|

市場調査レポート

商品コード

1750497

使い捨て手術器具の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Disposable Surgical Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 使い捨て手術器具の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月15日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

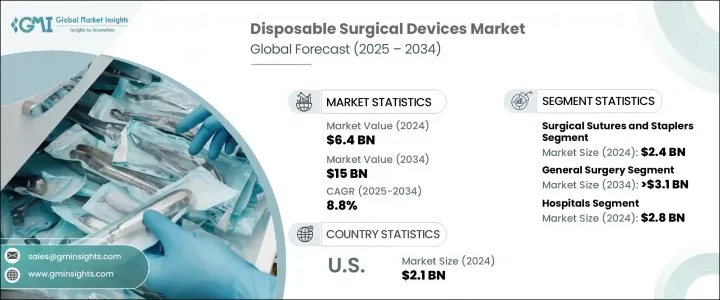

世界の使い捨て手術器具市場は、2024年には64億米ドルと評価され、手術件数の増加、感染防止対策の強化、低侵襲手術に対する世界の嗜好の高まりなどを背景に、CAGR 8.8%で成長し、2034年には150億米ドルに達すると予測されています。

使い捨て器具は、その効率性、使いやすさ、無菌状態を維持する能力から支持を集めています。先進経済諸国および新興経済諸国のヘルスケアシステムが業務の合理化と二次汚染のリスク軽減に取り組む中、使い捨て手術器具は最優先事項となりつつあります。自動化と人間工学的に高度なツールへのシフトは、特に高スループットの医療現場での採用をさらに後押ししています。

パンデミックの後、ヘルスケアプロバイダーはより厳格な感染管理方針を遵守しています。このため、特に選択的手術や緊急手術の件数が増加するにつれて、使い捨て手術ソリューションへの移行が加速しています。これらの器具は、衛生面で明確な利点を提供し、滅菌ステップを省き、手術室でのターンアラウンドタイムを短縮します。使い捨てを想定して設計されたこれらの器具は、スピードと患者の安全性の両方が要求される手術環境において、不可欠なものとなっています。基本的なツールから高度なステープラーやトロッカーまで、ディスポーザブルは手技の一貫性を向上させながら無菌状態を確保します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 64億米ドル |

| 予測金額 | 150億米ドル |

| CAGR | 8.8% |

製品タイプ別では、手術用縫合糸とステープラー部門が2024年に24億米ドルで市場をリードしました。縫合糸とステープラーは、従来の手技と低侵襲手技の両方で一貫して使用されているため、なくてはならないものとなっています。これらのツールは創傷管理に役立ち、適切な創傷閉鎖を保証し、感染を最小限に抑え、早期回復を助ける。人間工学に基づいたデザイン、結び目を必要としない有刺縫合糸、抗菌コーティングなどの技術革新により、安全性と効率性が大幅に向上し、トップクラスの実績を誇る製品カテゴリーとなっています。

一般外科分野は2034年までに31億米ドルに達し、CAGR 8.5%で成長すると予測されています。この分野では複数の手術が行われ、使い捨て手術器具の安定した需要に貢献しています。外来患者や入院患者の介入率の増加、慢性疾患や急性疾患の有病率の増加が、これらの器具の需要を押し上げています。医療機関は、特に大量生産環境において、安全遵守と患者ケアの合理化のために使い捨て手術器具に依存しています。

米国使い捨て手術器具2024年の市場規模は20億米ドルで、CAGR 7.7%で成長する見込みです。強力な規制の枠組み、洗練されたヘルスケアインフラ、有利な償還モデルのすべてが、使い捨て器具の急速な普及を支えています。また、米国に本社を置く大手医療機器メーカーが引き続き市場を牽引しています。

この市場の主要プレーヤーには、Smith+Nephew、CooperSurgical、Xenco Medical、BD、Johnson &Johnson、ZIMMER BIOMET、B Braun、Medtronic、Ambu、Surgical Innovations、Accutome、Boston Scientificなどがあります。足場を固めるため、各社は使いやすさ、安全性、性能を高めるための研究開発投資を通じて技術革新を優先しています。抗菌コーティングや結び目のない縫合糸など、スマートな機能を備えた製品ポートフォリオを拡充している企業も多いです。病院や手術センターとの戦略的提携も、供給契約の確保や市場浸透の深化に役立っています。さらにメーカー各社は、コスト効率を維持しながら増大する需要に対応するため、自動化と精密製造を活用し、世界市場での競争力を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界の手術件数の増加

- 急速な技術革新

- 使い捨て機器を優先する厳格な感染管理基準

- 低侵襲手術への関心の高まり

- 業界の潜在的リスク&課題

- 環境の持続可能性に関する懸念

- 費用と償還の障壁

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 外科用縫合糸とステープラー

- ハンドヘルド外科用機器

- 使い捨て内視鏡装置

- 電気外科用機器

第6章 市場推計・予測:手順別、2021-2034

- 主要動向

- 一般外科

- 形成外科および再建外科

- 整形外科

- 心臓血管外科

- 脳神経外科

- 産婦人科

- 創傷閉鎖

- その他の手順

第7章 市場推計・予測:最終用途別2021-2034

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Accutome

- Ambu

- B Braun

- BD

- Boston Scientific

- CooperSurgical

- Johnson &Johnson

- Medtronic

- Smith+Nephew

- Surgical Innovations

- Xenco Medical

- ZIMMER BIOMET

The Global Disposable Surgical Devices Market was valued at USD 6.4 billion in 2024 and is estimated to grow at a CAGR of 8.8% to reach USD 15 billion by 2034, driven by increasing surgical volumes, heightened infection control measures, and the rising global preference for minimally invasive procedures. Disposable instruments are gaining traction due to their efficiency, ease of use, and ability to maintain sterile conditions. As healthcare systems across developed and emerging economies look to streamline operations and reduce the risk of cross-contamination, single-use surgical tools are becoming a top priority. The shift toward automation and ergonomically advanced tools further supports adoption, particularly in high-throughput medical settings.

In the wake of the pandemic, healthcare providers adhere to stricter infection control policies. This has accelerated the move toward disposable surgical solutions, particularly as the number of elective and emergency procedures rebounds. These instruments offer clear benefits in hygiene, eliminate sterilization steps, and reduce turnaround times in operating rooms. Designed for single-use scenarios, they are proving vital in surgical environments that demand both speed and patient safety. From basic tools to advanced staplers and trocars, disposables ensure sterile conditions while improving procedural consistency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.4 Billion |

| Forecast Value | $15 Billion |

| CAGR | 8.8% |

Among product types, the surgical sutures and staplers segment led the market with USD 2.4 billion in 2024. Their consistent usage in both traditional and minimally invasive procedures makes them indispensable. These tools help in wound management, ensuring proper closure, minimizing infections, and aiding faster recovery. Innovations like ergonomic designs, barbed sutures requiring no knots, and antimicrobial coatings have significantly enhanced their safety and efficiency, making them the top-performing product category.

The general surgery segment is projected to reach USD 3.1 billion by 2034, growing at a CAGR of 8.5%. This category covers several procedures, contributing to consistent demand for disposable surgical tools. The increasing rate of outpatient and inpatient interventions, along with the growing prevalence of chronic and acute conditions, is boosting demand for these devices. Medical institutions rely on single-use surgical tools for safety compliance and streamlined patient care, especially in high-volume environments.

U.S. Disposable Surgical Devices Market accounted for USD 2 billion in 2024 and is expected to grow at a CAGR of 7.7%. A strong regulatory framework, sophisticated healthcare infrastructure, and favorable reimbursement models all support rapid adoption of disposable instruments. Additionally, major medical device companies headquartered in the U.S. continue to drive market momentum.

Key players in this market include Smith+Nephew, CooperSurgical, Xenco Medical, BD, Johnson & Johnson, ZIMMER BIOMET, B Braun, Medtronic, Ambu, Surgical Innovations, Accutome, and Boston Scientific. To strengthen their foothold, companies prioritize innovation through R&D investments to enhance usability, safety, and performance. Many are expanding product portfolios with smart features such as antimicrobial coatings and knotless sutures. Strategic collaborations with hospitals and surgical centers are also helping secure supply contracts and deepen market penetration. Furthermore, manufacturers leverage automation and precision manufacturing to meet growing demand while maintaining cost-efficiency, enhancing their competitive edge across global markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global surgical volume

- 3.2.1.2 Rapid technological innovation

- 3.2.1.3 Stringent infection control standards favoring disposable devices

- 3.2.1.4 Rising preference for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental sustainability concerns

- 3.2.2.2 Cost and reimbursement barriers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical sutures and staplers

- 5.3 Handheld surgical devices

- 5.4 Disposable endoscopy devices

- 5.5 Electrosurgical devices

Chapter 6 Market Estimates and Forecast, By Procedure, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Plastic and reconstructive Surgery

- 6.4 Orthopedic surgery

- 6.5 Cardiovascular surgery

- 6.6 Neurosurgery

- 6.7 Obstetrics and gynecology

- 6.8 Wound closure

- 6.9 Other procedures

Chapter 7 Market Estimates and Forecast, By End Use 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accutome

- 9.2 Ambu

- 9.3 B Braun

- 9.4 BD

- 9.5 Boston Scientific

- 9.6 CooperSurgical

- 9.7 Johnson & Johnson

- 9.8 Medtronic

- 9.9 Smith+Nephew

- 9.10 Surgical Innovations

- 9.11 Xenco Medical

- 9.12 ZIMMER BIOMET