|

市場調査レポート

商品コード

1750496

自動車用シートの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automotive Seating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用シートの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月08日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

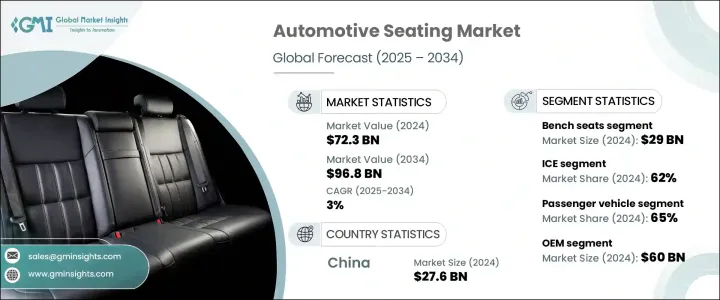

世界の自動車用シート市場は、2024年には723億米ドルとなり、自動車生産の増加、安全規制の強化、快適性と利便性に対する消費者の期待の高まりを背景に、CAGR3%で成長し、2034年までには968億米ドルに達すると予測されています。

自動車メーカーは、美観や乗員体験の向上だけでなく、進化する基準や購買者の選好を満たすスマート技術や持続可能な素材を統合するために、シーティングシステムを再考しています。

自動車用シート業界における顕著な変化は、人間工学と健康に配慮したデザインを優先する傾向が強まっていることです。自動車メーカーは、カスタマイズ可能なランバーサポート、体圧感知システム、姿勢矯正メカニズム、スマートシート内モニタリングソリューションなどの先進シート技術への投資を強化しています。これらの機能は、運転の快適性を高めるだけでなく、長時間の移動でも疲労を軽減し、背骨のアライメントを強化することで、長期的な健康をサポートするように設計されています。軽量複合材料は、構造強度と車両重量の軽減のバランスをとるためにますます使用されるようになっており、燃費とエネルギー効率の向上に貢献しています。インテリジェントで人間工学に基づいたシーティングシステムへの注目は、自動車のインテリアをよりユーザー中心の環境へと変化させ、メーカーが進化する消費者の期待に応えられるよう支援しています。中級車であってもプレミアムな体験を求める需要が高まる中、シーティングはブランドの差別化と購入者の意思決定を決定する要素となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 723億米ドル |

| 予測金額 | 968億米ドル |

| CAGR | 3% |

内燃機関車(ICE)セグメントは2024年に62%のシェアを占め、世界の自動車ラインアップに広く存在するため、引き続き支配的です。しかし、電気自動車(EV)セグメントは勢いを増しており、予測期間を通じて約4%のCAGRで成長すると予測されます。ICEモデルはその多様性とアクセシビリティで依然として人気がありますが、EVメーカーは技術に精通し、快適さを追求する消費者を引き付けるために、ランバー調整、ベンチレーション、マッサージ機能などの高度なシート機能を取り入れています。

2024年には、ベンチシートセグメントは290億米ドルを創出すると予想されます。ベンチシートの人気は、SUV、バン、多目的車など、乗員スペースの最大化が不可欠な車種での実用性に起因します。これらの構成は、座席定員を増やし、多目的なレイアウトを可能にするため、ファミリー向けとフリート向けの両方の車両セグメントに適しています。合理的な構造と手頃な価格により、ベンチシートは新興国市場でも成熟市場でも信頼できる選択肢であり続けています。

中国の自動車用シート市場は、2024年に276億米ドルとなり、自動車製造のエコシステム、ハイテク内装機能への選好の高まり、カスタマイズ性、接続性、高級感を優先するシーティングシステムへの新たな需要が原動力となっています。電気自動車や高級モデルが普及するにつれて、ベンチレーション付きシート、電子調整機能、メモリー機能といった機能が標準的な期待になりつつあります。中国の自動車メーカーは、急速な技術革新と現地生産の強化でこれに対応し、この地域のシーティング業界における中国の優位性をさらに強めています。

この市場を形成している主要企業、GRAMMER、RECARO Holding、Toyota Boshoku、Lear、MG Seating Systems、Adient、Magna International、Brose Sitech、Faurecia、Fisher and Companyなどです。競争力を維持するため、主要自動車用シートメーカーは、持続可能で人間工学に基づいた素材への研究開発投資、OEMとの協業、地域的な生産拡大などの戦略的な動きに注力しています。また、デジタル技術やAIを活用したシーティングシステムを統合することで、乗員体験を向上させ、ブランドアイデンティティを強化し、トップ自動車メーカーとの長期契約を確保している企業も多いです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 材料提供者

- 部品供給業者

- 製造業者

- 販売代理店

- OEM

- テクノロジーインテグレーター

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 貿易への影響

- 価格設定と製品戦略

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- スマートシート技術

- 車両システムとの統合

- 軽量化技術

- 快適性向上技術

- 新興技術

- AIと機械学習のアプリケーション

- シーティングシステムへのIoT統合

- 生体認証センシングとモニタリング

- 先端材料科学

- 現在の技術動向

- 特許分析

- 主なニュースと取り組み

- 消費者の選好と行動

- 快適さの期待

- 座席の好みに対する人口統計学的影響

- 座席の快適さに関する消費者の認識

- 価格動向

- シート

- 地域

- コスト内訳分析

- 規制情勢

- 影響要因

- 促進要因

- スマートでコネクテッドな座席技術の統合

- 軽量で持続可能な素材の進歩

- 電気自動車・自動運転車の内装再構成の増加

- センサーとエアバッグの統合による強化された安全機能

- 業界の潜在的リスク・課題

- ポリウレタンフォーム・複合材料のリサイクルの複雑さ

- 高度なシート機構の開発コストが高め

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:シート別、2021年~2034年

- 主要動向

- 折りたたみシート

- バケットシート

- ベンチシート

- 分割シート

- その他

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 標準

- 電動

- 換気機能付き

- 空調設備付き

- マッサージ機能付き

- その他

第7章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 本革

- 合成皮革

- ファブリック

- サステナブル

- リサイクル

- バイオベース

- 植物由来

第8章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第9章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- フレーム

- フォームパッド

- シートアジャスター

- ヘッドレスト

- その他

第10章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- 内燃機関(ICE)

- 電気自動車(EV)

- ハイブリッド車

第11章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- オリジナル機器メーカー(OEM)

- アフターマーケット

第12章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第13章 企業プロファイル

- Adient

- Brose Sitech

- Camaco-Amvian

- Dura Automotive Systems

- Faurecia

- Fisher and Company

- Freedman Seating

- GRAMMER

- Guelph Manufacturing

- Lear

- Magna International

- MG Seating Systems

- NHK Spring

- RECARO

- TACHI-S

- TM Systems

- Toyota Boshoku

- True Assistive Tech

- TS Tech

- Woodbridge

The Global Automotive Seating Market was valued at USD 72.3 billion in 2024 and is estimated to grow at a CAGR of 3% to reach USD 96.8 billion by 2034, fueled by increasing automobile production, tightening safety regulations, and rising consumer expectations for comfort and convenience. Automakers are rethinking seating systems not only to enhance aesthetics and passenger experience but to integrate smart technologies and sustainable materials that meet evolving standards and buyer preferences.

A noticeable shift in the automotive seating industry is the growing prioritization of ergonomics and health-conscious design. Automakers are ramping up investments in advanced seat technologies such as customizable lumbar support, pressure-sensing systems, posture correction mechanisms, and smart in-seat monitoring solutions. These features are designed not only to elevate driving comfort but also to support long-term health by reducing fatigue and enhancing spinal alignment during extended travel. Lightweight composite materials are increasingly used to balance structural strength with reduced vehicle weight, contributing to greater fuel and energy efficiency. This focus on intelligent, ergonomic seating systems transforms vehicle interiors into more user-centric environments, helping manufacturers meet evolving consumer expectations. As demand rises for premium experiences even in mid-range vehicles, seating has become a defining element of brand distinction and buyer decision-making.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $72.3 Billion |

| Forecast Value | $96.8 Billion |

| CAGR | 3% |

The internal combustion engine (ICE) vehicles segment held a 62% share in 2024, continuing to dominate due to their extensive presence across global automotive lineups. However, the electric vehicle (EV) segment is gaining momentum, projected to grow at approximately 4% CAGR through the forecast period. While ICE models remain popular for their variety and accessibility, EV manufacturers incorporate sophisticated seat functionalities, like lumbar adjustments, ventilation, and massage features, to attract tech-savvy, comfort-driven consumers.

In 2024, the bench seats segment will generate USD 29 billion. Their popularity stems from their practicality in SUVs, vans, and multipurpose vehicles, where maximizing passenger space is essential. These configurations allow for increased seating capacity and versatile layouts, making them well-suited for both family and fleet-oriented vehicle segments. Their streamlined construction and affordability continue to make bench seats a reliable choice in both developing and mature markets.

China Automotive Seating Market generated USD 27.6 billion in 2024, driven by the vehicle manufacturing ecosystem, a rising preference for high-tech interior features, and the new demand for seating systems prioritizing customization, connectivity, and premium feel. As electric vehicles and luxury models gain traction, features like ventilated seating, electronic adjustability, and memory functions are becoming standard expectations. China's automakers are responding with rapid innovation and enhanced local production, further reinforcing the country's dominance in the regional seating industry.

Key players shaping this market include GRAMMER, RECARO Holding, Toyota Boshoku, Lear, MG Seating Systems, Adient, Magna International, Brose Sitech, Faurecia, and Fisher and Company. To maintain a competitive edge, leading automotive seating manufacturers focus on strategic moves such as R&D investments in sustainable and ergonomic materials, collaborations with OEMs, and regional manufacturing expansion. Many integrate digital technology and AI-enabled seating systems to elevate passenger experience, strengthen brand identity, and secure long-term contracts with top automakers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Distributors

- 3.1.1.5 OEMs

- 3.1.1.6 Technology integrators

- 3.1.1.7 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.1 Impact on trade

- 3.3 Pricing and product strategies

- 3.4 Technology & innovation landscape

- 3.4.1 Current technological trends

- 3.4.1.1 Smart seating technologies

- 3.4.1.2 Integration with vehicle systems

- 3.4.1.3 Weight reduction technologies

- 3.4.1.4 Comfort enhancement technologies

- 3.4.2 Emerging Technologies

- 3.4.2.1 AI and Machine Learning Applications

- 3.4.2.2 IoT integration in seating systems

- 3.4.2.3 Biometric sensing and monitoring

- 3.4.2.4 Advanced material sciences

- 3.4.1 Current technological trends

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Consumer preferences and behavior

- 3.7.1 Comfort expectations

- 3.7.2 Demographic influences on seating preferences

- 3.7.3 Consumer perception of seating comfort

- 3.8 Price trend

- 3.8.1 Seat

- 3.8.2 Region

- 3.9 Cost breakdown analysis

- 3.10 Regulatory landscape

- 3.11 Impacting forces

- 3.11.1 Growth drivers

- 3.11.1.1 Integration of smart and connected seating technologies

- 3.11.1.2 Advancements in lightweight and sustainable materials

- 3.11.1.3 Growth in electric and autonomous vehicle interior reconfigurations

- 3.11.1.4 Enhanced safety features with sensor and airbag integrations

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 Complexity in recycling polyurethane foams and composites

- 3.11.2.2 High development costs for advanced seat mechanisms

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Seat, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Folding seat

- 5.3 Bucket seat

- 5.4 Bench seat

- 5.5 Split seat

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Standard

- 6.3 Powered

- 6.4 Ventilated

- 6.5 Climate-Controlled

- 6.6 Massage

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Genuine leather

- 7.3 Synthetic leather

- 7.4 Fabric

- 7.5 Sustainable

- 7.5.1 Recycled

- 7.5.2 Bio-based

- 7.5.3 Plant-derived

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Passenger vehicles

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUVs

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicles (LCVs)

- 8.3.2 Medium commercial vehicles (MCV)

- 8.3.3 Heavy commercial vehicles (HCVs)

Chapter 9 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Frames

- 9.3 Foam padding

- 9.4 Seat adjuster

- 9.5 Headrests

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Internal combustion engine (ICE)

- 10.3 Electric vehicles (EVs)

- 10.4 Hybrid vehicles

Chapter 11 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 Original equipment manufacturers (OEMs)

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 12.1 Key Trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Southeast Asia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 UAE

- 12.6.2 Saudi Arabia

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Adient

- 13.2 Brose Sitech

- 13.3 Camaco-Amvian

- 13.4 Dura Automotive Systems

- 13.5 Faurecia

- 13.6 Fisher and Company

- 13.7 Freedman Seating

- 13.8 GRAMMER

- 13.9 Guelph Manufacturing

- 13.10 Lear

- 13.11 Magna International

- 13.12 MG Seating Systems

- 13.13 NHK Spring

- 13.14 RECARO

- 13.15 TACHI-S

- 13.16 TM Systems

- 13.17 Toyota Boshoku

- 13.18 True Assistive Tech

- 13.19 TS Tech

- 13.20 Woodbridge