低電圧サーキットブレーカーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Low Voltage Circuit Breaker Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750539

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

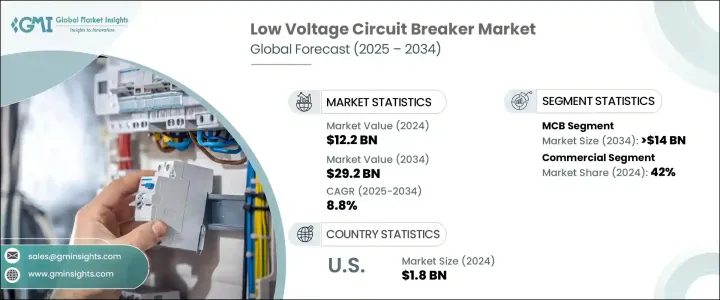

世界の低電圧サーキットブレーカー市場は、2024年には122億米ドルと評価され、CAGR 8.8%で成長し、2034年には292億米ドルに達すると予測されています。

これは、特に住宅および商業建設部門におけるインフラへの大規模な投資が、信頼性の高い回路保護システムへの需要を後押ししているためです。さらに、近代的な製造施設のデジタル化と相互接続が進むにつれて、インテリジェントな回路保護ソリューションの需要が高まっています。スマートモニタリング、リモート診断、リアルタイム故障検出を備えた低圧サーキットブレーカは、自動化環境において不可欠なコンポーネントとなっています。

これらの高度な機能は、ダウンタイムとメンテナンスコストを削減するだけでなく、予知保全戦略もサポートします。インダストリー4.0への移行は、特に自動車、エレクトロニクス、重機などの分野において、より堅牢で応答性の高い回路保護システムの必要性を強化しています。また、複合商業施設、データセンター、再生可能エネルギー設備などのインフラプロジェクトへの投資が増加しており、市場の成長をさらに促進しています。各国政府は、より厳しい規制を実施し、時代遅れの電気インフラをアップグレードするためのインセンティブを提供することで、極めて重要な役割を果たしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 122億米ドル |

| 予測金額 | 292億米ドル |

| CAGR | 8.8% |

小型サーキットブレーカー(MCB)分野は、過負荷や短絡時に回路を自動的に切断し、電気火災のリスクを軽減する機能によって、2034年までに140億米ドルに達すると予測されています。この機能は、世界の急速な都市化とインフラ開発に伴い、住宅、商業、工業の各分野で不可欠なものとなっています。世界の都市部の成長と電力需要の増加に伴い、MCBは電気設備における重要な部品となりつつあり、新築と改修スペースの両方で安全な配電を保証しています。

商業用最終用途セグメントは2024年に42%のシェアを占め、2034年までCAGR 8.5%で成長すると予想されています。家庭における電気安全性の革新とスマートホーム技術の進歩が、高度な回路保護システムの成長を促進しています。オフィスや小売業などの商業部門では、省エネ技術とともに自動化の導入が進んでおり、機器を保護し継続的な電力供給を保証する信頼性の高いサーキットブレーカの必要性が高まっています。産業活動の強化、新しい製造工場、再生可能エネルギー資源の追加は、産業市場に顕著な拡大をもたらしています。

米国の低電圧サーキットブレーカー市場の規模は、2024年には18億米ドルを生み出しました。人口増加と都市化に伴う住宅、商業、工業セクターの電力需要の増加は、信頼性が高く効率的な電気システムの必要性を強調し、低電圧サーキットブレーカの需要を促進しています。米国の老朽化した電気インフラを改善するための投資は、各地域がシステムの安全性と信頼性の向上に注力しているため、市場の拡大をさらに後押ししています。全体として、低電圧サーキットブレーカ市場は、インフラ開発、安全基準の強化、近代化と自動化への世界の動向によって、大きく成長する見込みです。

Texas Instruments社、L&T Electrical and Automation社、Efacec社、Tesco Automation社、Hitachi Energy社、Locamation社、Rockwell Automation社、Schneider Electric社、CG Power社、Siemens社、Eaton社、General Electric社、ABB社、Open System International社は、低電圧サーキットブレーカー市場の革新と成長を牽引する主要企業です。低電圧サーキットブレーカー市場の主要メーカーは、革新、拡大、デジタル統合戦略を組み合わせて購入し、市場での地位を強化しています。多くの企業が研究開発に多額の投資を行い、予知保全や遠隔監視をサポートする、よりスマートでエネルギー効率の高いサーキットブレーカーを開発しています。ハイテク企業との戦略的提携は、製品の自動化とIoT互換性の強化に役立っています。いくつかの企業は、新興市場に参入し、地域の需要に対応するために現地に製造施設やサービス施設を設立することで、世界の足跡を拡大しています。また、市場シェアを強化し、製品ポートフォリオを多様化するために、M&Aに注力している企業もあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 競合情勢

- 戦略的ダッシュボード

- 企業の市場シェア分析

- 競合ベンチマーキング

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:製品別、2021-2034

- 主要動向

- ACB

- MCB

- MCCB

- その他

第6章 市場規模・予測:最終用途別、2021-2034

- 主要動向

- 住宅用

- 商業用

- 産業

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- イタリア

- 英国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- オマーン

- 南アフリカ

- ラテンアメリカ

- ブラジル

- チリ

第8章 企業プロファイル

- ABB

- CG Power

- Eaton

- Efacec

- General Electric

- Hitachi Energy

- L&T Electrical and Automation

- Locamation

- Open System International

- Rockwell Automation

- Schneider Electric

- Siemens

- Tesco Automation

- Texas Instruments

目次

The Global Low Voltage Circuit Breaker Market was valued at USD 12.2 billion in 2024 and is estimated to grow at 8.8% CAGR to reach USD 29.2 billion by 2034, driven by substantial investments in infrastructure, especially within the residential and commercial construction sectors, boosting demand for reliable circuit protection systems. Moreover, as modern manufacturing facilities become more digitized and interconnected, the demand for intelligent circuit protection solutions is gaining traction. Low-voltage circuit breakers equipped with smart monitoring, remote diagnostics, and real-time fault detection are becoming essential components in automated environments.

These advanced features not only reduce downtime and maintenance costs but also support predictive maintenance strategies, which are crucial for minimizing operational disruptions. The transition to Industry 4.0 reinforces the need for more robust and responsive circuit protection systems, particularly in sectors such as automotive, electronics, and heavy machinery. In tandem, rising investments in infrastructure projects-including commercial complexes, data centers, and renewable energy installations-are further stimulating market growth. Governments play a pivotal role by implementing stricter regulations and offering incentives for upgrading outdated electrical infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.2 Billion |

| Forecast Value | $29.2 Billion |

| CAGR | 8.8% |

The miniature circuit breaker (MCB) segment is projected to reach USD 14 billion by 2034, fueled by its ability to automatically disconnect circuits during overloads or short circuits, thereby mitigating the risks of electrical fires. This feature has become essential across residential, commercial, and industrial settings, aligning with rapid urbanization and infrastructure development worldwide. As global urban areas grow and electricity demand rises, MCBs are becoming critical components in electrical installations, ensuring safe power distribution in both new constructions and renovated spaces.

The commercial end-use segment held a 42% share in 2024 and is anticipated to grow at a CAGR of 8.5% through 2034. Innovations in electrical safety at home and the advancement in smart home technologies drive the growth of highly advanced circuit protection systems. Commercial sectors, including offices and retail, are adopting automation alongside energy-saving technologies, which increases the need for reliable circuit breakers to protect equipment and ensure a continuous power supply. The enhancement of industrial activities, new manufacturing plants, and the addition of renewable energy resources are creating notable expansion in the industrial market.

U.S. Low Voltage Circuit Breaker Market generated USD 1.8 billion in 2024. Rising electricity demand across residential, commercial, and industrial sectors, alongside population growth and urbanization, underscores the need for reliable and efficient electrical systems, thereby driving demand for low-voltage circuit breakers. Investments in upgrading the U.S. aging electrical infrastructure further support market expansion as regions focus on improving system safety and reliability. Overall, the low-voltage circuit breaker market is set for significant growth, driven by infrastructure development, heightened safety standards, and the global trend toward modernization and automation.

Texas Instruments, L&T Electrical and Automation, Efacec, Tesco Automation, Hitachi Energy, Locamation, Rockwell Automation, Schneider Electric, CG Power, Siemens, Eaton, General Electric, ABB, and Open System International are key players driving innovation and growth in the low voltage circuit breaker market. Leading manufacturers in the low voltage circuit breaker market purchase a blend of innovation, expansion, and digital integration strategies to strengthen their market position. Many companies invest heavily in R&D to develop smarter, more energy-efficient circuit breakers that support predictive maintenance and remote monitoring. Strategic collaborations with tech firms are helping enhance product automation and IoT compatibility. Several players are expanding their global footprint by entering emerging markets and establishing local manufacturing or service facilities to meet regional demand. Others focus on mergers and acquisitions to consolidate their market share and diversify their product portfolios.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Competitive landscape, 2025

- 4.2 Strategic dashboard

- 4.3 Company market share analysis

- 4.4 Competitive benchmarking

- 4.5 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (‘000 Units, USD Million)

- 5.1 Key trends

- 5.2 ACB

- 5.3 MCB

- 5.4 MCCB

- 5.5 Others

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 (‘000 Units, USD Million)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (‘000 Units, USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Italy

- 7.3.4 UK

- 7.3.5 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Oman

- 7.5.5 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Chile

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 CG Power

- 8.3 Eaton

- 8.4 Efacec

- 8.5 General Electric

- 8.6 Hitachi Energy

- 8.7 L&T Electrical and Automation

- 8.8 Locamation

- 8.9 Open System International

- 8.10 Rockwell Automation

- 8.11 Schneider Electric

- 8.12 Siemens

- 8.13 Tesco Automation

- 8.14 Texas Instruments

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日