ペット用糖尿病ケア機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Pet Diabetes Care Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750545

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

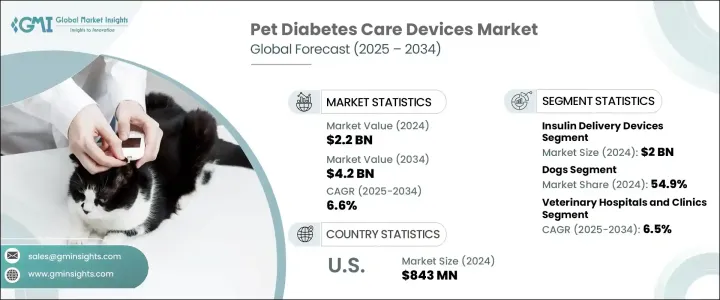

ペット用糖尿病ケア機器の世界市場は、2024年には22億米ドルと評価され、ペット飼育の増加、獣医ヘルスケアにおける技術進歩、動物ヘルスケアへの支出増加などを背景に、CAGR 6.6%で成長し、2034年には42億米ドルに達すると予測されています。

ペットの飼育率が上昇を続ける中、ペットの糖尿病などの慢性疾患を管理する必要性を認識する飼い主が増えています。ペットの肥満の蔓延、ペットの高齢化、座りがちなライフスタイルが糖尿病患者の急増に寄与しているため、モニタリングと治療ソリューションの需要が増加しています。ペットの健康と福祉が飼い主の最優先事項になるにつれ、糖尿病などの慢性疾患の管理に重点が置かれるようになり、今後も市場の拡大が予想されます。

技術の進歩により、ペットの糖尿病管理に役立つグルコース・モニターやインスリン・ポンプなどの機器の入手性が向上しています。こうした革新的な製品の開発は、獣医師や飼い主がより良いケアとより効果的な治療を提供するのに役立っています。ペットの糖尿病が、特に高齢や肥満の動物でより一般的になるにつれて、効果的な管理ソリューションへの需要が高まっています。この動向は、先進地域における可処分所得の増加によって支えられており、ペットの飼い主は先進ヘルスケア機器に投資する傾向が強いです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 22億米ドル |

| 予測金額 | 42億米ドル |

| CAGR | 6.6% |

市場は、インスリン送達デバイスとグルコースモニタリングデバイスの2つの主要セグメントに分けられます。2024年には、インスリン送達デバイスが最大の市場シェアを占め、20億米ドルと評価されました。このセグメントはさらに、ペットの糖尿病管理に不可欠なインスリン注射器とインスリンペンに分けられます。ペットの糖尿病はしばしば生涯にわたるインスリン療法を必要とすることから、インスリン送達デバイスは効果的な治療を保証するために極めて重要です。これらのデバイスは広く入手可能であり、価格も手ごろであるため、市場での優位性を確固たるものとしており、成長の主要な促進要因となっています。

ペット用糖尿病ケア機器市場はさらに動物の種類別に区分され、犬、猫、馬が主要なカテゴリーです。犬セグメントは2024年に54.9%のシェアを占めています。肥満、加齢、遺伝的要因によって犬の糖尿病有病率が高いため、糖尿病管理デバイスの最も一般的な受け手となっています。ペットの飼い主は、愛犬の健康管理の重要性をますます認識するようになっており、グルコースモニターやインスリン送達システムのような専用デバイスの採用が増加しています。

北米のペット用糖尿病ケア機器市場は2024年に41%のシェアを占めたが、これは同地域全体のペット飼育率の高さ、ペットの糖尿病管理の重要性に関する飼い主の意識の高まりなど、いくつかの要因によるものです。動物の積極的な健康管理の重要性を認識する飼い主が増えたことで、グルコースモニターやインスリン送達システムといった特殊なケア機器の需要が急増しています。その他の特典として、北米は獣医学のインフラがしっかりしており、数多くの動物病院やクリニックが、ペットの糖尿病などの症状を診断・治療するための最先端技術を提供しています。

ペット用糖尿病ケア機器世界市場の主要企業は、製品の革新、戦略的パートナーシップ、流通チャネルの拡大といった戦略を積極的に採用し、存在感を高めています。Zoetis社、Merck Animal Health社、Becton, Dickinson and Company社などの企業は、ペットの飼い主の進化するニーズに応える新製品を投入するために研究開発に投資しています。さらに、i-SENSやTaiDocなどの企業は、より幅広い顧客層に対応するため、糖尿病管理機器の入手しやすさと価格の向上に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ペット糖尿病の罹患率の上昇

- ペットヘルスケア費の増加

- ペットの肥満の増加

- 血糖モニタリングにおける技術的進歩

- 業界の潜在的リスク&課題

- デバイスに関連する高コスト

- 新興国における認知度とアクセスの限界

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーの情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:デバイスタイプ別、2021 –2034

- 主要動向

- インスリン送達装置

- インスリン注射器

- インスリン注入ペン

- 血糖値モニタリング装置

- 血糖値モニター(BGM)

- 持続血糖モニター(CGM)

第6章 市場推計・予測:動物の種類別、2021 –2034

- 主要動向

- 犬

- 猫

- 馬

第7章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 動物病院および診療所

- 在宅ケアの設定

- その他の用途

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Allison Medical

- ALR Technologies

- Becton、Dickinson and Company

- Boehringer Ingelheim

- FitBark

- Henry Schein Animal Health

- Merck Animal Health

- TaiDoc

- Ulticare

- Zoetis

目次

The Global Pet Diabetes Care Devices Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 4.2 billion by 2034, driven by the increasing adoption of pets, technological advancements in veterinary healthcare, and rising expenditure on animal healthcare. As pet ownership continues to rise, more owners are becoming aware of the need for managing chronic conditions like diabetes in pets. The growing prevalence of pet obesity, the aging pet population, and sedentary lifestyles contribute to the surge in cases of diabetes, thus increasing demand for monitoring and treatment solutions. As pets' health and well-being become a top priority for owners, the focus on managing chronic conditions such as diabetes is expected to continue to expand the market.

Technological advancements have improved the availability of devices such as glucose monitors and insulin pumps, which help manage diabetes in pets. The development of these innovative products has helped veterinarians and pet owners provide better care and more effective treatments. As diabetes among pets becomes more common, especially in aging or obese animals, the demand for effective management solutions grows. This trend is supported by higher disposable income in developed regions, where pet owners are more likely to invest in advanced healthcare devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $4.2 Billion |

| CAGR | 6.6% |

The market is divided into two main segments: insulin delivery devices and glucose monitoring devices. In 2024, insulin delivery devices held the largest market share, valued at USD 2 billion. This segment is further divided into insulin syringes and insulin pens, which are essential for managing diabetes in pets. Given that diabetes in pets often requires lifelong insulin therapy, insulin delivery devices are crucial for ensuring effective treatment. The widespread availability and affordability of these devices have solidified their dominance in the market, providing a key driver for growth.

The pet diabetes care devices market is further segmented by animal type, with dogs, cats, and horses being the primary categories. The dogs segment held a 54.9% share in 2024. The higher prevalence of diabetes in dogs, driven by obesity, aging, and genetic factors, makes them the most common recipients of diabetes management devices. Pet owners are increasingly aware of the importance of managing their dogs' health, leading to an uptick in the adoption of specialized devices like glucose monitors and insulin delivery systems.

North American Pet Diabetes Care Devices Market held a 41% share in 2024, attributed to several factors, including the high rate of pet ownership across the region and a growing awareness among pet owners regarding the importance of diabetes management for their pets. With more individuals recognizing the significance of proactive health management for their animals, demand for specialized care devices such as glucose monitors and insulin delivery systems has surged. Additionally, North America benefits from a robust veterinary infrastructure, with numerous veterinary clinics and hospitals offering state-of-the-art technologies for diagnosing and treating conditions like diabetes in pets.

Key players in the Global Pet Diabetes Care Devices Market are actively employing strategies like product innovation, strategic partnerships, and expanding their distribution channels to strengthen their presence. Companies like Zoetis, Merck Animal Health, and Becton, Dickinson and Company are investing in research and development to introduce new products that cater to the evolving needs of pet owners. In addition, firms such as i-SENS and TaiDoc are focusing on enhancing the accessibility and affordability of diabetes management devices to cater to a broader customer base.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of pet diabetes

- 3.2.1.2 Increasing pet healthcare expenditure

- 3.2.1.3 Growing incidence of obesity in pets

- 3.2.1.4 Technological advancements in glucose monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with devices

- 3.2.2.2 Limited awareness and access in emerging countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Device Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Insulin delivery devices

- 5.2.1 Insulin syringes

- 5.2.2 Insulin delivery pen

- 5.3 Glucose monitoring devices

- 5.3.1 Blood glucose monitors (BGMs)

- 5.3.2 Continuous glucose monitors (CGMs)

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Horses

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Veterinary hospitals and clinics

- 7.3 Homecare settings

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Allison Medical

- 9.2 ALR Technologies

- 9.3 Becton, Dickinson and Company

- 9.4 Boehringer Ingelheim

- 9.5 FitBark

- 9.6 Henry Schein Animal Health

- 9.7 Merck Animal Health

- 9.8 TaiDoc

- 9.9 Ulticare

- 9.10 Zoetis

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日