|

市場調査レポート

商品コード

1750524

高温産業用ボイラーの市場機会、成長促進要因、産業動向分析、2025~2034年予測High Temperature Industrial Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 高温産業用ボイラーの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月09日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

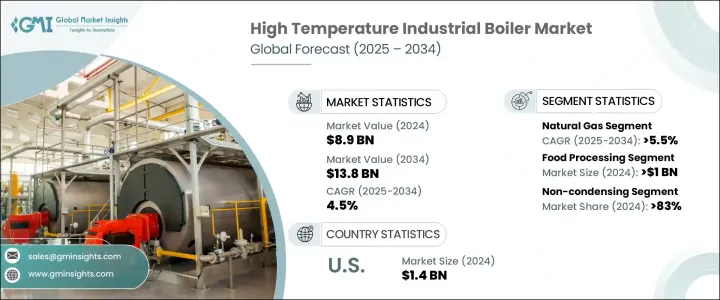

高温産業用ボイラーの世界市場規模は2024年に89億米ドルとなり、発展途上国における急速な都市拡大による産業生産の急増を背景に、CAGR 4.5%で成長し、2034年には138億米ドルに達すると予測されています。

各国がエネルギー効率を高めるためにより厳しい規制を実施する中、高度なボイラー技術に対する需要は大幅に伸びると予想されます。人口水準の上昇は、特に商業・工業スペースの暖房ソリューションの消費パターンに影響を与えます。インフラ開発が勢いを増し、再生可能エネルギーの統合が普及するにつれて、産業界はより環境に優しい低排出技術の採用を迫られるようになっています。こうした動向は、持続可能な高温ボイラーシステムの需要を促進すると予想されます。

この業界は、近代的な製造プロセスへの投資の拡大や、世界レベルでの環境意識の高い政策によっても形成されています。排ガス規制が優先課題となる中、気候変動目標に沿ったエネルギー効率の高いソリューションが好まれるようになっています。高温産業用ボイラー市場は、運用コストとエネルギー消費量の削減を目指す部門全体で統合システムの利用が増加していることから、さらなる恩恵を受けています。エネルギー安全保障と天然ガスインフラの利用可能性の拡大が、ガス式高温ボイラーの採用を引き続き後押ししています。信頼性の高い高温スチーム・ソリューションが、特に熱を大量に消費する環境において産業界から求められており、事業の見通しは引き続き堅調です。貿易政策と競合要因は、国際競争力を形成する追加要因です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 89億米ドル |

| 予測金額 | 138億米ドル |

| CAGR | 4.5% |

天然ガス焚き高温ボイラーは、産業界がよりクリーンなエネルギー源への移行を続けているため、2034年までCAGR 5.5%で成長すると予測されます。大気質に関する懸念の高まり、天然ガスの利用可能性の上昇、支援インフラの拡大により、これらのシステムはより実行可能で費用対効果が高いものとなっています。多くの政府や民間団体が、温室効果ガスを多く排出する石炭・石油への依存を減らすため、ガス暖房技術に積極的に投資しています。天然ガス・ボイラーは、低排出ガスレベルを維持しながら安定した高温出力を提供できるため、製造、加工、化学などのエネルギー集約型セクターで好ましい選択肢となっています。

非凝縮式高温ボイラー・セグメントは2024年に83%のシェアを占めました。これらのボイラーは、シンプルな設計、耐久性、過酷な環境でも性能を発揮する能力で支持されています。連続的な加熱が必要な産業では、その高い保温性と迅速な応答時間により、非凝縮システムに大きく依存しています。環境規制の高まりにもかかわらず、インフラやコストへの配慮から凝縮型やハイブリッド型に移行できない場合、これらのボイラーは依然として人気があります。しかし、効率基準の変化に対応するため、メーカー各社は、より優れた制御システムと高度な燃焼技術によって、非凝縮型モデルを強化しています。

米国の高温産業用ボイラー市場は、国内需要の堅調さを反映して、2024年には14億米ドルに達しました。この成長の大部分は、古い産業施設の老朽化した非効率的なボイラーシステムの置き換えによるものです。エネルギー消費と排出に関する新たな規制が厳しくなるにつれて、産業界は操業を近代化しています。連邦および州レベルのインセンティブは、よりクリーンで高効率の機器の採用を支援することで、このシフトを促しています。持続可能性への注目の高まりは、エネルギー・インフラへの経済的投資と相まって、将来対応可能なエネルギー政策に沿った技術的に高度なボイラーへのニーズを後押ししています。

市場情勢に貢献している主要企業には、Siemens、Thermax、Mitsubishi Heavy Industries、Hurst Boiler and Welding、Babcock and Wilcox Enterprises、Sofinter、Forbes Marshall、GE Vernova、Victory Energy Operations、Cleaver-Brooks、Viessmann、Clayton Industries、Cochran、Doosan Heavy Industries & Construction および、 FONDITAL、Bharat Heavy Electricals、FERROLI、Hoval、John Wood Group、Groupe Atlantic、IHI Corporation、Walchandnagar Industries、John Cockerill、Miura America、The Fulton Companies、Robert Bosch、Fonderie Sime、Rentech Boilers などがあります。同市場での地位を強化するため、大手企業は技術革新、持続可能性、戦略的提携に注力しています。各社は研究開発に投資し、厳しい排出基準を満たすコンパクトでエネルギー効率の高いボイラーを開発しています。政府や他の産業企業との提携は、業務範囲を拡大し、サプライ・チェーンを合理化するのに役立っています。多くの企業は、ボイラーの性能を最適化し、ダウンタイムを最小化するためにデジタル制御システムを強化する一方、長期的な顧客関係を構築するためにアフターマーケット・サービスを拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 自動ベンチトップ歯科用オートクレーブの需要増加

- 感染制御への注目が高まる

- オートクレーブの技術的進歩

- 歯科疾患の罹患率の上昇

- 業界の潜在的リスク&課題

- 再生歯科用オートクレーブの導入

- 新興経済諸国における認識の低さ

- 促進要因

- 成長可能性分析

- 技術的情勢

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 国別の対応

- 業界への影響

- 供給側の影響(製造コスト)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(消費者のコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(製造コスト)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 自動

- 半自動

- マニュアル

第6章 市場推計・予測:技術別、2021-2034

- 主要動向

- 真空前後

- 重力

第7章 市場推計・予測:クラス別、2021-2034

- 主要動向

- クラスB

- Nクラス

- Sクラス

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院と歯科医院

- 歯科技工所

- 学術研究機関

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Biolab Scientific

- Bionics Scientific

- Dentsply Sirona

- Flight Dental Systems

- FONA

- Labocon

- Life Steriware

- Matachana

- Midmark Corporation

- NSK

- RAYPA

- Steelco

- Thermo Fisher Scientific

- Tuttnauer

- W&H

The Global High Temperature Industrial Boiler Market was valued at USD 8.9 billion in 2024 and is estimated to grow at a CAGR of 4.5% to reach USD 13.8 billion by 2034, driven by the surge in industrial production with rapid urban expansion across developing nations. As countries implement stricter regulations to boost energy efficiency, demand for advanced boiler technologies is expected to grow significantly. Rising population levels influence consumption patterns, particularly for heating solutions in commercial and industrial spaces. With infrastructure development gaining momentum and renewable energy integration becoming more widespread, industries are under increased pressure to adopt greener, low-emission technologies. These trends are expected to fuel demand for sustainable high-temperature boiler systems.

The industry is also being shaped by growing investments in modern manufacturing processes and eco-conscious policies at the global level. With emissions control becoming a priority, there's a growing preference for energy-efficient solutions that align with climate goals. The high temperature industrial boiler market is further benefiting from the increased use of integrated systems across sectors seeking to reduce operational costs and energy consumption. Energy security and the expanding availability of natural gas infrastructure continue to support the adoption of gas-powered high-temperature boilers. With industries demanding reliable high-temperature steam solutions, especially in heat-intensive environments, the business outlook remains strong. Trade policies and component pricing are additional factors shaping global competitiveness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.9 Billion |

| Forecast Value | $13.8 Billion |

| CAGR | 4.5% |

Natural gas-fired high temperature boilers are projected to grow at a CAGR of 5.5% through 2034, as industries continue shifting toward cleaner energy sources. Increasing concerns around air quality, rising natural gas availability, and expanding supportive infrastructure make these systems more viable and cost-effective. Many governments and private entities are actively investing in gas-powered heating technologies to reduce dependence on coal and oil, which emit higher levels of greenhouse gases. The ability of natural gas boilers to deliver consistent high-temperature output while maintaining lower emission levels positions them as a preferred option across energy-intensive sectors such as manufacturing, processing, and chemicals.

Non-condensing high temperature boilers segment held an 83% share in 2024. These boilers are favored for their simple design, durability, and ability to perform in demanding environments. Industries with continuous heating needs rely heavily on non-condensing systems due to their high heat retention and quick response time. Despite growing environmental regulations, these boilers remain popular where infrastructure or cost considerations prevent a shift to condensing or hybrid models. However, to meet changing efficiency standards, manufacturers are enhancing non-condensing models with better control systems and advanced combustion technologies.

United States High Temperature Industrial Boiler Market reached USD 1.4 billion in 2024, reflecting strong domestic demand. A major portion of this growth is attributed to replacing aging and inefficient boiler systems in older industrial facilities. As new regulations on energy consumption and emissions become more stringent, industries modernize their operations. Federal and state-level incentives are encouraging this shift by offering support for the adoption of cleaner, high-efficiency equipment. The increased focus on sustainability, coupled with economic investments in energy infrastructure, is driving the need for technologically advanced boilers that align with future-ready energy policies.

Leading companies contributing to the market landscape include Siemens, Thermax, Mitsubishi Heavy Industries, Hurst Boiler and Welding, Babcock and Wilcox Enterprises, Sofinter, Forbes Marshall, GE Vernova, Victory Energy Operations, Cleaver-Brooks, Viessmann, Clayton Industries, Cochran, Doosan Heavy Industries & Construction, FONDITAL, Bharat Heavy Electricals, FERROLI, Hoval, John Wood Group, Groupe Atlantic, IHI Corporation, Walchandnagar Industries, John Cockerill, Miura America, The Fulton Companies, Robert Bosch, Fonderie Sime, and Rentech Boilers. To reinforce their position in the market, major players are focusing on innovation, sustainability, and strategic alliances. Companies invest in R&D to develop compact, energy-efficient boilers that meet stringent emissions standards. Partnerships with governments and other industrial firms help expand operational reach and streamline supply chains. Many enhance digital control systems to optimize boiler performance and minimize downtime, while expanding aftermarket services to build long-term client relationships.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for automatic bench-top dental autoclaves

- 3.2.1.2 Growing focus on infection control

- 3.2.1.3 Technological advancement in autoclave

- 3.2.1.4 Rising prevalence of dental disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adoption of refurbished dental autoclaves

- 3.2.2.2 Limited awareness in developing economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technological landscape

- 3.5 Regulatory landscape

- 3.6 Trump administration tariffs

- 3.6.1 Impact on trade

- 3.6.1.1 Trade volume disruptions

- 3.6.1.2 Country-wise response

- 3.6.2 Impact on the industry

- 3.6.2.1 Supply-side impact (Cost of manufacturing)

- 3.6.2.1.1 Price volatility in key materials

- 3.6.2.1.2 Supply chain restructuring

- 3.6.2.1.3 Production cost implications

- 3.6.2.2 Demand-side impact (Cost to consumers)

- 3.6.2.2.1 Price transmission to end markets

- 3.6.2.2.2 Market share dynamics

- 3.6.2.2.3 Consumer response patterns

- 3.6.2.1 Supply-side impact (Cost of manufacturing)

- 3.6.3 Key companies impacted

- 3.6.4 Strategic industry responses

- 3.6.4.1 Supply chain reconfiguration

- 3.6.4.2 Pricing and product strategies

- 3.6.4.3 Policy engagement

- 3.6.5 Outlook and future considerations

- 3.6.1 Impact on trade

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Automatic

- 5.3 Semi-automatic

- 5.4 Manual

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pre and post vacuum

- 6.3 Gravity

Chapter 7 Market Estimates and Forecast, By Class, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Class B

- 7.3 Class N

- 7.4 Class S

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and dental clinics

- 8.3 Dental laboratories

- 8.4 Academic and research institutes

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Biolab Scientific

- 10.2 Bionics Scientific

- 10.3 Dentsply Sirona

- 10.4 Flight Dental Systems

- 10.5 FONA

- 10.6 Labocon

- 10.7 Life Steriware

- 10.8 Matachana

- 10.9 Midmark Corporation

- 10.10 NSK

- 10.11 RAYPA

- 10.12 Steelco

- 10.13 Thermo Fisher Scientific

- 10.14 Tuttnauer

- 10.15 W&H