|

市場調査レポート

商品コード

1750540

カプノグラフィデバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Capnography Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| カプノグラフィデバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月09日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

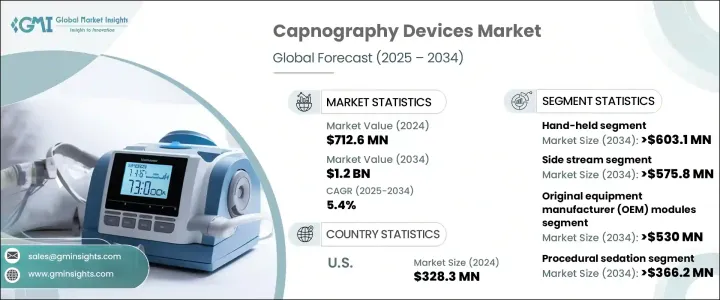

カプノグラフィデバイスの世界市場規模は、2024年に7億1,260万米ドルとなり、呼吸器疾患の罹患率の上昇、クリティカルケアや救急現場での使用の増加、低侵襲処置への嗜好の高まりなど、いくつかの要因によってCAGR 5.4%で成長し、2034年には12億米ドルに達すると予測されています。

また、カプノグラフィデバイスの採用は、患者の鎮静時に使用を義務付ける規制や、ヘルスケアにおける先進技術の採用という継続的な動向も後押ししています。さらに、携帯型カプノグラフィ装置に対する需要の高まりにより、これらの装置は外来診療所、救急医療サービス、病院以外の環境に適しており、市場の成長をさらに後押ししています。

カプノグラフィデバイスの需要は、呼気中の二酸化炭素(CO2)濃度をモニターする能力に関連しており、これは麻酔やクリティカルケア処置中の患者の安全を確保するために極めて重要です。これらの機器はリアルタイムのモニタリングに不可欠であり、ヘルスケアプロバイダーは呼吸器系の問題を早期に発見し、効果的に対応することができます。市場の成長は、患者中心のケアへの注目の高まりと、これらの機器の精度と使いやすさを向上させる技術の進歩によっても支えられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億1,260万米ドル |

| 予測金額 | 12億米ドル |

| CAGR | 5.4% |

ハンドヘルド分野は、CAGR 5%で成長し、2034年までに6億310万米ドルの予測値で大きく貢献する見込みです。ハンドヘルドは携帯性に優れ、病院前や外来での使用に最適です。これらのデバイスにより、ヘルスケアプロバイダーは、鎮静や呼吸モニタリングが必要な処置中に、迅速かつ十分な情報に基づいた意思決定を行うことができ、患者の安全が確保されます。さらに、マルチパラメータシステムよりも費用対効果が高いため、予算重視のヘルスケア現場で人気があります。

コンポーネント別では、OEM(相手先ブランド製造)モジュールがCAGR 5.1%で成長する見込みです。これらのモジュールはマルチパラメータシステムに統合され、ヘルスケア施設が診断能力を強化するための費用対効果の高い方法を提供します。コンパクトな設計で他のプラットフォームと統合できるため、さまざまなヘルスケア環境に適応できます。相互運用性と個別ケアの必要性が、OEMモジュールの需要を押し上げ続けており、世界中の病院や診断センターで支持を集めています。

米国のカプノグラフィデバイス市場は、2024年に3億2,830万米ドルと評価され、今後も上昇基調が続くと予想されています。この背景には、麻酔や処置鎮静におけるカプノグラフィの要件など、強力な規制支援があります。さらに、外来手術や病院前のケアにおけるカプノグラフィの採用拡大も米国での市場拡大に寄与しています。

世界カプノグラフィデバイス市場の主要企業には、ZOLL Medical社、Medtronic社、Philips Healthcare社、Masimo Corporation社、Becton, Dickinson and Company社などがあります。これらの企業は、戦略的提携、製品イノベーション、より先進的でポータブルかつコスト効率の高いソリューションの提供を通じて、市場での地位を強化しています。患者の安全性向上と使いやすさを求める顧客ニーズに注力することで、これらの企業は市場での存在感を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 低侵襲手術の増加

- 呼吸器疾患の増加

- 酸素濃度計よりもカプノメーターが好まれる傾向

- 最近の技術進歩と政府の好ましい取り組み

- 整形手術の増加

- 業界の潜在的リスク&課題

- 熟練した専門家の不足

- デバイスの高コスト

- 厳格な規制ガイドライン

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーの情勢

- ギャップ分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 手持ち式

- スタンドアロン

- マルチパラメータ

第6章 市場推計・予測:技術別、2021-2034

- 主要動向

- 副流

- 主流

- マイクロストリーム

第7章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- OEMモジュール

- その他のコンポーネント

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- 処置鎮静

- 救急医療

- 集中治療

- 疼痛管理

- その他の用途

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Becton、Dickinson and Company

- Criticare Systems

- Dragerwerk

- Edan Instruments

- Infinium Medical

- Masimo Corporation

- Medtronic

- Mindray Medical

- Nihon Kohden

- Nonin Medical

- Phillips Healthcare

- Shenzhen Comen Medical Instruments

- Smiths Medical

- ZOLL Medical

The Global Capnography Devices Market was valued at USD 712.6 million in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 1.2 billion by 2034, driven by several factors, including the rising incidence of respiratory diseases, increased use in critical care and emergency settings, and the growing preference for minimally invasive procedures. The adoption of capnography devices is also fueled by regulations that require their use during patient sedation, along with the ongoing trend of adopting advanced technologies in healthcare. Additionally, the increased demand for portable capnography units has made these devices suitable for outpatient clinics, emergency medical services, and non-hospital environments, further propelling market growth.

The demand for capnography devices is linked to their ability to monitor carbon dioxide (CO2) levels in exhaled breath, which is crucial for ensuring patient safety during anesthesia and critical care procedures. These devices are essential for real-time monitoring, allowing healthcare providers to detect respiratory issues early and respond effectively. The market's growth is also supported by the increasing focus on patient-centered care and technological advancements that improve the accuracy and ease of use of these devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $712.6 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 5.4% |

The handheld segment is expected to grow at a 5% CAGR and contribute significantly with a projected value of USD 603.1 million by 2034. Handheld capnography devices are favored for their portability, making them ideal for use in pre-hospital care and ambulatory settings. These devices allow healthcare providers to make quick, informed decisions during procedures that require sedation or respiratory monitoring, ensuring patient safety. Moreover, their cost-effectiveness over multi-parameter systems drives their popularity in budget-conscious healthcare settings.

Based on components, OEM (Original Equipment Manufacturer) modules are expected to grow at a CAGR of 5.1%. These modules are integrated into multi-parameter systems, offering a cost-effective way for healthcare facilities to enhance their diagnostic capabilities. Their compact design and ability to integrate with other platforms make them highly adaptable for various healthcare environments. The need for interoperability and personalized care continues to push the demand for OEM modules, which are gaining traction in hospitals and diagnostic centers worldwide.

U.S. Capnography Devices Market was valued at USD 328.3 million in 2024 and is expected to continue its upward trajectory. This is due to strong regulatory support, including the requirement for capnography in anesthesia and procedural sedation. Additionally, the growing adoption of capnography in outpatient surgeries and pre-hospital care contributes to the market's expansion in the U.S.

Key players in the Global Capnography Devices Market include companies such as ZOLL Medical, Medtronic, Philips Healthcare, Masimo Corporation, and Becton, Dickinson and Company. These companies are strengthening their market positions through strategic collaborations, product innovations, and offering more advanced, portable, and cost-effective solutions. By focusing on customer needs for improved patient safety and ease of use, these companies are increasing their market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing number of minimally invasive surgeries

- 3.2.1.2 Rising number of respiratory diseases

- 3.2.1.3 Surging preference for capnometers over oximetry

- 3.2.1.4 Recent technological advancements coupled with favorable government initiatives

- 3.2.1.5 Increasing number of plastic surgeries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals

- 3.2.2.2 High cost of the device

- 3.2.2.3 Stringent regulatory guidelines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hand-held

- 5.3 Stand-alone

- 5.4 Multi-parameter

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Side stream

- 6.3 Main stream

- 6.4 Micro stream

Chapter 7 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Original equipment manufacturer (OEM) modules

- 7.3 Other components

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Procedural sedation

- 8.3 Emergency medicine

- 8.4 Critical care

- 8.5 Pain management

- 8.6 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Becton, Dickinson and Company

- 11.2 Criticare Systems

- 11.3 Dragerwerk

- 11.4 Edan Instruments

- 11.5 Infinium Medical

- 11.6 Masimo Corporation

- 11.7 Medtronic

- 11.8 Mindray Medical

- 11.9 Nihon Kohden

- 11.10 Nonin Medical

- 11.11 Phillips Healthcare

- 11.12 Shenzhen Comen Medical Instruments

- 11.13 Smiths Medical

- 11.14 ZOLL Medical