ドルに達し、2023年には2,760万米ドルに上昇、さらに2024年には2,930万米ドルに達しました。この上昇軌道は、よりクリーンな技術や省エネソリューションの採用を促進する政策主導の取り組みによるところが大きいです。米国および州レベルのプログラムは引き続き高効率機器の設置にインセンティブを与えており、食品製造ユニット全体で最新のコンデンシングボイラー・システムに対する需要を強化しています。

より広い北米地域全体では、市場は2034年までCAGR 4.7%以上の成長が見込まれています。気候変動に対する意識の高まりや、温室効果ガス排出削減に対する各地域の強いコミットメントといった要因が、エネルギー効率の高いボイラー技術の広範な導入を支えています。特に食品加工業界は、操業コストの削減と環境基準の遵守を優先しており、この2つは凝縮式煙管ボイラーが提供する利点と一致しています。

市場情勢は中程度に集約されており、上位5社で世界シェアの約40%を占めています。これらの主要プレーヤーは、製品革新、戦略的パートナーシップ、地理的拡大に注力し、競争の激しい環境での足場固めを行っています。食品加工における持続可能な加熱ソリューションへの需要が高まり続ける中、将来の動向形成におけるこれら市場リーダーの役割はますます重要になると思われます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 10 MMBtu/毎時未満

- 10~25 MMBtu/毎時

- 25~50 MMBtu/毎時

- 50~75 MMBtu/毎時

- 75~100 MMBtu/毎時

- 100~175 MMBtu/毎時

- 175~250 MMBtu/毎時

- 250 MMBtu/毎時以上

第6章 市場規模・予測:燃料別、2021年~2034年

- 主要動向

- 天然ガス

- 油

- 石炭

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Babcock and Wilcox

- Babcock Wanson

- BM GreenTech

- Bosch Industriekessel

- Clayton Industries

- Cleaver-Brooks

- Cochran

- Forbes Marshall

- Fulton

- Hoval

- Hurst Boiler

- Johnston Boiler

- Miura America

- Thermax

- Thermodyne Boilers

- Viessmann

目次

The Global Condensing Fire-Tube Food Processing Boiler Market was valued at USD 137.4 million in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 230 million by 2034, driven by the increasing focus on sustainable heating technologies and the modernization of industrial infrastructure. Growing concerns over emissions and the need for cleaner, more energy-efficient systems are leading food processing facilities to adopt high-efficiency condensing fire-tube boilers. These systems are engineered to optimize energy use while delivering consistent thermal output, aligning with evolving environmental norms and energy conservation goals.

The market is further propelled by stricter regulatory frameworks that encourage the replacement or enhancement of aging boiler systems. These regulations are pushing manufacturers and plant operators to invest in advanced heating units that are both compliant and performance-focused. The rising demand for reliable and continuous steam production, a critical component in food manufacturing, is also fueling the demand for modern boiler technologies. In addition, as industrial setups expand and modernize, particularly in urban and semi-urban regions, there is a growing need for compact, cost-effective, and energy-saving solutions-needs that condensing fire-tube boilers are well-positioned to meet.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $137.4 Million |

| Forecast Value | $230 Million |

| CAGR | 5.2% |

Innovations in control systems, remote monitoring, and digital integration are playing a crucial role in enhancing operational efficiency and minimizing downtime. The incorporation of smart technologies allows operators to track performance in real time, identify issues quickly, and optimize energy consumption. These advancements are making condensing fire-tube boilers an attractive option for businesses aiming to reduce their carbon footprint while maintaining high productivity levels.

In terms of capacity, condensing fire-tube food processing boilers with a 10 MMBtu/hr capacity are anticipated to grow at a CAGR exceeding 5.5% by 2034. Their compact footprint, ease of installation, and high operational efficiency make them an ideal replacement for older, non-condensing units. Their ability to deliver reliable and consistent performance without occupying much space is particularly appealing to food processing facilities looking to upgrade without major spatial reconfigurations.

When segmented by fuel type, the market includes natural gas, oil, coal, and others. In 2024, the natural gas-fired segment accounted for 32.6% of the total market share. This segment is expected to witness significant growth over the coming years due to its superior energy efficiency, cleaner combustion, and compatibility with renewable energy sources. The shift toward natural gas is also supported by the rising global focus on reducing dependence on coal and oil, both of which have higher emission footprints.

In the United States, the condensing fire-tube food processing boiler market has shown consistent growth in recent years. It reached USD 26.1 million in 2022, climbed to USD 27.6 million in 2023, and further rose to USD 29.3 million in 2024. This upward trajectory is largely attributed to policy-driven initiatives promoting the adoption of cleaner technologies and energy-saving solutions. Federal and state-level programs continue to incentivize the installation of high-efficiency equipment, reinforcing the demand for modern condensing boiler systems across food manufacturing units.

Across the broader North American region, the market is set to grow at a CAGR of more than 4.7% through 2034. Factors such as growing awareness of climate change, coupled with strong regional commitments to reducing greenhouse gas emissions, are supporting the widespread implementation of energy-efficient boiler technologies. The food processing industry, in particular, is prioritizing operational cost savings and compliance with environmental standards, both of which align with the benefits offered by condensing fire-tube boilers.

The market landscape is moderately consolidated, with the top five manufacturers collectively holding around 40% of the global share. These key players are focusing on product innovation, strategic partnerships, and geographic expansion to strengthen their foothold in a highly competitive environment. As demand for sustainable heating solutions in food processing continues to rise, the role of these market leaders in shaping future trends will become increasingly significant.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million, MMBTU/hr & Units)

- 5.1 Key trends

- 5.2 < 10 MMBtu/hr

- 5.3 10 - 25 MMBtu/hr

- 5.4 25 - 50 MMBtu/hr

- 5.5 50 - 75 MMBtu/hr

- 5.6 75 - 100 MMBtu/hr

- 5.7 100 - 175 MMBtu/hr

- 5.8 175 - 250 MMBtu/hr

- 5.9 > 250 MMBtu/hr

Chapter 6 Market Size and Forecast, By Fuel, 2021 - 2034 (USD Million, MMBTU/hr & Units)

- 6.1 Key trends

- 6.2 Natural gas

- 6.3 Oil

- 6.4 Coal

- 6.5 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, MMBTU/hr & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Russia

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Turkey

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Babcock and Wilcox

- 8.2 Babcock Wanson

- 8.3 BM GreenTech

- 8.4 Bosch Industriekessel

- 8.5 Clayton Industries

- 8.6 Cleaver-Brooks

- 8.7 Cochran

- 8.8 Forbes Marshall

- 8.9 Fulton

- 8.10 Hoval

- 8.11 Hurst Boiler

- 8.12 Johnston Boiler

- 8.13 Miura America

- 8.14 Thermax

- 8.15 Thermodyne Boilers

- 8.16 Viessmann

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日