車載アプリ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

In-Vehicle Apps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750562

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

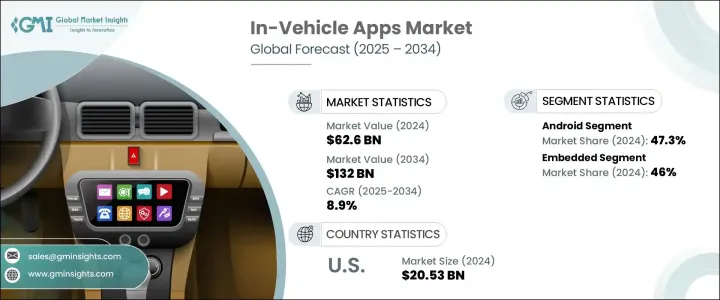

車載アプリの世界市場規模は、2024年に626億米ドルとなり、自動車技術の急速な進歩と電気自動車や自律走行車の普及の高まりにより、CAGR 8.9%で成長し、2034年には1,320億米ドルに達すると予測されています。

これらの次世代自動車は、ナビゲーション、エネルギー効率、運転支援などを管理するソフトウェア・エコシステムへの依存度を高めています。その結果、ユーザーエクスペリエンスの向上、機能性の改善、継続的なコネクティビティの提供を目指す自動車メーカーにとって、車載アプリケーションは不可欠なものとなりつつあります。スマート・モビリティ・ソリューションとリアルタイム・サービスの自動車への統合が重視されるようになったことで、ドライバーと自動車との関わり方が変化し、利便性、安全性、パーソナライゼーションを優先したアプリ中心の体験が促進されています。

自動車メーカーは、車内でのインタラクションを向上させるため、HDタッチスクリーン、AIを活用した音声コントロール、高速接続をサポートする、よりスマートなインフォテインメント・プラットフォームへの投資を進めています。強化されたオペレーティングシステムとデバイス間のシームレスな同期により、これらのプラットフォームは、ユーザーフレンドリーなインターフェイス内でナビゲーション、メディアアクセス、診断、車両制御を提供する機能豊富なアプリを後押ししています。消費者は、スマートフォンやタブレットから得られるのと同じ流動的なデジタル体験を車内でも求めているため、こうしたソリューションへの需要が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 626億米ドル |

| 予測金額 | 1,320億米ドル |

| CAGR | 8.9% |

Androidベースの車載プラットフォームセグメントは2024年に47.3%のシェアを占め、このセグメントは2034年までCAGR 9.5%で成長すると予測されます。その魅力は、自動車メーカーがカスタマイズ可能で拡張性の高いインフォテインメント・エコシステムを構築できる、Androidのオープンソースの柔軟性にあります。このアプローチは、幅広いサードパーティのサービスやアプリケーションとの統合をサポートし、ドライバーがさまざまな価格セグメントやモデルでナビゲーション、音楽、音声アシスタント、リアルタイムの車両データにアクセスできるようにします。自動車メーカー各社は、進化する消費者の需要にマッチした、没入感のあるパーソナライズされた体験を作り上げるために、Androidへの傾倒を強めています。

コネクティビティ技術別に分類すると、組み込みシステム・セグメントは2024年に46%のシェアを占める。これらの組み込みアプリケーションは、外部のスマートフォンやモバイル機器とは独立して機能するため、あらゆる運転状況において高い信頼性を発揮します。内蔵アプリケーションは、車両のハードウェアや内部ネットワークと直接統合することで、安全警告、ルート案内、システム診断などの中核機能への一貫したアクセスを提供します。

米国の車載アプリ市場は、成熟した自動車産業、ハイテク・インフラ、コネクテッド・ビークル機能に対する需要が引き続きイノベーションと普及を促進するため、2024年には85.6%のシェアを占め、205億3,000万米ドルを創出しました。主要な自動車OEM企業、ハイテク企業、ソフトウェア開発者の強力なプレゼンスが、迅速な製品開発と展開のための協力的な環境を育んでいます。米国市場は、高度なインフォテインメント、スマートフォンのシームレスな統合、車両内のリアルタイム・デジタル・サービスに対する消費者の高い期待から恩恵を受けています。

現代自動車、アップル、マイクロソフト、Harman International Industries、Nvidia、Garmin、トヨタ自動車、NXPセミコンダクターズ、ゼネラルモーターズ、グーグルなど、車載アプリ世界市場の主要企業は、市場の足場を固めるためにいくつかの主要戦略に注力しています。これには、OEMとの提携、AIとクラウドサービスの統合、ユーザー体験を向上させる独自OSの開発などが含まれます。各社はまた、アプリのエコシステムを拡大し、ユーザー・インターフェース・デザインに投資し、モビリティ新興企業との協業を進めることで、動向を先取りし、競争の激しい環境で差別化された拡張可能なソリューションを提供しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- アプリ開発者

- プラットフォームプロバイダー

- 接続プロバイダー

- テクノロジープロバイダー

- メディアおよびコンテンツプロバイダー

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 車両アプリの統計

- 車両普及率統計

- アプリケーションの使用状況統計

- ユーザー行動エンゲージメント

- 接続性とデータ使用量

- 規制情勢

- 影響要因

- 促進要因

- 電気自動車と自動運転車の台頭

- インフォテインメントシステムの技術的進歩

- 接続性に対する消費者の需要の高まり

- 車両の安全性と促進要因支援の必要性の高まり

- 業界の潜在的リスク&課題

- 促進要因の注意散漫と安全上の懸念

- データのプライバシーとセキュリティ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 軽作業

- 中型

- ヘビーデューティー

第6章 市場推計・予測:オペレーティングシステム別、2021年~2034年

- 主要動向

- iOS

- Android

- Windows

- その他

第7章 市場推計・予測:コネクティビティテクノロジー別、2021年~2034年

- 主要動向

- 埋め込み

- テザリング型

- 統合型

第8章 市場推計・予測:アプリ別、2021年~2034年

- 主要動向

- インフォテインメントアプリ

- ナビゲーションアプリ

- テレマティクスアプリ

- 安全アプリ

- コミュニケーションアプリ

- 車両制御アプリ

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Alcatel-Lucent

- Apple

- Audi

- Continental

- Elektrobit Automotive

- Ford Motor Company

- Garmin

- General Motors

- Harman International Industries

- Hyundai Motor Company

- Microsoft

- Nvidia

- NXP Semiconductors

- Renesas Electronics

- Robert Bosch

- Siemens

- Tesla

- TomTom

- Toyota Motor

目次

The Global In-Vehicle Apps Market was valued at USD 62.6 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 132 billion by 2034, driven by the rapid advancements in automotive technology, coupled with the rising adoption of electric and autonomous vehicles. These next-gen vehicles are increasingly reliant on software ecosystems to manage navigation, energy efficiency, driver assistance, and more. As a result, in-vehicle applications are becoming indispensable for automakers looking to enhance user experience, improve functionality, and offer continuous connectivity. The growing emphasis on smart mobility solutions and the integration of real-time services into vehicles is transforming how drivers interact with their cars, promoting app-centric experiences that prioritize convenience, safety, and personalization.

Automakers are investing in smarter infotainment platforms that support HD touchscreens, AI-powered voice controls, and high-speed connectivity to elevate in-car interactions. With enhanced operating systems and seamless synchronization across devices, these platforms are powering feature-rich apps that offer navigation, media access, diagnostics, and vehicle control within a user-friendly interface. The demand for these solutions is increasing as consumers expect the same fluid digital experience inside their cars that they get from their smartphones and tablets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $62.6 Billion |

| Forecast Value | $132 Billion |

| CAGR | 8.9% |

The Android-based in-vehicle platforms segment held a 47.3% share in 2024, and this segment is expected to grow at a CAGR of 9.5% through 2034. The appeal lies in Android's open-source flexibility, which allows car manufacturers to build customizable and scalable infotainment ecosystems. This approach supports integration with a broad range of third-party services and applications, enabling drivers to access navigation, music, voice assistants, and real-time vehicle data across various price segments and models. Automakers are increasingly leaning toward Android to craft immersive, personalized experiences that match evolving consumer demands.

When categorized by connectivity technology, the embedded systems segment held a 46% share in 2024. These built-in applications function independently of external smartphones or mobile devices, which makes them highly reliable in all driving conditions. By integrating directly with the vehicle's hardware and internal network, embedded apps offer consistent access to core features like safety alerts, route guidance, and system diagnostics-even in areas with limited or no internet connectivity.

United States In-Vehicle Apps Market held 85.6% share and generated USD 20.53 billion in 2024 as the country's mature auto industry, high-tech infrastructure, and demand for connected vehicle features continue to propel innovation and adoption. The strong presence of leading automotive OEMs, tech companies, and software developers fosters a collaborative environment for rapid product development and deployment. The U.S. market benefits from high consumer expectations for advanced infotainment, seamless smartphone integration, and real-time digital services in vehicles.

Leading players in the Global In-Vehicle Apps Market, including Hyundai Motor Company, Apple, Microsoft, Harman International Industries, Nvidia, Garmin, Toyota Motor, NXP Semiconductors, General Motors, and Google, are focused on several key strategies to reinforce their market foothold. These include partnerships with OEMs, integration of AI and cloud services, and development of proprietary operating systems to enhance user experience. Companies are also expanding their app ecosystems, investing in user interface design, and collaborating with mobility startups to stay ahead of trends and offer differentiated, scalable solutions in a highly competitive environment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 App developers

- 3.2.2 Platform providers

- 3.2.3 Connectivity providers

- 3.2.4 Technology providers

- 3.2.5 Media and content providers

- 3.2.6 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Vehicle apps statistics

- 3.8.1 Vehicle penetration statistics

- 3.8.2 Application usage statistics

- 3.8.3 User behavior engagement

- 3.8.4 Connectivity and data usage

- 3.9 Regulatory landscape

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rise of electric and autonomous vehicles

- 3.10.1.2 Technological advancements in infotainment systems

- 3.10.1.3 Growing consumer demand for connectivity

- 3.10.1.4 Increasing need for vehicle safety and driver assistance

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Driver distractions and safety concerns

- 3.10.2.2 Data privacy and security

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

Chapter 6 Market Estimates & Forecast, By Operating System, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 iOS

- 6.3 Android

- 6.4 Windows

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Connectivity Technology, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Embedded

- 7.3 Tethered

- 7.4 Integrated

Chapter 8 Market Estimates & Forecast, By App, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Infotainment apps

- 8.3 Navigation apps

- 8.4 Telematics apps

- 8.5 Safety apps

- 8.6 Communication apps

- 8.7 Vehicle control apps

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Alcatel-Lucent

- 10.2 Apple

- 10.3 Audi

- 10.4 Continental

- 10.5 Elektrobit Automotive

- 10.6 Ford Motor Company

- 10.7 Garmin

- 10.8 General Motors

- 10.9 Google

- 10.10 Harman International Industries

- 10.11 Hyundai Motor Company

- 10.12 Microsoft

- 10.13 Nvidia

- 10.14 NXP Semiconductors

- 10.15 Renesas Electronics

- 10.16 Robert Bosch

- 10.17 Siemens

- 10.18 Tesla

- 10.19 TomTom

- 10.20 Toyota Motor

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日