|

市場調査レポート

商品コード

1750489

炭素繊維注入ポリマーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Carbon Fiber-Infused Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 炭素繊維注入ポリマーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月14日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

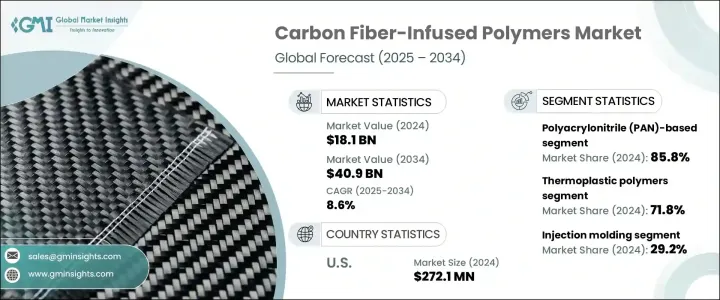

炭素繊維注入ポリマーの世界市場規模は、2024年に181億米ドルとなり、自動車、航空宇宙、防衛、再生可能エネルギー分野など様々な産業における需要の増加に牽引され、CAGR8.6%で成長し、2034年までには409億米ドルに達すると予測されています。

高強度対重量比、耐食性、熱安定性といった炭素繊維注入ポリマーのユニークな特性は、軽量で耐久性のある材料を必要とする用途に理想的です。自動車産業では、これらの材料は燃費の向上と排出ガスの削減に貢献し、厳しい環境規制に対応しています。

同様に、航空宇宙・防衛産業においても、これらの複合材を採用することで性能が向上し、運用コストが削減されます。再生可能エネルギー産業、特に風力発電分野では、タービンブレードの製造に炭素繊維複合材を組み込むことで利益を得続けています。これらの材料は、運転効率を高めながら風力エネルギーを捕捉する、より軽量で耐久性のあるブレードを可能にします。その高い強度対重量比は、より長いブレードの設計をサポートし、構造的完全性を損なうことなく、より大きなエネルギー出力につながります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 181億米ドル |

| 予測金額 | 409億米ドル |

| CAGR | 8.6% |

炭素繊維注入ポリマー市場において、ポリマータイプ別にセグメント化すると、熱可塑性ポリマーと熱硬化性ポリマーが注目されます。熱可塑性ポリマーの2024年のシェアは71.8%で、リサイクル性、加工時間の短さ、繰り返しの加熱と再成形に耐える能力が支持されています。これらの特徴は、持続可能性とコスト効率がますます重要になっている自動車や航空宇宙製造の大量生産用途に魅力的です。

射出成形分野は、精密で耐久性のある部品を大規模に供給できることから、2024年には29.2%のシェアを占めました。特に自動車分野では、軽量でありながら堅牢な構造部品の生産が可能で、自動車の性能と燃費の向上に貢献するため、このプロセスの恩恵を受けています。射出成形の複雑な形状への適応性と熱可塑性複合材料との互換性は、市場の関連性をさらに高めています。

米国の炭素繊維注入ポリマーの2024年の市場シェアは85%で、イノベーションと先端製造業への米国の戦略的投資が牽引しています。官民の資金援助により、複合材料製造の最適化に焦点を当てた専用の研究センターやテストベッドの設立が促進されています。こうした努力は、炭素繊維のコストを下げ、特に防衛、モビリティ、クリーンエネルギーなどの主要分野で商業利用できるようにその性能を向上させることを目的としています。

世界の炭素繊維注入ポリマー市場で事業を展開している主な企業には、Toray Industries Inc.、Teijin Limited、Hexcel Corporation、SGL Carbon、Solvay S.A.などがあります。これらの企業は技術革新の最前線に立ち、さまざまな産業の高まる需要に応えるため、先端材料や製造プロセスの開発に注力しています。市場での地位を強化するため、炭素繊維注入ポリマー業界の企業はいくつかの戦略的イニシアチブを採用しています。これには、材料特性の革新と改善のための研究開発への投資、市場開拓のための合弁事業やパートナーシップの確立、需要の増加に対応するための製造能力の強化などが含まれます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 原材料サプライヤー

- 製造業者

- 販売代理店

- 最終用途

- 利益率分析

- COVID-19によるバリューチェーンの混乱

- トランプ政権の関税の影響-構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

注:上記の貿易統計は主要国についてのみ提供されます

- 利益率分析

- 主なニュースと取り組み

- テクノロジーの情勢

- 伝統的な製造技術

- 高度な製造技術

- 新興技術

- 特許分析

- 規制情勢

- 市場力学

- 市場促進要因

- 自動車産業と航空宇宙産業における軽量素材の需要増加

- 燃費と排出ガス削減への関心の高まり

- スポーツやレジャーのアプリケーションでの採用増加

- 再生可能エネルギー部門の拡大

- 製造プロセスにおける技術の進歩

- 業界の潜在的リスク・課題

- 高い生産コスト

- 複雑な製造プロセス

- リサイクルと寿命の課題

- サプライチェーンの脆弱性

- 市場促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 市場シェア分析

- 競合ダッシュボード

- 戦略的取り組み

- 合併と買収

- 合弁事業

- 製品の発売

- 拡張計画

- 研究開発投資

- 競合ベンチマーキング

- ベンダー採用マトリックス

- 競合ポジショニングマトリックス

第5章 市場推計・予測:ポリマータイプ別、2021年~2034年

- 主要動向

- 熱可塑性ポリマー

- ポリアミド(PA)

- ポリプロピレン(PP)

- ポリエーテルエーテルケトン(PEEK)

- ポリフェニレンサルファイド(PPS)

- ポリエーテルイミド(PEI)

- その他

- 熱硬化性ポリマー

- エポキシ

- ポリエステル

- ビニルエステル

- ポリウレタン

- その他

第6章 市場推計・予測:カーボンファイバータイプ別、2021年~2034年

- 主要動向

- ポリアクリロニトリル(PAN)ベース

- 標準弾性係数

- 中間弾性率

- 高弾性率

- ピッチベース

- レーヨンベース

- リサイクル炭素繊維

第7章 市場推計・予測:製造工程別、2021年~2034年

- 主要動向

- 射出成形

- 圧縮成形

- 樹脂トランスファー成形

- プルトルージョン

- フィラメントワインディング

- 積層造形

- その他

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 航空宇宙・防衛

- 航空機部品

- 宇宙用途

- 防衛装備

- 自動車

- 構造部品

- 内装部品

- パワートレイン部品

- 電気自動車の用途

- 風力エネルギー

- ブレード

- ナセル

- その他のコンポーネント

- スポーツ・レジャー

- 自転車

- テニスラケット

- ゴルフクラブ

- その他

- 建設

- 補強材

- 構造部品

- その他

- 海洋

- 船体構造

- デッキコンポーネント

- その他

- 医学

- 義肢

- 画像機器

- その他

- 産業機器

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Carbon Fiber Composite Design

- Composite Horizons LLC

- Cytec Industries Inc.

- DowAksa

- Formosa Plastics Corporation

- Hexcel Corporation

- Hyosung Advanced Materials

- Kureha Corporation

- Mitsubishi Chemical Holdings Corporation

- Nippon Carbon Co.、Ltd.

- Plasan Carbon Composites

- SABIC

- SGL Carbon

- Sigmatex

- Solvay S.A.

- Teijin Limited

- Toho Tenax Co.、Ltd.

- Toray Industries、Inc.

- Zhongfu Shenying Carbon Fiber Co.、Ltd.

- Zoltek Companies、Inc.

The Global Carbon Fiber-Infused Polymers Market was valued at USD 18.1 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 40.9 billion by 2034, driven by the increasing demand across various industries, including automotive, aerospace, defense, and renewable energy sectors. The unique properties of carbon fiber-infused polymers-such as high strength-to-weight ratios, corrosion resistance, and thermal stability-make them ideal for applications requiring lightweight and durable materials. In the automotive industry, these materials contribute to fuel efficiency and reduced emissions, aligning with stringent environmental regulations.

Similarly, in aerospace and defense, adopting these composites enhances performance and reduces operational costs. The renewable energy industry, especially the wind power segment, continues to gain from integrating carbon fiber composites into turbine blade production. These materials allow lighter, more durable blades that capture wind energy while enhancing operational efficiency. Their high strength-to-weight ratio supports the design of longer blades, which leads to greater energy output without compromising structural integrity-an essential factor for large-scale wind installations both onshore and offshore.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.1 Billion |

| Forecast Value | $40.9 Billion |

| CAGR | 8.6% |

Within the carbon fiber-infused polymers market, segmentation by polymer type highlights thermoplastic and thermoset variants. The thermoplastic polymers segment held 71.8% share in 2024, favored for their recyclability, fast processing times, and ability to withstand repeated heating and reshaping. These features make them attractive for high-volume applications in automotive and aerospace manufacturing, where sustainability and cost-efficiency are becoming increasingly important.

The injection molding segment held a 29.2% share in 2024 due to its ability to deliver precise, durable parts at scale. The automotive sector, in particular, benefits from this process, as it enables the production of lightweight yet robust structural parts that contribute to improved vehicle performance and fuel efficiency. Injection molding's adaptability to complex geometries and compatibility with thermoplastic composites further amplify its market relevance.

United States Carbon Fiber-Infused Polymers Market held 85% share in 2024, driven by the nation's strategic investment in innovation and advanced manufacturing. Public and private sector funding has facilitated the establishment of dedicated research centers and test beds focused on optimizing composite material production. These efforts aim to lower the cost of carbon fiber and improve its performance for commercial use, particularly in key sectors like defense, mobility, and clean energy.

Key companies operating in the Global Carbon Fiber-Infused Polymers Market include Toray Industries Inc., Teijin Limited, Hexcel Corporation, SGL Carbon, and Solvay S.A. These companies are at the forefront of innovation, focusing on developing advanced materials and manufacturing processes to meet the growing demands of various industries. To strengthen their market position, companies in the carbon fiber-infused polymers industry are adopting several strategic initiatives. These include investing in research and development to innovate and improve material properties, establishing joint ventures and partnerships to expand market reach, and enhancing manufacturing capabilities to meet increasing demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research methodology

- 1.1.1 Initial data exploration

- 1.1.2 Primary research methodology

- 1.1.3 Secondary research methodology

- 1.1.4 Market size estimation approach

- 1.1.5 Data triangulation techniques

- 1.1.6 Research assumptions

- 1.2 Market definition and scope

- 1.2.1 Base year and forecast period

- 1.2.2 Market segmentation

- 1.2.3 Regional scope

- 1.2.4 Currency conversion rates

- 1.3 Information procurement

- 1.3.1 Purchased database

- 1.3.2 GMI's internal database

- 1.3.3 Secondary sources

- 1.3.4 Primary research

- 1.4 Information analysis

- 1.4.1 Data analysis models

- 1.4.2 Market breakdown and data triangulation

Chapter 2 Executive Summary

- 2.1 Carbon fiber-infused polymers industry 3600 synopsis, 2021-2034

- 2.1.1 Business trends

- 2.1.2 Regional trends

- 2.1.3 Polymer type trends

- 2.1.4 Carbon fiber type trends

- 2.1.5 Manufacturing process trends

- 2.1.6 End use industry trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Manufacturers

- 3.1.3 Distributors

- 3.1.4 End use

- 3.1.5 Profit margin analysis

- 3.1.6 Value chain disruptions due to COVID-19

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.5.1 Technology landscape

- 3.5.2 Traditional manufacturing technologies

- 3.5.3 Advanced manufacturing technologies

- 3.5.4 Emerging technologies

- 3.5.5 Patent analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Market dynamics

- 3.7.1 Market drivers

- 3.7.1.1 Increasing demand for lightweight materials in the automotive and aerospace industries

- 3.7.1.2 Growing focus on fuel efficiency and emission reduction

- 3.7.1.3 Rising adoption in sports and leisure applications

- 3.7.1.4 Expanding the renewable energy sector

- 3.7.1.5 Technological advancements in manufacturing processes

- 3.7.2 Industry pitfalls and challenges

- 3.7.2.1 High production costs

- 3.7.2.2 Complex manufacturing processes

- 3.7.2.3 Recycling and end-of-life challenges

- 3.7.2.4 Supply chain vulnerabilities

- 3.7.1 Market drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.9.1 Supplier power

- 3.9.2 Buyer power

- 3.9.3 Threat of new entrants

- 3.9.4 Threat of substitutes

- 3.9.5 Industry rivalry

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis, 2024

- 4.2 Competitive dashboard

- 4.3 Strategic initiatives

- 4.3.1 Mergers & acquisitions

- 4.3.2 Joint ventures

- 4.3.3 Product launches

- 4.3.4 Expansion plans

- 4.3.5 R&D investments

- 4.4 Competitive benchmarking

- 4.5 Vendor adoption matrix

- 4.6 Competitive positioning matrix

Chapter 5 Market Estimates and Forecast, By Polymer Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Thermoplastic polymers

- 5.2.1 Polyamide (PA)

- 5.2.2 Polypropylene (PP)

- 5.2.3 Polyether ether ketone (PEEK)

- 5.2.4 Polyphenylene sulfide (PPS)

- 5.2.5 Polyetherimide (PEI)

- 5.2.6 Others

- 5.3 Thermoset polymers

- 5.3.1 Epoxy

- 5.3.2 Polyester

- 5.3.3 Vinyl ester

- 5.3.4 Polyurethane

- 5.3.5 Others

Chapter 6 Market Estimates and Forecast, By Carbon Fiber Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Polyacrylonitrile (PAN)-based

- 6.2.1 Standard modulus

- 6.2.2 Intermediate modulus

- 6.2.3 High modulus

- 6.3 Pitch-based

- 6.4 Rayon-based

- 6.5 Recycled carbon fiber

Chapter 7 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Injection molding

- 7.3 Compression molding

- 7.4 Resin transfer molding

- 7.5 Pultrusion

- 7.6 Filament winding

- 7.7 Additive manufacturing

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.2.1 Aircraft components

- 8.2.2 Space applications

- 8.2.3 Defense equipment

- 8.3 Automotive

- 8.3.1 Structural components

- 8.3.2 Interior components

- 8.3.3 Powertrain components

- 8.3.4 Electric vehicle applications

- 8.4 Wind energy

- 8.4.1 Blades

- 8.4.2 Nacelles

- 8.4.3 Other components

- 8.5 Sports & leisure

- 8.5.1 Bicycles

- 8.5.2 Tennis rackets

- 8.5.3 Golf clubs

- 8.5.4 Others

- 8.6 Construction

- 8.6.1 Reinforcement materials

- 8.6.2 Structural components

- 8.6.3 Others

- 8.7 Marine

- 8.7.1 Hull structures

- 8.7.2 Deck components

- 8.7.3 Others

- 8.8 Medical

- 8.8.1 Prosthetics

- 8.8.2 Imaging equipment

- 8.8.3 Others

- 8.9 Industrial equipment

- 8.10 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Carbon Fiber Composite Design

- 10.2 Composite Horizons LLC

- 10.3 Cytec Industries Inc.

- 10.4 DowAksa

- 10.5 Formosa Plastics Corporation

- 10.6 Hexcel Corporation

- 10.7 Hyosung Advanced Materials

- 10.8 Kureha Corporation

- 10.9 Mitsubishi Chemical Holdings Corporation

- 10.10 Nippon Carbon Co., Ltd.

- 10.11 Plasan Carbon Composites

- 10.12 SABIC

- 10.13 SGL Carbon

- 10.14 Sigmatex

- 10.15 Solvay S.A.

- 10.16 Teijin Limited

- 10.17 Toho Tenax Co., Ltd.

- 10.18 Toray Industries, Inc.

- 10.19 Zhongfu Shenying Carbon Fiber Co., Ltd.

- 10.20 Zoltek Companies, Inc.