|

市場調査レポート

商品コード

1750519

非包装発泡体の市場機会、成長促進要因、産業動向分析、2025~2034年予測Nonpackaging Foam Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 非包装発泡体の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月06日

発行: Global Market Insights Inc.

ページ情報: 英文 360 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

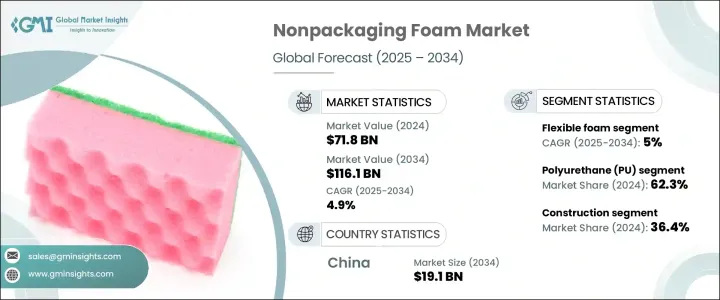

非包装発泡体の世界市場規模は、2024年に718億米ドルとなり、建設、自動車、家具、エレクトロニクス、ヘルスケアなどの分野における軽量で耐久性のある断熱材への需要増加を背景に、CAGR 4.9%で成長し、2034年には1,161億米ドルに達すると予測されています。

産業が拡大を続ける中、非包装発泡体は、その汎用性、性能、様々な用途の特定のニーズを満たす能力により、不可欠なものとなっています。北米、欧州、アジア太平洋の新興市場では、環境問題に対応し、厳しい規制を満たすために、バイオベース、リサイクル可能、生分解性など、持続可能な発泡体ソリューションの開拓にますます力を入れています。

持続可能性への取り組みは、非包装発泡体市場の形成に重要な役割を果たしています。企業は、石油化学原料への依存を減らし、循環型経済への取り組みを支援するクローズド・ループ・リサイクル・システムに投資しています。この動向は、政府が環境政策を強化し、環境に優しい製品の開発を奨励している北米と欧州で特に顕著です。アジア太平洋では、特に中国など、建設業や自動車産業が主要な促進要因となっている国々で、インフラや製造業が拡大し、非包装発泡体の需要が急速に伸びています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 718億米ドル |

| 予測金額 | 1,161億米ドル |

| CAGR | 4.9% |

市場は製品タイプ別に区分され、軟質フォームと硬質フォームが主なカテゴリーです。軟質フォームは、家具、寝具、自動車内装、防音材など幅広い用途があるため、2024年には477億米ドルを生み出し、2034年にはCAGR 5%で成長して778億米ドルに達すると予測されます。人間工学に基づいたマットレスや軽量の自動車部品など、快適性を重視した製品に対する需要の高まりが、軟質フォームの拡大を後押ししています。さらに、持続可能な低VOC処方へのシフトの増加やeコマースの台頭が、軟質フォームの需要をさらに押し上げています。

非包装発泡体市場のポリウレタン(PU)フォーム分野は2024年に62.3%のシェアを占めたが、これは断熱材、自動車内装材、家具用クッション材などの用途における卓越した汎用性に起因します。PUフォームは軽量で耐熱性に優れているため、エネルギー効率と快適性を重視する産業にとって理想的な素材です。PUフォームは、さまざまな分野のニーズに合わせて簡単にカスタマイズできるため、その需要はさらに高まっています。幅広い密度と形状に成形できるため、硬質と軟質の両方の用途に使用でき、さまざまな市場でその有用性が拡大しています。

中国の非包装発泡体の市場規模は、2024年には117億米ドルと評価されました。建設と自動車セクターの需要急増に牽引され、CAGR 5.1%で成長し、2034年には191億米ドルに達すると予想されます。インフラ整備への政府投資の増加が、断熱材、防音材、構造用発泡体などの材料へのニーズを煽っています。さらに、電気自動車(EV)の台頭により、特に軽量でエネルギー効率の高い材料への需要が高まっている自動車産業において、フォームの新たな利用機会がもたらされています。これらの分野が拡大を続ける中、非包装発泡体、特にPUフォームの市場は中国で持続的な成長を遂げようとしています。

非包装発泡体の世界市場における主要企業は、Huntsman Corporation、BASF、INOAC Corporation、Covestroなどです。これらの企業は、生産能力の拡大、製品提供の強化、持続可能性への取り組みの推進に注力しています。発泡体製造の技術的進歩を活用し、環境に優しいソリューションに注力することで、これらの企業は競争市場での地位を強化することを目指しています。さらに、非包装発泡体の世界の需要拡大に対応するため、戦略的提携、買収、地域拡大への投資も行っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税の影響- 構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計

- 主要輸入国

- 国1

- 国2

- 国3

- 主要輸出国

- 国1

- 国2

- 国3

- 主要輸入国

- 利益率分析

- 規制情勢

- 影響要因

- 促進要因

- エネルギー効率の高い建築資材の需要増加

- 自動車および家具分野における軽量性と快適性の要件

- 新興市場における急速な工業化とインフラ開発

- 業界の潜在的リスク&課題

- 発泡スチロール廃棄物とVOC排出に関する環境懸念と規制

- 原材料価格の変動

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

- バリューチェーン分析

- 原材料サプライヤー

- フォームメーカー

- 加工業者およびコンバーター

- 販売業者と小売業者

- 最終用途産業

- バリューチェーン最適化戦略

- コスト構造分析

- 価格分析

- 環境規制とコンプライアンス要件

- 製品規格と認証

- 輸出入規制

- 規制による市場成長への影響

- 将来の規制動向

- 持続可能性と環境への影響

- 素材の種類別の価格評価

- 非包装発泡体の環境フットプリント

- 持続可能なフォームソリューション

- バイオベースのフォーム

- リサイクル可能なフォーム

- 生分解性フォーム

- リサイクルと廃棄物管理

- 循環型経済の取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 柔軟なフォーム

- 硬質フォーム

第6章 市場推計・予測:材料別、2021-2034

- 主要動向

- ポリウレタン(PU)

- ポリスチレン(PS)

- ポリエチレン(PE)

- ポリプロピレン(PP)

- ゴムフォーム

- その他

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 建設

- 自動車

- 家具と寝具

- エレクトロニクス

- ヘルスケア

- その他

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- BASF

- Armacell International

- Covestro

- Dow

- FXI Holdings

- Huntsman Corporation

- INOAC Corporation

- JSP Corporation

- Recticel

- Saint-Gobain

- Sheela Foam

- UFP Technologies

- Wanhua Chemical Group

- Woodbridge Group

- Zotefoams

The Global Nonpackaging Foam Market was valued at USD 71.8 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 116.1 billion by 2034, driven by the increasing demand for lightweight, durable insulating materials in sectors such as construction, automotive, furniture, electronics, and healthcare. As industries continue to expand, nonpackaging foam has become essential due to its versatility, performance, and ability to meet the specific needs of various applications. Manufacturers are increasingly focusing on developing sustainable foam solutions, such as bio-based, recyclable, and biodegradable options, to address environmental concerns and meet stringent regulations in North America, Europe, and emerging markets in Asia-Pacific.

Sustainability efforts are playing a significant role in shaping the nonpackaging foam market. Companies are investing in closed-loop recycling systems, which reduce the reliance on petrochemical feedstocks and support circular economy initiatives. This trend is particularly prominent in North America and Europe, where governments are tightening environmental policies and encouraging the development of eco-friendly products. In Asia-Pacific, the demand for nonpackaging foam is growing rapidly, driven by the expansion of infrastructure and manufacturing sectors, especially in countries such as China, where construction and automotive industries are key growth drivers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $71.8 Billion |

| Forecast Value | $116.1 Billion |

| CAGR | 4.9% |

The market is segmented by product type, with flexible and rigid foam being the two main categories. Flexible foam generated USD 47.7 billion in 2024 and is projected to reach USD 77.8 billion by 2034, growing at a 5% CAGR due to its broad range of applications, including furniture, bedding, automotive interiors, and acoustic insulation. The growing demand for comfort-focused products, such as ergonomic mattresses and lightweight vehicle components, is driving the expansion of flexible foam. Additionally, the increasing shift toward sustainable, low-VOC formulations and the rise of e-commerce have further boosted the demand for flexible foam.

Polyurethane (PU) foam segment in the nonpackaging foam market held 62.3% share in 2024, attributed to its exceptional versatility in applications such as thermal insulation, automotive interiors, and cushioning for furniture. The material's lightweight nature and excellent thermal resistance make it an ideal choice for industries that prioritize energy efficiency and comfort. PU foam is easily customizable to meet the specific needs of different sectors, which further drives its demand. Its capacity to be molded into a wide range of densities and forms enables it to serve both rigid and flexible purposes, expanding its utility across various markets.

China Nonpackaging Foam Market generated USD 11.7 billion in 2024 and is expected to grow at a CAGR of 5.1%, reaching USD 19.1 billion by 2034, driven by the surging demand in the construction and automotive sectors. Increased government investment in infrastructure development is fueling the need for materials like insulation, soundproofing, and structural foam. Additionally, the rise of electric vehicles (EVs) has introduced new opportunities for foam usage, particularly in the automotive industry, where demand for lightweight, energy-efficient materials is on the rise. As these sectors continue to expand, the market for nonpackaging foam, especially PU foam, is poised for sustained growth in China.

Leading players in the Global Nonpackaging Foam Market include Huntsman Corporation, BASF, INOAC Corporation, and Covestro. These companies are focusing on expanding their production capacities, enhancing product offerings, and advancing sustainability initiatives. By leveraging technological advancements in foam production and focusing on eco-friendly solutions, these players aim to strengthen their position in the competitive market. Moreover, they are investing in strategic partnerships, acquisitions, and regional expansions to meet the growing demand for nonpackaging foam globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade Statistics

- 3.3.1 Major importing countries

- 3.3.1.1 Country 1

- 3.3.1.2 Country 2

- 3.3.1.3 Country 3

- 3.3.2 Major exporting countries

- 3.3.2.1 Country 1

- 3.3.2.2 Country 2

- 3.3.2.3 Country 3

- 3.3.1 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for energy-efficient building materials

- 3.6.1.2 Lightweight and comfort requirements in automotive and furniture sectors

- 3.6.1.3 Rapid industrialization and infrastructure development in emerging markets

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Environmental concerns and regulations on foam waste and VOC emissions

- 3.6.2.2 Volatility in raw material prices

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Value chain analysis

- 3.10.1 Raw material suppliers

- 3.10.2 Foam manufacturers

- 3.10.3 Fabricators and converters

- 3.10.4 Distributors and retailers

- 3.10.5 End-use industries

- 3.10.6 Value chain optimization strategies

- 3.10.7 Cost structure analysis

- 3.11 Pricing Analysis

- 3.11.1 North America

- 3.11.2 Europe

- 3.11.3 Asia Pacific

- 3.11.4 Latin America

- 3.11.5 Middle East and Africa

- 3.12 Environmental regulations and compliance requirements

- 3.12.1 Product standards and certifications

- 3.12.2 Import/export regulations

- 3.12.3 Regulatory impact on market growth

- 3.12.4 Future regulatory trends

- 3.13 Sustainability and environmental impact

- 3.13.1 Price point assessment by material type

- 3.13.2 Environmental footprint of nonpackaging foam

- 3.13.3 Sustainable foam solutions

- 3.13.4 Bio-based foams

- 3.13.5 Recyclable foams

- 3.13.6 Biodegradable foams

- 3.13.7 Recycling and waste management

- 3.13.8 Circular economy initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Flexible foam

- 5.3 Rigid foam

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Polyurethane (PU)

- 6.3 Polystyrene (PS)

- 6.4 Polyethylene (PE)

- 6.5 Polypropylene (PP)

- 6.6 Rubber foam

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Automotive

- 7.4 Furniture & bedding

- 7.5 Electronics

- 7.6 Healthcare

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF

- 9.2 Armacell International

- 9.3 Covestro

- 9.4 Dow

- 9.5 FXI Holdings

- 9.6 Huntsman Corporation

- 9.7 INOAC Corporation

- 9.8 JSP Corporation

- 9.9 Recticel

- 9.10 Saint-Gobain

- 9.11 Sheela Foam

- 9.12 UFP Technologies

- 9.13 Wanhua Chemical Group

- 9.14 Woodbridge Group

- 9.15 Zotefoams