|

市場調査レポート

商品コード

1750565

ジェネレーティブAI市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Generative AI Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ジェネレーティブAI市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年05月14日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

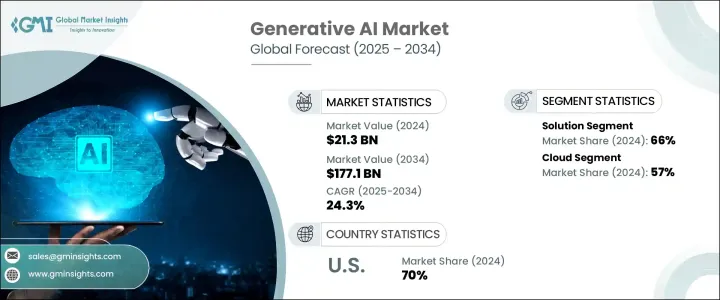

ジェネレーティブAIの世界市場規模は、2024年に213億米ドルとなり、CAGR 24.3%で成長し、2034年には1,771億米ドルに達すると予測されています。

マーケティング、メディア、eコマースなどの分野でコンテンツ自動生成の需要が高まっていることが、この成長を後押ししています。ジェネレーティブAIを利用することで、企業はテキスト、画像、動画、音声など、パーソナライズされたコンテンツを効率的かつ大規模に作成し、制作時間とコストを削減することができます。このような関心の高まりは、デジタル・インタラクションや迅速なコンテンツ配信に大きく依存する業界で特に顕著です。

ディープラーニングアルゴリズム、トランスフォーマーアーキテクチャ、クラウドコンピューティングリソースの利用可能性における技術的進歩は、ジェネレーティブAIの開発を大幅に加速させました。GPTやDALL-EのようなAIモデルはより効率的で強力になりつつあり、企業はこれらの技術を創造的で分析的なタスクに使用できるようになっています。AIの処理能力が向上するにつれて、リアルタイムのコンテンツ生成がますます可能になり、企業はジェネレーティブAIをワークフローに組み込むことができます。このテクノロジーは、顧客サービス、レポート作成、コード作成、製品設計を合理化することで、業界全体のデジタルトランスフォーメーションをサポートします。その結果、効率性の向上、イノベーションの促進、運用コストの削減が可能になり、ジェネレーティブAIは先進的な企業にとって重要な投資となります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 213億米ドル |

| 予測金額 | 1,771億米ドル |

| CAGR | 24.3% |

2024年のジェネレーティブAI市場は、ソリューション分野が市場シェアの約66%を占め、圧倒的な強さを見せた。この優位性は、AIプラットフォームやツールが業界全体で広く使用され、アプリケーション主導の具体的な利益をもたらしていることによる。ジェネレーティブAIソリューションには、コンテンツ作成、画像生成、バーチャルアシスタント、コード生成、データ強化などのAIソフトウェアが含まれます。企業は、スケーラブルで、事前にトレーニングされ、統合が容易で、社内のAI専門知識を最小限に抑えたエンドツーエンドのソリューションをますます求めるようになっています。ヘルスケア、マーケティング、金融、デザインなどの業界でジェネレーティブAIアプリケーションの需要が高まるにつれ、カスタマイズ可能な既製のプラットフォームが人気を博しています。

クラウド展開もジェネレーティブAI市場に大きく貢献しています。クラウドセグメントは、その拡張性、手頃な価格、容易な展開により、2024年には57%のシェアを占めています。ジェネレーティブAIモデルのトレーニングや推論の計算量は、ハイエンドのGPUやTPUを提供するクラウドプラットフォームによって効率的に処理されます。クラウドベースのプラットフォームは、リアルタイムの処理、ライブアップデート、他のAIツールとの統合を提供するため、企業は大規模な言語モデルや画像ジェネレータのような強力な生成モデルに、大規模なインフラ投資を行うことなくアクセスすることができます。

米国のジェネレーティブAI市場は70%のシェアを占め、2024年には47億米ドルを生み出しました。同国の優位性は、強力なAIイノベーション、ハイテク大手の高集中、多額のベンチャーキャピタル投資によってもたらされます。米国はまた、倫理的なAI開発と規制の枠組みでもリードしており、ジェネレーティブAIの進歩と商業的成功のハブとなっています。

ジェネレーティブAI業界の主要プレーヤーには、Adobe、NVIDIA、Amazon Web Services(AWS)、Microsoft、Meta、IBM、Google LLC、Autodesk、Baidu、Lighttricksなどがいます。市場ポジションを強化するため、ジェネレーティブAI分野の企業はいくつかの戦略的イニシアティブに注力しています。これには、拡張性を高めるためのクラウドサービスプロバイダーとのパートナーシップの拡大、AIモデルの効率性を高めるための研究開発への投資、多様な顧客ニーズに対応するための業界特化型AIソリューションの開発などが含まれます。さらに、大手企業は最先端の技術を統合し、急速に進化する市場で競争力を維持できるようにするため、買収や提携を模索しています。カスタマイズ可能なAIプラットフォームを提供し、既存の企業システムに容易に統合できるようにすることは、企業が存在感を確固たるものにするための重要な戦略です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- クラウドインフラストラクチャプロバイダー

- ファンデーションモデル開発者

- プラットフォームプロバイダー

- ソフトウェアプロバイダー

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 他国による報復措置

- 業界への影響

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- ユースケース

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- コンテンツ自動化の需要の高まり

- AIとコンピューティングインフラの進歩

- 企業のデジタル変革イニシアチブ

- マルチモーダルアプリケーションの成長

- 業界の潜在的リスク&課題

- 誤情報と倫理的誤用のリスク

- データの品質と偏り

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- サービス

第6章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- クラウド

- オンプレミス

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 生成的敵対ネットワーク(GAN)

- トランスフォーマーモデル

- 変分オートエンコーダ

- 拡散モデル

- その他

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- ヘルスケア

- 小売業とeコマース

- 製造業

- BFSI

- メディアとエンターテイメント

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Adobe

- Amazon Web Services(AWS)

- Apple

- Autodesk

- Baidu

- DeepMind

- Genie AI

- IBM

- Intel

- Meta

- Microsoft

- MOSTLY AI

- NVIDIA

- OpenAI

- Oracle

- Salesforce

- Siemens

- Synthesia

- Uber AI

- Unity Technologies

The Global Generative AI Market was valued at USD 21.3 billion in 2024 and is estimated to grow at a CAGR of 24.3% to reach USD 177.1 billion by 2034, driven by the increasing demand for automated content generation across sectors such as marketing, media, and e-commerce is driving this growth. Generative AI allows businesses to create personalized content, including text, images, video, and audio, efficiently and at scale, while reducing production time and costs. This surge in interest is particularly pronounced in industries heavily reliant on digital interaction and quick content distribution.

Technological advancements in deep learning algorithms, transformer architectures, and the availability of cloud computing resources have significantly accelerated the development of generative AI. AI models like GPT and DALL-E are becoming more efficient and powerful, enabling companies to use these technologies for creative and analytical tasks. As AI processing capabilities improve, real-time content generation becomes increasingly feasible, helping organizations integrate generative AI into their workflows. This technology supports digital transformation across industries by streamlining customer service, report generation, code creation, and product design. As a result, businesses can improve efficiency, foster innovation, and reduce operational costs, positioning generative AI as a critical investment for forward-thinking companies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Billion |

| Forecast Value | $177.1 Billion |

| CAGR | 24.3% |

In 2024, the solutions segment dominated the generative AI market, accounting for around 66% of the market share. This dominance is due to the widespread use of AI platforms and tools across industries, which deliver tangible, application-driven benefits. Generative AI solutions encompass AI software for content creation, image generation, virtual assistance, code generation, and data enhancement. Enterprises are increasingly looking for end-to-end solutions that are scalable, pre-trained, and easy to integrate, requiring minimal in-house AI expertise. As the demand for generative AI applications grows across industries like healthcare, marketing, finance, and design, customizable, off-the-shelf platforms have gained popularity.

Cloud deployment is also a major contributor to the generative AI market. The cloud segment accounted for 57% share in 2024 due to its scalability, affordability, and easy deployment. The computational intensity of training and inference for generative AI models is efficiently handled by cloud platforms that offer high-end GPUs and TPUs. Cloud-based platforms provide real-time processing, live updates, and integration with other AI tools, allowing organizations to access powerful generative models like large language models and image generators without heavy infrastructure investments.

United States Generative AI Market held a 70% share and generated USD 4.7 billion in 2024. The country's dominance is driven by strong AI innovation, a high concentration of tech giants, and significant venture capital investment. The U.S. also leads in ethical AI development and regulatory frameworks, making it a hub for generative AI advancement and commercial success.

Key players in the generative AI industry include Adobe, NVIDIA, Amazon Web Services (AWS), Microsoft, Meta, IBM, Google LLC, Autodesk, Baidu, and Lighttricks. To strengthen their market position, companies in the generative AI space focus on several strategic initiatives. These include expanding partnerships with cloud service providers to enhance scalability, investing in R&D to improve AI model efficiency, and developing industry-specific AI solutions to address diverse customer needs. Moreover, leading firms are exploring acquisitions and collaborations to integrate cutting-edge technologies, enabling them to stay competitive in a rapidly evolving market. Offering customizable AI platforms and ensuring easy integration into existing enterprise systems are key strategies helping businesses solidify their presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Cloud infrastructure providers

- 3.2.2 Foundational model developers

- 3.2.3 Platform providers

- 3.2.4 Software providers

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Use cases

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising demand for content automation

- 3.10.1.2 Advancements in AI and computing infrastructure

- 3.10.1.3 Enterprise digital transformation initiatives

- 3.10.1.4 Growth in multimodal applications

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Risk of misinformation and ethical misuse

- 3.10.2.2 Data quality and bias

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.3 Service

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premises

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Generative adversarial networks (GANs)

- 7.3 Transformers model

- 7.4 Variational auto-encoders

- 7.5 Diffusion models

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Healthcare

- 8.3 Retail and e-commerce

- 8.4 Manufacturing

- 8.5 BFSI

- 8.6 Media and entertainment

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Adobe

- 10.2 Amazon Web Services (AWS)

- 10.3 Apple

- 10.4 Autodesk

- 10.5 Baidu

- 10.6 DeepMind

- 10.7 Genie AI

- 10.8 Google

- 10.9 IBM

- 10.10 Intel

- 10.11 Meta

- 10.12 Microsoft

- 10.13 MOSTLY AI

- 10.14 NVIDIA

- 10.15 OpenAI

- 10.16 Oracle

- 10.17 Salesforce

- 10.18 Siemens

- 10.19 Synthesia

- 10.20 Uber AI

- 10.21 Unity Technologies