|

市場調査レポート

商品コード

1750514

業務用ガス焚きボイラーの市場機会、成長促進要因、産業動向分析、2025~2034年予測Commercial Gas Fired Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 業務用ガス焚きボイラーの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月15日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

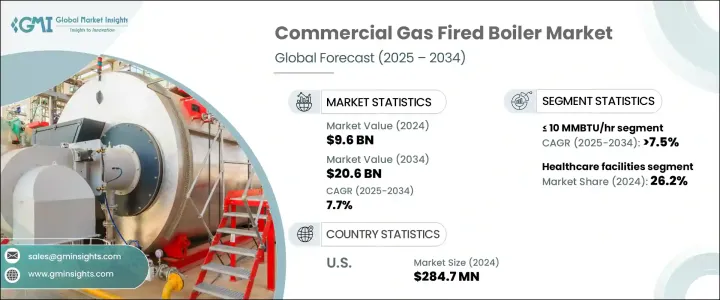

業務用ガス焚きボイラーの世界市場規模は2024年に96億米ドルとなり、2034年にはCAGR 7.7%で成長して206億米ドルに達すると推定されます。

ボイラー・システムにおけるモノのインターネット(IoT)の利用拡大により、遠隔監視、リアルタイムの性能最適化、予知保全が可能になり、ダウンタイムの削減と運用コストの削減が実現します。このセクターは、水素混合技術革新の恩恵を受けており、大手メーカーはダイナミックな暖房需要に対応する先進モデルを設計しています。こうした取り組みは、性能の信頼性を維持しながら、よりクリーンなエネルギー転換をサポートすることを目的としています。

モジュール式暖房システムに対する需要の高まりは、大規模なキャンパス、企業オフィス、商業施設のエネルギー使用への取り組み方を変革しています。バイオテクノロジー、製薬、データインフラといった分野の継続的な拡大により、信頼性と適応性を提供する精密な暖房ソリューションが求められています。サプライチェーンの不確実性や貿易規制の変化に対応するため、ボイラーメーカーは国内生産に投資して供給対応力を高め、地政学的リスクを軽減しています。例えば、金属に対する関税が以前に実施され、製造業の経済性に大きな影響を与えたため、企業は事業を現地化し、部品調達戦略を多様化する動機付けとなりました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 96億米ドル |

| 予測金額 | 206億米ドル |

| CAGR | 7.7% |

10 MMBTU/hr未満のシステムは力強い成長軌道を維持し、2034年までCAGR 7.5%で拡大すると予想されます。こうした小型で高効率のソリューションは、教育機関、小売店、ヘルスケア施設、ホスピタリティ・ビルなど、スペースに制約のある環境に適しています。拡張性があり、初期投資とメンテナンスのコストが低いため、性能や排出基準を損なうことなく安定した暖房を提供できる、費用対効果の高い方法です。

商業オフィス部門は、現代の持続可能性ベンチマークに沿ったインテリジェントでエネルギー効率の高い暖房システムへの需要増に後押しされ、2034年までに35億米ドルに達すると予測されています。企業は、コンプライアンス要件を満たすためだけでなく、業務効率を高めるためにも、コンデンシングボイラーや超低NOx技術を採用しています。ビルオートメーションシステムとの統合が一般的になりつつあり、施設管理者は暖房負荷を制御してエネルギーの無駄を省くことができます。

米国の業務用ガス焚きボイラー市場規模は、2024年には2億8,470万米ドルと評価され、全国的なインフラ近代化努力と温室効果ガス排出削減を義務付ける環境規制の強化が原動力となっています。商業ビル、特に暖房のアップグレードが必要な老朽化した建築物では、より高い熱効率とデジタル統合をサポートする高度なボイラーシステムへの切り替えが進んでいます。クリーンエネルギーの導入を奨励する政府の優遇措置や地域の規制も、従来型システムから高性能のガス焚き代替システムへの置き換えを促進する一因となっています。

BDR Thermea Group、Lochinvar、Viessmann、Ariston Holding、Bosch Industriekessel、Weil-McLain、Bradford White Corporation、A.O. Smith、Burnham Commercial、Daikin、Vaillant Group、FERROLI、FONDITAL、Immergas、Remeha、Hoval、Cleaver-Brooks、Babcock &Wilcoxなどの大手メーカーは、競争力を維持するために重要な戦略を採用しています。これらの戦略には、スマート製品ラインの拡大、水素対応モデルの研究開発強化、顧客サポートシステムの改善、地域製造ハブの構築などが含まれ、持続可能性目標を達成しながら、納品スピードの向上とコスト削減を図っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業の市場シェア分析

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:容量別、2021-2034

- 主要動向

- 10 MMBTU/時未満

- 10~50 MMBTU/時以上

- 50~100 MMBTU/時以上

- 100~250 MMBTU/時以上

- 250 MMBTU/時以上

第6章 市場規模・予測:技術別、2021-2034

- 主要動向

- 凝縮

- 不凝縮

第7章 市場規模・予測:用途別、2021-2034

- 主要動向

- オフィス

- ヘルスケア施設

- 教育機関

- 宿泊施設

- 小売店

- その他

第8章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- 英国

- ポーランド

- イタリア

- スペイン

- オーストリア

- ドイツ

- スウェーデン

- ロシア

- アジア太平洋地域

- 中国

- インド

- フィリピン

- 日本

- 韓国

- オーストラリア

- インドネシア

- 中東・アフリカ

- サウジアラビア

- イラン

- アラブ首長国連邦

- ナイジェリア

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第9章 企業プロファイル

- A.O. Smith

- Ariston Holding

- Babcock &Wilcox Enterprises

- BDR Thermea Group

- Bosch Industriekessel

- Bradford White Corporation

- BURNHAM COMMERCIAL BOILERS

- Cleaver-Brooks

- Daikin

- FERROLI

- FONDITAL

- Hoval

- Immergas

- Lochinvar

- Remeha

- Vaillant Group

- VIESSMANN

- Weil-McLain

The Global Commercial Gas Fired Boiler Market was valued at USD 9.6 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 20.6 billion by 2034, driven by evolving heating needs across sectors and the continued push for smarter, more efficient building systems. The increasing use of Internet of Things (IoT) in boiler systems enables remote monitoring, real-time performance optimization, and predictive maintenance, reducing downtime and cutting operational costs. The sector benefits from hydrogen blending innovations, with leading manufacturers designing advanced models to accommodate dynamic heating demands. These efforts aim to support cleaner energy transitions while maintaining performance reliability.

A rise in demand for modular heating systems is transforming how large campuses, corporate offices, and commercial facilities approach energy use. The continued expansion of sectors like biotechnology, pharmaceuticals, and data infrastructure has pushed for precision heating solutions that offer reliability and adaptability. In response to supply chain uncertainties and shifting trade regulations, boiler manufacturers invest in domestic production to enhance supply responsiveness and reduce geopolitical risks. For instance, earlier tariff implementations on metals significantly impacted manufacturing economics, motivating companies to localize operations and diversify component sourcing strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.6 Billion |

| Forecast Value | $20.6 Billion |

| CAGR | 7.7% |

Systems rated at <= 10 MMBTU/hr are expected to maintain a strong growth trajectory, expanding at a CAGR of 7.5% through 2034. These compact, high-efficiency solutions are well-suited for space-constrained environments such as educational institutions, retail outlets, healthcare facilities, and hospitality buildings. Their scalability and lower upfront and maintenance costs offer a cost-effective way to deliver consistent heating without compromising performance or emissions standards.

The commercial office segment is projected to reach USD 3.5 billion by 2034, fueled by increased demand for intelligent, energy-efficient heating systems in line with modern sustainability benchmarks. Organizations are adopting condensing boilers and ultra-low NOx technology not only to meet compliance requirements but also to enhance operational efficiency. Integration with building automation systems is becoming more common, allowing facility managers to control heating loads and reduce energy waste.

United States Commercial Gas Fired Boiler Market generated USD 284.7 million in 2024, driven by the nationwide infrastructure modernization efforts and stricter environmental mandates reducing greenhouse gas emissions. Commercial buildings-especially aging structures in need of heating upgrades-are switching to advanced boiler systems that support higher thermal efficiency and digital integration. Government incentives and regional regulations encouraging clean energy adoption have also contributed to the increased replacement of conventional systems with high-performance gas-fired alternatives.

Leading manufacturers such as BDR Thermea Group, Lochinvar, Viessmann, Ariston Holding, Bosch Industriekessel, Weil-McLain, Bradford White Corporation, A.O. Smith, Burnham Commercial, Daikin, Vaillant Group, FERROLI, FONDITAL, Immergas, Remeha, Hoval, Cleaver-Brooks, and Babcock & Wilcox are adopting key strategies to stay competitive. These include expanding smart product lines, boosting R&D in hydrogen-ready models, improving customer support systems, and building regional manufacturing hubs to increase delivery speed and reduce costs while meeting sustainability targets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiatives

- 4.4 Company market share analysis, 2024

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 10 MMBTU/hr

- 5.3 > 10 - 50 MMBTU/hr

- 5.4 > 50 - 100 MMBTU/hr

- 5.5 > 100 - 250 MMBTU/hr

- 5.6 > 250 MMBTU/hr

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Condensing

- 6.3 Non-condensing

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Offices

- 7.3 Healthcare facilities

- 7.4 Educational institutions

- 7.5 Lodgings

- 7.6 Retail stores

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 France

- 8.3.2 UK

- 8.3.3 Poland

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Germany

- 8.3.8 Sweden

- 8.3.9 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Philippines

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Australia

- 8.4.7 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 Iran

- 8.5.3 UAE

- 8.5.4 Nigeria

- 8.5.5 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

Chapter 9 Company Profiles

- 9.1 A.O. Smith

- 9.2 Ariston Holding

- 9.3 Babcock & Wilcox Enterprises

- 9.4 BDR Thermea Group

- 9.5 Bosch Industriekessel

- 9.6 Bradford White Corporation

- 9.7 BURNHAM COMMERCIAL BOILERS

- 9.8 Cleaver-Brooks

- 9.9 Daikin

- 9.10 FERROLI

- 9.11 FONDITAL

- 9.12 Hoval

- 9.13 Immergas

- 9.14 Lochinvar

- 9.15 Remeha

- 9.16 Vaillant Group

- 9.17 VIESSMANN

- 9.18 Weil-McLain