|

市場調査レポート

商品コード

1750506

亜鉛めっきおよびコーティング鉄・鋼板の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Galvanized And Coated Iron and Steel Sheets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 亜鉛めっきおよびコーティング鉄・鋼板の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月13日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

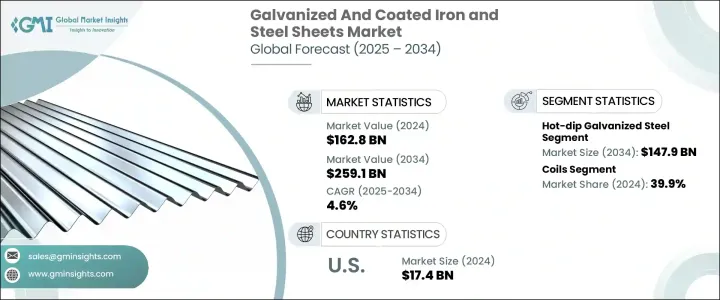

世界の亜鉛めっきおよびコーティング鉄・鋼板市場は、2024年に1,628億米ドルと評価され、自動車、建設、消費財などの産業からの需要の急増により、CAGR4.6%で成長し、2034年までには2,591億米ドルに達すると推定されています。

先進国や新興経済諸国における急速な都市化と産業拡大が、耐久性と耐食性に優れた鋼材の需要を後押ししています。これらの鋼板は長寿命、構造的完全性、費用対効果を提供し、頑丈で長期的な用途に不可欠です。

さらに、耐食性、耐久性、美観を向上させる高度な表面処理の開発により、亜鉛めっきおよびコーティング鉄・鋼板の応用範囲が拡大しています。メーカー各社は、製造時の有害物質の排出とエネルギー消費を削減する、環境に優しいコーティング処方を取り入れています。これは、より環境に優しい建築材料や製造材料を求める規制の圧力や顧客の要求の高まりと一致しています。その結果、これらの技術革新は性能を向上させるだけでなく、持続可能性基準への準拠をサポートし、建設、自動車、工業用途での使用を世界的に魅力的なものにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 1,628億米ドル |

| 予測金額 | 2,591億米ドル |

| CAGR | 4.6% |

同市場では、溶融亜鉛メッキ鋼板が引き続き最も広く使用されている塗装技術です。この分野は2024年に957億米ドルを生み出し、2034年には1,479億米ドルに達すると予測されています。溶融亜鉛メッキの優位性は、優れた耐久性、長期的な腐食保護、手頃な価格から生じています。溶融亜鉛メッキは、亜鉛と鋼鉄の結合を形成し、過酷な環境下でもシールドとして機能するため、農業、インフラ、輸送、工業プロジェクトなどでの衝撃の大きい用途に理想的な材料です。

コイル状の亜鉛メッキ鋼板および塗装鋼板は、輸送の容易さと在庫コストの削減により、大規模ユーザーの間で依然として人気のある選択肢です。2024年のコイルセグメントのシェアは39.9%でした。コイルは現場で特定の寸法に加工できるため、廃棄物を最小限に抑え、材料使用量を最適化できます。こうした特性から、自動車生産ライン、モジュール式住宅プロジェクト、プレハブ構造物における合理化作業に最適です。さらに、亜鉛メッキコイルは、グリーンでエネルギー効率の高い建設への関心の高まりに伴い、塗装および美観グレードの建築部材の主要原材料としての需要が高まっています。

米国の亜鉛めっきおよびコーティング鉄・鋼板市場は2024年に174億米ドルとなり、2034年までのCAGRは4.9%と予想されます。堅調な需要を牽引しているのは、耐食性と材料寿命の延長が重要な要件である同国の自動車およびインフラセクターの拡大です。橋梁、商業ビル、輸送網などのプロジェクトでは、様々な環境下での弾力性と性能により、これらの鋼材の採用が続いています。

この市場の主要企業には、POSCO、ArcelorMittal、Baowu Steel Group、TATA Steel、Nippon Steel Corporationなどがあります。これらの企業は、高度な亜鉛メッキ技術への投資、生産能力の拡大、最終用途産業との戦略的パートナーシップの形成により、競争力を強化しています。コスト削減と長期的な拡張性をサポートするため、環境に配慮した方法と製造の自動化が重視されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 亜鉛めっきおよびコーティング鉄・鋼板:基礎と進化

- 亜鉛メッキ鋼・塗装鋼板製品の定義と分類

- コーティング技術の歴史的開発

- 原材料と構成

- ベース鋼の種類と特性

- 亜鉛・亜鉛合金

- アルミニウム・アルミニウム亜鉛合金

- ポリマー・有機コーティング

- その他のコーティング材

- 製造プロセス

- 溶融亜鉛メッキ

- 電気亜鉛メッキ

- ガルバニーリング

- アルミメッキ・ガルバリウムコーティング

- 塗装前・カラーコーティング

- その他のコーティング技術

- 比較分析:亜鉛メッキ鋼とその他の塗装鋼板製品

- コーティングプロセスにおける技術的進歩

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国、2021-2024

- 主要輸入国、2021-2024

- 要約

- 市場概要主な調査結果

- 市場規模と成長予測

- 主要な市場促進要因と制約

- 競合情勢のスナップショット

- 投資機会と戦略的提言

- 将来の見通しと市場の可能性

- 世界亜鉛メッキ鋼板市場概要

- 市場の定義と範囲

- 市場規模と成長分析

- 市場力学

- 市場促進要因

- 耐腐食性材料の需要増加

- 建設とインフラ開発の拡大

- 自動車生産の増加と軽量化の動向

- 再生可能エネルギーアプリケーションにおける採用の増加

- 市場抑制要因

- 原材料価格の変動

- 代替材料の競合

- 環境問題と規制上の課題

- 市場機会

- 新興市場における需要の増加

- コーティング技術の革新

- 再生可能エネルギーインフラの拡大

- 市場の課題

- 厳しい環境規制

- サプライチェーンの混乱

- 変動するエネルギーコスト

- 市場促進要因

- COVID-19の影響とパンデミック後の回復

- ポーターのファイブフォース分析

- PESTEL分析

- バリューチェーン分析

- 原材料サプライヤー

- 製造業者

- 販売業者と小売業者

- エンドユーザー

- 製造・生産分析

- 製造プロセスの概要

- 原材料の調達と準備

- ファンデーション鉄鋼生産

- 表面処理

- コーティング塗布プロセス

- コーティング後の処理

- 品質管理とテスト

- 生産コスト分析

- 原材料費

- エネルギーコスト

- 人件費

- 製造間接費

- コスト最適化戦略

- 製造施設分析

- 主要製造拠点

- 生産能力評価

- 施設拡張計画

- サプライチェーンの課題と解決策

- 製造プロセスにおける持続可能性

- エネルギー効率対策

- 廃棄物削減戦略

- 節水対策

- 環境に優しいコーティング技術

- 製造プロセスの概要

- 規制状況と基準

- 世界の規制枠組み

- 地域規制枠組み

- 北米

- ASTM規格

- 建築基準法と規制

- 環境規制

- 欧州

- EN規格

- CEマーキング要件

- 環境規制

- アジア太平洋

- JIS規格(日本)

- GB規格(中国)

- BIS規格(インド)

- 世界のその他の地域

- 北米

- 製品認証と規格

- 品質基準

- 安全基準

- 環境基準

- コンプライアンスの課題と戦略

- 将来の規制動向とその影響

- 環境・社会・ガバナンス(ESG)分析

- 環境影響評価

- カーボンフットプリント分析

- ライフサイクルアセスメント(LCA)

- エネルギー消費と排出量

- 廃棄物管理とリサイクル

- 社会的影響

- 労働慣行と労働条件

- コミュニティへの影響と関与

- 健康と安全に関する考慮事項

- ガバナンスと倫理的配慮

- コーポレートガバナンスの実践

- 倫理的なサプライチェーン管理

- 透明性と報告

- 主要企業のESGパフォーマンスベンチマーク

- ESGリスク評価と軽減戦略

- 亜鉛メッキ鋼板および塗装鋼板業界における将来のESG動向

- 環境影響評価

- 消費者行動と市場動向の分析

- 消費者の嗜好と購買パターン

- 購入決定に影響を与える要因

- 価格感度

- 品質とパフォーマンスの要件

- 環境への配慮

- 美的選好

- 業界固有の好み

- 建設業界の好み

- 自動車業界の好み

- 家電業界の好み

- 消費者行動の地域差

- デジタル変革が消費者エンゲージメントに与える影響

- 将来の消費者動向とその影響

- 技術的情勢とイノベーション分析

- 亜鉛メッキ鋼・塗装鋼板の現在の技術動向

- 新興技術とその潜在的な影響

- 高度なコーティング配合

- ナノテクノロジーの応用

- デジタル製造とインダストリー4.0

- コーティング工程における自動化とロボット工学

- 研究開発活動とイノベーションハブ

- アプリケーション全体にわたる技術採用動向

- 技術準備状況評価

- 将来の技術ロードマップ、2025年~2033年

- 価格分析と経済的要因

- 価格動向分析

- 歴史的価格動向

- 現在の価格シナリオ

- 価格予測

- 価格に影響を与える要因

- 原材料費

- エネルギー価格

- 人件費

- 需給動向

- 貿易政策と関税

- 地域による価格差

- 価格と価値の関係分析

- 市場に影響を与える経済指標

- GDP成長と建設活動

- 工業生産指数

- 自動車生産動向

- インフラ投資

- 主要市場企業の価格戦略

- 価格動向分析

- 持続可能性と循環型経済

- 持続可能な原材料調達

- 生産におけるエネルギー効率

- 廃棄物削減とリサイクルの取り組み

- 二酸化炭素排出量削減戦略

- 亜鉛メッキ鋼および塗装鋼板の循環型経済モデル

- 製品寿命延長戦略

- 終末期管理

- リサイクルとアップサイクルの機会

- 持続可能な実践の事例研究

- 業界における持続可能性の未来

- 市場機会と戦略的提言

- 未開拓の市場機会

- 市場参入企業への戦略的提言

- メーカー向け

- 投資家向け

- エンドユーザー産業向け

- 新製品開発の機会

- 新規参入者の市場参入戦略

- 多様化の機会

- 戦略的パートナーシップとコラボレーションの機会

- 投資分析と市場の魅力

- 現在の投資シナリオ

- セグメント別の投資機会

- 地域別の投資機会

- ROI分析

- ベンチャーキャピタルとプライベートエクイティの情勢

- M&A活動分析

- 将来の投資見通し

- リスク評価と軽減戦略

- 市場リスク

- 技術的リスク

- 規制リスク

- 競争リスク

- サプライチェーンのリスク

- 環境と持続可能性のリスク

- リスク軽減戦略

- 将来の見通しと市場の進化

- 長期市場予測

- 新しいアプリケーションとユースケース

- 技術進化のシナリオ

- 将来の市場力学

- 潜在的な破壊者とゲームチェンジャー

- 将来の競合情勢

第4章 競合情勢

- 主要企業の市場シェア分析

- 競合ポジショニングマトリックス

- 採用している競争戦略:主要企業別

- 製品の革新と開発

- 合併と買収

- パートナーシップとコラボレーション

- 拡大戦略

- 主要企業のSWOT分析

- 主要市場企業の詳細な企業プロファイル

- ArcelorMittal

- Nippon steel corporation

- POSCO

- Tata steel

- Baowu steel group

- JFE steel corporation

- Nucor corporation

- Thyssenkrupp

- United States steel corporation

- Cleveland-cliffs

- Steel dynamics

- Hyundai steel

- Bluescope steel

- Jindal steel & power

- その他の主要企業

- 亜鉛めっきおよびコーティング鉄・鋼板市場における新興企業とスタートアップ企業

- 特許分析と知的財産の情勢

- 最近の特許出願

- 特許所有権分析

- 特許に基づく技術動向分析

第5章 市場規模・予測:コーティングタイプ別、2021年~2034年

- 主要動向

- 溶融亜鉛メッキ鋼

- 電気亜鉛メッキ鋼

- 亜鉛メッキ鋼

- ガルバリュム(亜鉛アルミニウムコーティング)鋼

- アルミニウムメッキ鋼

- 塗装済み亜鉛メッキ鋼板(PPGI)

- その他

第6章 市場規模・予測:製品形態別、2021年~2034年

- 主要動向

- コイル

- シート

- プレート

- バー・ワイヤー

- その他

第7章 市場規模・予測:塗工量別、2021年~2034年

- 主要動向

- ライトコーティング(G30~G60)

- ミディアムコーティング(G90~G235)

- ヘビーコーティング(G240以上)

第8章 市場規模・予測:ベース鋼グレード別、2021年~2034年

- 主要動向

- 商業用鋼

- 鋼材の引抜き

- 構造用鋼

- 高強度低合金鋼(HSLA)

- 先進高強度鋼(AHSS)

- その他

第9章 市場規模・予測:最終用途産業別、2021年~2034年

- 主要動向

- 建設・インフラ

- 住宅建設

- 商業建設

- 産業建設

- インフラ開発

- 自動車・輸送

- 乗用車

- 商用車

- 鉄道・地下鉄システム

- 造船

- 家電製品・電子機器

- 白物家電

- HVACシステム

- 電子機器の筐体

- エネルギー・電力

- 太陽エネルギーシステム

- 風力エネルギーインフラ

- 送電・配電

- 農業

- 産業機器・機械

- その他

第10章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 屋根材・外壁材

- 構造部品

- 自動車ボディ部品

- 家電製品の筐体

- 電気配管・筐体

- HVACダクト

- その他

第11章 市場規模・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 販売代理店・サービスセンター

- 小売店

- eコマース

- その他

第12章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ

第13章 企業プロファイル

- ArcelorMittal

- Nippon Steel Corporation

- POSCO

- Tata Steel

- Baowu Steel

- JFE Steel Corporation

- Nucor Corporation

- ThyssenKrupp

- United States Steel

- Cleveland-Cliffs

- Steel Dynamics

- Hyundai Steel

- BlueScope Steel

- Jindal Steel &Power

The Global Galvanized And Coated Iron and Steel Sheets Market was valued at USD 162.8 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 259.1 billion by 2034, shaped by the surge in demand from industries such as automotive, construction, and consumer goods. Rapid urbanization and industrial expansion in developed and emerging economies help boost demand for durable and corrosion-resistant steel materials. These sheets offer longevity, structural integrity, and cost-effectiveness, essential in heavy-duty and long-term applications.

Additionally, the development of advanced surface treatments that enhance corrosion resistance, durability, and aesthetic appeal is expanding the application range of galvanized and coated iron and steel sheets. Manufacturers incorporate eco-friendly coating formulations that reduce toxic emissions and energy consumption during production. This aligns with growing regulatory pressures and customer demand for greener building and manufacturing materials. As a result, these innovations not only improve performance but also support compliance with sustainability standards, making them more appealing for use in construction, automotive, and industrial applications globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $162.8 Billion |

| Forecast Value | $259.1 Billion |

| CAGR | 4.6% |

Within the market, hot-dip galvanized steel continues to be the most widely used coating technique. This segment generated USD 95.7 billion in 2024 and is projected to reach USD 147.9 billion by 2034. Its dominance stems from superior durability, long-term corrosion protection, and affordability. The hot-dip process creates a zinc-steel bond that acts as a shield in aggressive environments, making it an ideal material for high-impact use in agriculture, infrastructure, transportation, and industrial projects.

Galvanized and coated steel in coil form remains a popular choice among large-scale users due to its ease of transportation and reduced inventory costs. In 2024, the coils segment accounted for a 39.9% share. Coils can be processed into specific dimensions on-site, minimizing waste and optimizing material usage. These characteristics make them ideal for streamlined operations in automotive production lines, modular housing projects, and prefabricated structures. Additionally, galvanized coils are seeing heightened demand as key raw materials in painted and aesthetic-grade building components, aligning with growing interest in green and energy-efficient construction.

United States Galvanized And Coated Iron and Steel Sheets Market stood at USD 17.4 billion in 2024 and is expected to register a CAGR of 4.9% through 2034. Robust demand is driven by the country's expanding automotive and infrastructure sectors, where corrosion resistance and extended material lifespan are critical requirements. Projects in bridges, commercial buildings, and transport networks continue to adopt these steel products due to their resilience and performance in various environments.

Key players in this market include POSCO, ArcelorMittal, Baowu Steel Group, TATA Steel, and Nippon Steel Corporation. These companies are strengthening their competitive edge by investing in advanced galvanizing technology, expanding production capacities, and forming strategic partnerships with end-use industries. A strong emphasis is placed on environmentally responsible methods and automation in manufacturing to reduce costs and support long-term scalability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Report scope and objectives

- 1.2 Research design and approach

- 1.3 Data collection methods

- 1.3.1 Primary research

- 1.3.2 Secondary research

- 1.4 Market estimation and forecasting methodology

- 1.5 Assumptions and limitations

- 1.6 Data validation and triangulation techniques

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Galvanized and coated steel: fundamentals and evolution

- 3.1.1 Definition and classification of galvanized and coated steel products

- 3.1.2 Historical development of coating technologies

- 3.1.3 Raw materials and composition

- 3.1.3.1 Base steel types and properties

- 3.1.3.2 Zinc and zinc alloys

- 3.1.3.3 Aluminum and aluminum-zinc alloys

- 3.1.3.4 Polymers and organic coatings

- 3.1.3.5 Other coating materials

- 3.1.4 Manufacturing processes

- 3.1.4.1 Hot-dip galvanizing

- 3.1.4.2 Electro galvanizing

- 3.1.4.3 Galvannealing

- 3.1.4.4 Aluminizing and galvalume coating

- 3.1.4.5 Pre-painting and color coating

- 3.1.4.6 Other coating technologies

- 3.1.5 Comparative analysis: galvanized vs. Other coated steel products

- 3.1.6 Technological advancements in coating processes

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (USD Mn)

- 3.3.2 Major importing countries, 2021-2024 (USD Mn)

- 3.4 Summary

- 3.4.1 Market overview and key findings

- 3.4.2 Market size and growth projections

- 3.4.3 Key market drivers and restraints

- 3.4.4 Competitive landscape snapshot

- 3.4.5 Investment opportunities and strategic recommendations

- 3.4.6 Future outlook and market potential

- 3.5 Global galvanized and coated steel market overview

- 3.5.1 Market definition and scope

- 3.5.2 Market size and growth analysis

- 3.5.3 Market dynamics

- 3.5.3.1 Market drivers

- 3.5.3.1.1 Growing demand for corrosion-resistant materials

- 3.5.3.1.2 Expansion in construction and infrastructure development

- 3.5.3.1.3 Rising automotive production and lightweight trends

- 3.5.3.1.4 Increasing adoption in renewable energy applications

- 3.5.3.2 Market restraints

- 3.5.3.2.1 Volatility in raw material prices

- 3.5.3.2.2 Competition of alternative materials

- 3.5.3.2.3 Environmental concerns and regulatory challenges

- 3.5.3.3 Market opportunities

- 3.5.3.3.1 Growing demand in emerging markets

- 3.5.3.3.2 Innovations in coating technologies

- 3.5.3.3.3 Expansion in renewable energy infrastructure

- 3.5.3.4 Market challenges

- 3.5.3.4.1 Stringent Environmental Regulations

- 3.5.3.4.2 Supply chain disruptions

- 3.5.3.4.3 Fluctuating energy costs

- 3.5.3.1 Market drivers

- 3.5.4 Impact of covid-19 and post-pandemic recovery

- 3.5.5 Porter's five forces analysis

- 3.5.6 Pestle analysis

- 3.5.7 Value chain analysis

- 3.5.7.1 Raw material suppliers

- 3.5.7.2 Manufacturers

- 3.5.7.3 Distributors and retailers

- 3.5.7.4 End users

- 3.6 Manufacturing and production analysis

- 3.6.1 Manufacturing process overview

- 3.6.1.1 Raw material procurement and preparation

- 3.6.1.2 Base steel production

- 3.6.1.3 Surface preparation

- 3.6.1.4 Coating application processes

- 3.6.1.5 Post-coating treatments

- 3.6.1.6 Quality control and testing

- 3.6.2 Production cost analysis

- 3.6.2.1 Raw material costs

- 3.6.2.2 Energy costs

- 3.6.2.3 Labor costs

- 3.6.2.4 Manufacturing overheads

- 3.6.2.5 Cost optimization strategies

- 3.6.3 Manufacturing facilities analysis

- 3.6.3.1 Key manufacturing locations

- 3.6.3.2 Production capacity assessment

- 3.6.3.3 Facility expansion plans

- 3.6.4 Supply chain challenges and solutions

- 3.6.5 Sustainability in manufacturing processes

- 3.6.5.1 Energy efficiency measures

- 3.6.5.2 Waste reduction strategies

- 3.6.5.3 Water conservation practices

- 3.6.5.4 Eco-friendly coating technologies

- 3.6.1 Manufacturing process overview

- 3.7 Regulatory landscape and standards

- 3.7.1 Global regulatory framework

- 3.7.2 Regional regulatory frameworks

- 3.7.2.1 North America

- 3.7.2.1.1 ASTM standards

- 3.7.2.1.2 Building codes and regulations

- 3.7.2.1.3 Environmental regulations

- 3.7.2.2 Europe

- 3.7.2.2.1 EN standards

- 3.7.2.2.2 CE marking requirements

- 3.7.2.2.3 Environmental regulations

- 3.7.2.3 Asia-pacific

- 3.7.2.3.1 JIS standards (Japan)

- 3.7.2.3.2 GB standards (China)

- 3.7.2.3.3 BIS standards (India)

- 3.7.2.4 Rest of the world

- 3.7.2.1 North America

- 3.7.3 Product certification and standards

- 3.7.3.1 Quality standards

- 3.7.3.2 Safety standards

- 3.7.3.3 Environmental standards

- 3.7.4 Compliance challenges and strategies

- 3.7.5 Future regulatory trends and their implications

- 3.8 Environmental, social, and governance (ESG) analysis

- 3.8.1 Environmental impact assessment

- 3.8.1.1 Carbon footprint analysis

- 3.8.1.2 Life cycle assessment (LCA)

- 3.8.1.3 Energy consumption and emissions

- 3.8.1.4 Waste management and recycling

- 3.8.2 Social implications

- 3.8.2.1 Labor practices and working conditions

- 3.8.2.2 Community impact and engagement

- 3.8.2.3 Health and safety considerations

- 3.8.3 Governance and ethical considerations

- 3.8.3.1 Corporate governance practices

- 3.8.3.2 Ethical supply chain management

- 3.8.3.3 Transparency and reporting

- 3.8.4 ESG performance benchmarking of key players

- 3.8.5 ESG risk assessment and mitigation strategies

- 3.8.6 Future ESG trends in the galvanized and coated steel industry

- 3.8.1 Environmental impact assessment

- 3.9 Consumer behavior and market trends analysis

- 3.9.1 Consumer preferences and purchasing patterns

- 3.9.2 Factors influencing purchase decisions

- 3.9.2.1 Price sensitivity

- 3.9.2.2 Quality and performance requirements

- 3.9.2.3 Environmental considerations

- 3.9.2.4 Aesthetic preferences

- 3.9.3 Industry-specific preferences

- 3.9.3.1 Construction industry preferences

- 3.9.3.2 Automotive industry preferences

- 3.9.3.3 Appliance industry preferences

- 3.9.4 Regional variations in consumer behavior

- 3.9.5 Impact of digital transformation on consumer engagement

- 3.9.6 Future consumer trends and their implications

- 3.10 Technological landscape and innovation analysis

- 3.10.1 Current technological trends in galvanized and coated steel

- 3.10.2 Emerging technologies and their potential impact

- 3.10.2.1 Advanced coating formulations

- 3.10.2.2 Nanotechnology applications

- 3.10.2.3 Digital manufacturing and industry 4.0

- 3.10.2.4 Automation and robotics in coating processes

- 3.10.3 R&D activities and innovation hubs

- 3.10.4 Technology adoption trends across applications

- 3.10.5 Technology readiness assessment

- 3.10.6 Future technology roadmap 2025–2033

- 3.11 Pricing analysis and economic factors

- 3.11.1 Pricing trends analysis

- 3.11.1.1 Historical price trends

- 3.11.1.2 Current pricing scenario

- 3.11.1.3 Price forecast

- 3.11.2 Factors affecting pricing

- 3.11.2.1 Raw material costs

- 3.11.2.2 Energy prices

- 3.11.2.3 Labor costs

- 3.11.2.4 Supply-demand dynamics

- 3.11.2.5 Trade policies and tariffs

- 3.11.3 Regional price variations

- 3.11.4 Price-value relationship analysis

- 3.11.5 Economic indicators impacting the market

- 3.11.5.1 GDP growth and construction activity

- 3.11.5.2 Industrial production index

- 3.11.5.3 Automotive production trends

- 3.11.5.4 Infrastructure investment

- 3.11.6 Pricing strategies for key market players

- 3.11.1 Pricing trends analysis

- 3.12 Sustainability and circular economy

- 3.12.1 Sustainable sourcing of raw materials

- 3.12.2 Energy efficiency in production

- 3.12.3 Waste reduction and recycling initiatives

- 3.12.4 Carbon footprint reduction strategies

- 3.12.5 Circular economy models in galvanized and coated steel

- 3.12.5.1 Product life extension strategies

- 3.12.5.2 End-of-life management

- 3.12.5.3 Recycling and upcycling opportunities

- 3.12.6 Case studies of sustainable practices

- 3.12.7 Future of sustainability in the industry

- 3.13 Market opportunities and strategic recommendations

- 3.13.1 Untapped market opportunities

- 3.13.2 Strategic recommendations for market participants

- 3.13.2.1 For manufacturers

- 3.13.2.2 For investors

- 3.13.2.3 For end-user industries

- 3.13.3 New product development opportunities

- 3.13.4 Market entry strategies for new players

- 3.13.5 Diversification opportunities

- 3.13.6 Strategic partnerships and collaboration opportunities

- 3.14 Investment analysis and market attractiveness

- 3.14.1 Current investment scenario

- 3.14.2 Investment opportunities by segment

- 3.14.3 Investment opportunities by region

- 3.14.4 Roi analysis

- 3.14.5 Venture capital and private equity landscape

- 3.14.6 M&A activity analysis

- 3.14.7 Future investment outlook

- 3.15 Risk assessment and mitigation strategies

- 3.15.1 Market risks

- 3.15.2 Technological risks

- 3.15.3 Regulatory risks

- 3.15.4 Competitive risks

- 3.15.5 Supply chain risks

- 3.15.6 Environmental and sustainability risks

- 3.15.7 Risk mitigation strategies

- 3.16 Future outlook and market evolution

- 3.16.1 Long-term market forecast

- 3.16.2 Emerging applications and use cases

- 3.16.3 Technological evolution scenarios

- 3.16.4 Future market dynamics

- 3.16.5 Potential disruptors and game-changers

- 3.16.6 Future competitive landscape

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis of key players

- 4.2 Competitive positioning matrix

- 4.3 Competitive strategies adopted by key players

- 4.3.1 Product innovation and development

- 4.3.2 Mergers and acquisitions

- 4.3.3 Partnerships and collaborations

- 4.3.4 Expansion strategies

- 4.4 Swot analysis of key players

- 4.5 Detailed company profiles of major market players

- 4.5.1 ArcelorMittal

- 4.5.2 Nippon steel corporation

- 4.5.3 POSCO

- 4.5.4 Tata steel

- 4.5.5 Baowu steel group

- 4.5.6 JFE steel corporation

- 4.5.7 Nucor corporation

- 4.5.8 Thyssenkrupp

- 4.5.9 United States steel corporation

- 4.5.10 Cleveland-cliffs

- 4.5.11 Steel dynamics

- 4.5.12 Hyundai steel

- 4.5.13 Bluescope steel

- 4.5.14 Jindal steel & power

- 4.5.15 Other notable players

- 4.6 Emerging players and startups in galvanized and coated steel market

- 4.7 Patent analysis and intellectual property landscape

- 4.7.1 Recent patent filings

- 4.7.2 Patent ownership analysis

- 4.7.3 Technology trend analysis based on patents

Chapter 5 Market Size and Forecast, By Coating Type, 2021-2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Hot-dip galvanized steel

- 5.3 Electrogalvanized steel

- 5.4 Galvannealed steel

- 5.5 Galvalume (zinc-aluminum coated) steel

- 5.6 Aluminized steel

- 5.7 Pre-painted galvanized steel (PPGI)

- 5.8 Other

Chapter 6 Market Size and Forecast, By Product Form, 2021-2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Coils

- 6.3 Sheets

- 6.4 Plates

- 6.5 Bars and wires

- 6.6 Others

Chapter 7 Market Size and Forecast, By Coating Weight, 2021-2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Light coating (G30–G60)

- 7.3 Medium coating (G90–G235)

- 7.4 Heavy coating (G240 and above)

Chapter 8 Market Size and Forecast, By Base Steel Grade, 2021-2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 Commercial steel

- 8.3 Drawing steel

- 8.4 Structural steel

- 8.5 High-strength low-alloy steel (HSLA)

- 8.6 Advanced high-strength steel (AHSS)

- 8.7 Others

Chapter 9 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Million) (Tons)

- 9.1 Key trends

- 9.2 Construction and infrastructure

- 9.2.1 Residential construction

- 9.2.2 Commercial construction

- 9.2.3 Industrial construction

- 9.2.4 Infrastructure development

- 9.3 Automotive and transportation

- 9.3.1 Passenger vehicles

- 9.3.2 Commercial vehicles

- 9.3.3 Railway and metro systems

- 9.3.4 Shipbuilding

- 9.4 Home appliances and electronics

- 9.4.1 White goods

- 9.4.2 HVAC systems

- 9.4.3 Electronic enclosures

- 9.5 Energy and power

- 9.5.1 Solar energy systems

- 9.5.2 Wind energy infrastructure

- 9.5.3 Power transmission and distribution

- 9.6 Agriculture

- 9.7 Industrial equipment and machinery

- 9.8 Others

Chapter 10 Market Size and Forecast, By Specific Applications, 2021-2034 (USD Million) (Tons)

- 10.1 Key trends

- 10.2 Roofing and cladding

- 10.3 Structural components

- 10.4 Automotive body parts

- 10.5 Appliance casings

- 10.6 Electrical conduits and enclosures

- 10.7 HVAC ductwork

- 10.8 Others

Chapter 11 Market Size and Forecast, By Distribution Channel, 2021-2034 (USD Million) (Tons)

- 11.1 Key trends

- 11.2 Direct sales

- 11.3 Distributors and service centers

- 11.4 Retail outlets

- 11.5 E-commerce

- 11.6 Others

Chapter 12 Market Size and Forecast, By Region, 2021-2034 (USD Million) (Tons)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Rest of Europe

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Rest of Asia Pacific

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Rest of Latin America

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

- 12.6.4 Rest of Middle East & Africa

Chapter 13 Company Profiles

- 13.1 ArcelorMittal

- 13.2 Nippon Steel Corporation

- 13.3 POSCO

- 13.4 Tata Steel

- 13.5 Baowu Steel

- 13.6 JFE Steel Corporation

- 13.7 Nucor Corporation

- 13.8 ThyssenKrupp

- 13.9 United States Steel

- 13.10 Cleveland-Cliffs

- 13.11 Steel Dynamics

- 13.12 Hyundai Steel

- 13.13 BlueScope Steel

- 13.14 Jindal Steel & Power