船舶交通管理の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Vessel Traffic Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750502

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

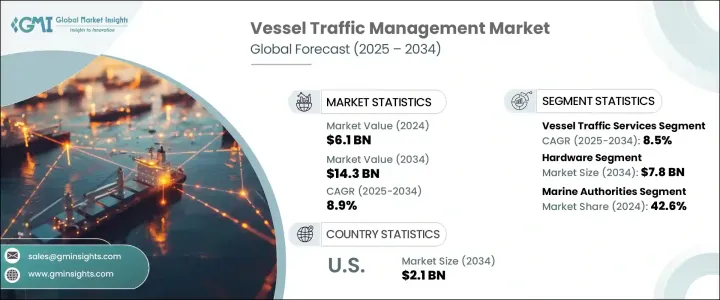

船舶交通管理の世界市場規模は、2024年に61億米ドルとなり、増加する船舶量を効率的かつ安全に処理できる、よりスマートな交通システムへの需要に牽引され、CAGR 8.9%で成長し、2034年には143億米ドルに達すると推定されます。

世界の港湾インフラは、船舶の動きの増加により圧力を受けており、航行を強化し、ボトルネックを解消し、港湾運営を強化する高性能システムの採用を促進しています。国際的な貿易政策や資材価格の変動に起因する業界のシフトにより、企業は地政学的リスクを軽減するため、生産を現地化し、サプライチェーン戦略を見直す必要に迫られています。港湾が混雑の激化に直面する中、安全規制の遵守を確保しながらオペレーションを合理化できる技術の必要性は、これまで以上に高まっています。

この市場は、混雑した航路におけるリアルタイム船舶モニタリングのニーズの高まりに大きな影響を受けています。レーダー、VHF通信、自動識別技術を組み込んだ強化船舶交通管理システムは、商業および防衛の両海事当局にとって不可欠なものとなっています。これらのシステムにより、シームレスな連携、状況認識、高密度の交通ゾーンをより安全に航行することが可能になります。デジタル海事インフラへの関心の高まりと、港湾警備・監視システムへの投資の増加により、船舶交通サービス(Vessel Traffic Services)というセグメントが大きな牽引力となっています。環境リスクの最小化と海上ロジスティクスの改善に重点を置く中、インテリジェントでコネクテッドなテクノロジーへの需要が地域間で急増しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 61億米ドル |

| 予測金額 | 143億米ドル |

| CAGR | 8.9% |

コンポーネントの観点からは、ハードウェアが船舶交通管理エコシステムにおいて強い存在感を示しており、2034年までに78億米ドルに達すると予測されています。これには、センサー、レーダー、通信モジュールなど、データ収集と伝送に必要な幅広い海事機器が含まれます。船舶の安全性に関する規制強化が引き続きこの需要を後押ししています。ハードウェアが支配的ではあるが、港湾がデータ分析、遠隔管理、予知保全を含む統合ソリューションを求めていることから、サービス分野は加速度的に成長する見通しです。

最終用途別では、船舶の安全性と環境基準を規制する重要な役割を担う海事当局セグメントが2024年に42.6%のシェアを占め、このセグメントを支配しています。これらの当局は、船舶交通の管理を強化し、国内および国際水域での円滑な運航を確保するために船舶交通システムに目を向けています。レーダー、AIS、統合通信システムなどのリアルタイム監視ツールに依存することで、海上のリスクを積極的に管理し、混雑を緩和し、緊急事態に迅速に対応することができます。

米国の船舶交通管理市場は、より厳格な安全プロトコルの推進と最先端のVTMS導入に支えられ、2034年までに21億米ドルに達すると予想されます。連邦政府の義務付けと沿岸警備隊のイニシアティブにより、交通量の多いゾーンでの最新監視システムの展開が加速しています。さらに、港湾インフラのアップグレードとAI駆動型ツールの統合を重視する国の姿勢が、インテリジェントVTMプラットフォームへの一貫した需要に拍車をかけています。しかし、貿易の不確実性や地政学的緊張と相まって、小規模な港湾運営者の間では予算の制約があり、特定の地域における急速な拡大の障壁となっています。

競争力を強化するため、Northrop Grumman Corporation、Leonardo S.p.A.、Kongsberg Gruppen、ST Engineering、Saab ABなどの企業は、研究とイノベーションに多額の投資を行っています。これらの企業は、人工知能、IoT、予測分析を活用して、よりスマートでスケーラブルな船舶交通管理ソリューションを提供しています。政府や港湾当局とのコラボレーションも、将来性の高い市場へのアクセスを得るために優先されています。多くのプレーヤーは、世界的に増大する業務の複雑性と規制上の要求に対応するため、エンドツーエンドのVTMS機能を備えたサービス・ポートフォリオを強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 成長

- 世界の海上貿易量の増加

- 港湾混雑と業務効率化の需要の増加

- AI、ML、リアルタイム監視技術の進歩

- 厳格な海上安全および環境規制

- 港湾インフラの近代化への投資

- 業界の潜在的リスク&課題

- 設置および保守コストが高め

- レガシーシステムと最新システム間の相互運用性が限られている

- 成長

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:システムタイプ別、2021 –2034

- 主要動向

- 船舶交通サービス(VTS)

- 港湾管理システム(PMS)

- 自動識別システム(AIS)

- レーダーベースのシステム

第6章 市場推計・予測:コンポーネント別、2021 –2034

- 主要動向

- ハードウェア

- ソフトウェア

- サービス

第7章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 海事当局

- 港湾

- 商業船舶運航業者

- 海軍

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Elcome International LLC

- Frequentis

- Furuno

- Hensoldt

- Indra Sistemas

- Japan Radio Co. Ltd.

- Kongsberg Gruppen

- Leonardo S.p.A.

- Marlink AS

- Northrop Grumman Corporation

- Saab

- ST Engineering

- Terma

- Thales Group

- Wartsila

目次

The Global Vessel Traffic Management Market was valued at USD 6.1 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 14.3 billion by 2034, driven by the demand for smarter traffic systems capable of handling increasing vessel volumes efficiently and safely. Global port infrastructure is under pressure due to growing ship movements, driving the adoption of high-performance systems that enhance navigation, reduce bottlenecks, and boost port operations. Industry shifts caused by international trade policies and material price volatility prompt companies to localize production and rethink their supply chain strategies to reduce geopolitical risks. As ports face rising congestion, the need for technologies that can streamline operations while ensuring compliance with safety regulations is more important than ever.

The market is heavily influenced by the rising need for real-time ship monitoring in congested sea routes. Enhanced vessel traffic management systems that incorporate radar, VHF communications, and automatic identification technologies are becoming essential for both commercial and defense maritime authorities. These systems enable seamless coordination, situational awareness, and safer navigation through high-density traffic zones. One segment, Vessel Traffic Services, is experiencing significant traction due to growing interest in digital maritime infrastructure and increasing investments in port security and surveillance systems. With a focus on minimizing environmental risk and improving maritime logistics, demand for intelligent and connected technologies is surging across regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.1 Billion |

| Forecast Value | $14.3 Billion |

| CAGR | 8.9% |

From a component standpoint, hardware holds a strong presence in the vessel traffic management ecosystem and is forecasted to hit USD 7.8 billion by 2034. This includes a wide range of maritime equipment necessary for data collection and transmission, such as sensors, radar, and communication modules. Tighter regulatory enforcement for ship safety continues to drive this demand. Although hardware dominates, the services segment is poised for accelerated growth as ports look for integrated solutions that include data analytics, remote management, and predictive maintenance.

Based on end-use, the marine authorities segment accounted for a 42.6% share in 2024, dominating the segment due to their critical role in regulating navigation safety and environmental standards. These authorities turn to vessel traffic systems to enhance control over ship traffic and ensure smooth operations in national and international waters. The reliance on real-time monitoring tools like radar, AIS, and integrated communications systems allows them to proactively manage maritime risks, mitigate congestion, and respond swiftly to emergencies.

U.S. Vessel Traffic Management Market is expected to reach USD 2.1 billion by 2034, supported by the push for stricter safety protocols and cutting-edge VTMS deployments. Federal mandates and Coast Guard initiatives have accelerated the rollout of modern monitoring systems across high-traffic zones. Furthermore, the nation's emphasis on upgrading port infrastructure and integrating AI-driven tools has spurred consistent demand for intelligent VTM platforms. However, budget constraints among smaller port operators, coupled with trade uncertainties and geopolitical tensions, remain barriers to rapid expansion in certain regions.

To solidify their competitive edge, companies like Northrop Grumman Corporation, Leonardo S.p.A., Kongsberg Gruppen, ST Engineering, and Saab AB are investing heavily in research and innovation. They leverage artificial intelligence, IoT, and predictive analytics to deliver smarter, scalable vessel traffic management solutions. Collaborations with governments and port authorities are also prioritized to gain access to high-potential markets. Many players are enhancing their service portfolios with end-to-end VTMS capabilities to address growing operational complexity and regulatory demands globally.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth

- 3.3.1.1.1 Rising global maritime trade volumes

- 3.3.1.1.2 Increasing port congestion and demand for operational efficiency

- 3.3.1.1.3 Advancements in AI, ML, and real-time monitoring technologies

- 3.3.1.1.4 Stringent maritime safety and environmental regulations

- 3.3.1.1.5 Investments in port infrastructure modernization

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1.1 High installation and maintenance costs

- 3.3.2.1.2 Limited interoperability between legacy and modern systems

- 3.3.1 Growth

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By System Type, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Vessel traffic services (VTS)

- 5.3 Port management systems (PMS)

- 5.4 Automatic identification system (AIS)

- 5.5 Radar-based systems

Chapter 6 Market Estimates and Forecast, By Component, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Hardware

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Marine authorities

- 7.3 Ports and harbours

- 7.4 Commercial vessel operators

- 7.5 Naval forces

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Elcome International LLC

- 9.2 Frequentis

- 9.3 Furuno

- 9.4 Hensoldt

- 9.5 Indra Sistemas

- 9.6 Japan Radio Co. Ltd.

- 9.7 Kongsberg Gruppen

- 9.8 Leonardo S.p.A.

- 9.9 Marlink AS

- 9.10 Northrop Grumman Corporation

- 9.11 Saab

- 9.12 ST Engineering

- 9.13 Terma

- 9.14 Thales Group

- 9.15 Wartsilä

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日