高温超電導体の市場機会と成長促進要因、産業動向分析、2025~2034年予測

High-Temperature Superconductors (HTS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750485

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

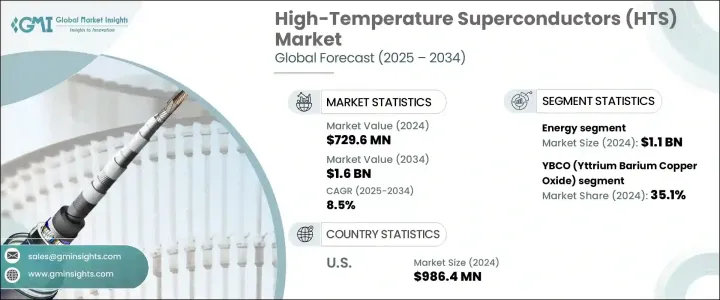

世界の高温超電導体市場は2024年に7億2,960万米ドルと評価され、CAGR 8.5%で成長し、2034年には16億米ドルに達すると推定されています。

高温超電導体(しばしばHTSと呼ばれる)は、従来の超電導体よりもかなり高い温度で抵抗なしに電気を通すことができる先端材料です。絶対零度に近い温度で動作する従来型とは異なり、HTS材料は77ケルビン以上で機能するため、液体窒素冷却システムと互換性があり、コスト効率が高く、管理も容易です。この重要な特性により、HTSは、次世代電力システム、輸送、高度医療画像技術など、高いエネルギー効率を必要とする用途において有利な選択肢となります。

各分野における電気性能の向上に対する需要の高まりは、HTS材料の採用を促進する上で極めて重要な役割を果たしています。これらの超電導体は、特に送電網のアップグレードやエネルギー損失の最小化のために、近代的なエネルギー・インフラに統合されつつあります。世界中の政府及び電力会社は、老朽化したシステムの改修に重点を置いており、HTSベースのソリューションは、その効率と、より低い運転損失でより高い電力負荷を処理する能力から、不可欠なものと考えられています。このような取り組みは、持続可能なエネルギーへの世界の後押しと、電力消費の増加と分散型エネルギー資源に対応できる弾力的な電力インフラの必要性によって、さらに後押しされています。故障電流の制限、電力品質の向上、グリッド性能の最適化における超電導デバイスの使用は、この勢いに拍車をかけています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億2,960万米ドル |

| 予測金額 | 16億米ドル |

| CAGR | 8.5% |

様々なHTSタイプの中で、イットリウムバリウム銅酸化物(YBCO)が引き続き市場を独占しています。このセグメントは2024年の世界シェアの35.1%を占め、評価額は11億米ドルに達しました。YBCOは90ケルビン近くで安定した性能を発揮するため、優れた電流密度と強磁場に耐える能力を備えながら、冷却ロジスティクスを簡素化することができます。これらの特徴により、高出力かつ磁石中心のアプリケーションでの使用に適しています。旧来の超電導体と比較して、YBCOはより優れた熱管理と動作効率を実現するため、商業的および実験的な配備において幅広く使用されています。

第一世代HTS線材セグメントは、2034年までに7億6,180万米ドルに達し、CAGR 11.6%という目覚しい成長を遂げると予測されています。BSCCO化合物をベースとする第一世代線材は、パウダー・イン・チューブ法のような成熟した製造技術のおかげで商業的利用が可能になりました。このプロセスでは、超電導粉末を銀ベースのチューブに入れ、線材に成形します。これらの線材は液体窒素と互換性のある温度で効率的に機能するため、冷却にかかる総コストを削減し、エネルギーシステムや科学研究におけるパイロット・スケールや少量生産のアプリケーションにとって魅力的な選択肢となります。

エネルギーは依然としてHTS材料の最大の用途分野であり、2024年の評価額は11億米ドルで、2025年から2034年にかけてCAGR 12%で成長し、市場全体の35.4%を占めると予想されています。世界の電力インフラの変革は、電気をロスなく伝送できる材料に大きく依存しています。HTSに対応した送電線とコンポーネントは、従来の銅やアルミのケーブルに比べて長距離で大電流を伝送することができ、特に都市人口が密集し、新設のための物理的なスペースが限られている地域ではその能力を発揮します。これらの配備はエネルギー散逸を減らし、システムの信頼性を高めるため、現代の配電網にとって不可欠なものとなっています。

米国では、2024年に9億8,640万米ドルの評価額に達し、2034年までのCAGRは12.4%で拡大すると見られています。電力網を近代化し、防衛とクリーンエネルギーのための新技術を探求する同国の取り組みの中心となっているのは、連邦政府機関、民間団体、研究機関の間の資金調達と協力の強化です。システムの脆弱性に対処しつつ、より高い性能を発揮できる超電導パワーデバイスに焦点を当てたプロジェクトに投資が注がれています。これらの投資は、国家インフラの強化とエネルギー自立の促進を目的とした広範な戦略の一環です。

高温超電導体の市場情勢は、既存企業とニッチなイノベーターが混在しており、競争は中程度です。この分野に携わる企業は、競争力を維持するために、垂直統合された事業、高度な研究能力、協力的なパートナーシップを有していることが多いです。大企業は豊富な製造経験とインフラを持ち込む一方、中小企業は専門技術や材料開発を通じて貢献しています。ヘルスケア、エネルギー、輸送などの分野における需要の変化に対応するためには、産学官の戦略的提携とともにイノベーションを継続することが不可欠です。この継続的な協力関係は、高温超電導の進歩の次の段階を形作るものと期待されます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーン構造

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)注:上記の貿易統計は主要国についてのみ提供されます

- 主要輸出国、2021-2024

- 主要輸入国、2021-2024

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- エネルギー効率の高いソリューションに対する需要の増加

- 極低温技術の進歩

- ヘルスケア分野で成長するアプリケーション

- 核融合エネルギー調査への投資増加

- 業界の潜在的リスク&課題

- 高い製造コスト

- 大規模生産における技術的課題

- 冷却システムの複雑さ

- 促進要因

- 市場機会

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 市場シェア分析

- メーカー別世界市場シェア

- メーカー別地域市場シェア

- 競合ベンチマーキング

- 製品ポートフォリオの比較

- 技術力の比較

- 研究開発投資の比較

- 製造能力の比較

- 戦略的取り組みと開発

- 合併と買収

- パートナーシップとコラボレーション

- 製品の発売とイノベーション

- 拡張計画

- 競合ポジショニングマトリックス

- 戦略的ダッシュボード

第5章 市場推計・予測:材質別、2021-2034

- 主要動向

- YBCO(イットリウムバリウム銅酸化物)

- BSCCO(ビスマスストロンチウムカルシウム銅酸化物)

- REBCO(希土類バリウム銅酸化物)

- MgB2(二ホウ化マグネシウム)

- 鉄系超伝導

- ニッケル酸塩

- その他

第6章 市場推計・予測:製品形態別、2021-2034

- 主要動向

- 第一世代(1G)HTSワイヤ

- 第2世代(2G)HTSテープ

- HTSバルク材料

- HTS薄膜

- その他

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- エネルギー

- 電源ケーブル

- トランスフォーマー

- モーターと発電機

- 故障電流制限装置

- エネルギー貯蔵システム

- ヘルスケア

- MRIシステム

- NMR装置

- その他

- 交通機関

- 磁気浮上式鉄道

- 電気航空機

- 船舶の推進

- 電子工学と通信

- 電子レンジフィルター

- RFおよびマイクロ波デバイス

- 量子コンピューティングコンポーネント

- 調査および科学機器

- 高磁場磁石

- 粒子加速器

- 核融合炉

- 産業用途

- 誘導加熱装置

- 磁気分離

- その他

- その他

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- American Superconductor

- Bruker

- Fujikura

- High Temperature Superconductors

- IBM

- Japan Superconductor Technology

- Nexans

- SuperOx

- SuperPower

- Theva

目次

The Global High-Temperature Superconductors Market was valued at USD 729.6 million in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 1.6 billion by 2034. High-temperature superconductors, often referred to as HTS, are advanced materials capable of conducting electricity without resistance at temperatures significantly higher than traditional superconductors. Unlike conventional counterparts that operate near absolute zero, HTS materials function at or above 77 Kelvin, making them compatible with liquid nitrogen cooling systems, which are both cost-effective and easier to manage. This key attribute positions HTS as a favorable option in applications requiring high energy efficiency, including next-generation power systems, transportation, and advanced medical imaging technologies.

Growing demand for enhanced electrical performance across sectors is playing a pivotal role in driving the adoption of HTS materials. These superconductors are being integrated into modern energy infrastructures, particularly for upgrading transmission grids and minimizing energy losses. Governments and utilities worldwide are placing emphasis on revamping aging systems, and HTS-based solutions are being considered essential due to their efficiency and ability to handle higher power loads with lower operational losses. These initiatives are further encouraged by the global push for sustainable energy and the need for resilient power infrastructures that can accommodate rising electricity consumption and distributed energy resources. The use of superconducting devices in limiting fault currents, enhancing power quality, and optimizing grid performance is adding to the momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $729.6 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 8.5% |

Among various HTS types, Yttrium Barium Copper Oxide (YBCO) continues to dominate the market. This segment accounted for 35.1% of the global share in 2024 and reached a valuation of USD 1.1 billion. YBCO remains preferred due to its stable performance at nearly 90 Kelvin, which simplifies cooling logistics while providing superior current density and the ability to withstand strong magnetic fields. These features make it suitable for use in high-power and magnet-centric applications. Compared to older superconductors, YBCO delivers better thermal management and operational efficiency, which has led to its wide-scale use in commercial and experimental deployments.

The first-generation HTS wires segment is projected to hit USD 761.8 million by 2034, growing at an impressive CAGR of 11.6%. First-generation wires, based on BSCCO compounds, have achieved commercial availability thanks to mature production techniques like the Powder-In-Tube method. This process involves placing superconducting powder into silver-based tubes and forming them into wires, resulting in conductors that are both effective and easier to produce at scale. These wires function efficiently at temperatures compatible with liquid nitrogen, reducing the overall cost of cooling and making them an attractive option for pilot-scale and low-volume applications in energy systems and scientific research.

Energy remains the largest application segment for HTS materials, with a valuation of USD 1.1 billion in 2024 and expected to grow at a CAGR of 12% from 2025 to 2034, capturing 35.4% of the total market. The transformation of global power infrastructure relies heavily on materials that can transmit electricity without losses. HTS-enabled power lines and components are capable of transmitting higher currents over long distances compared to conventional copper or aluminum cables, particularly in areas with dense urban populations and limited physical space for new installations. Their deployment reduces energy dissipation and enhances system reliability, making them essential for modern electricity distribution networks.

In the United States, the market reached a valuation of USD 986.4 million in 2024 and is set to expand at a CAGR of 12.4% through 2034. Increased funding and collaboration between federal agencies, private entities, and research institutions are central to the country's efforts to modernize its power grid and explore new technologies for defense and clean energy. Investments are being channeled into projects focusing on superconducting power devices that can deliver greater performance while addressing system vulnerabilities. These investments are part of broader strategies aimed at reinforcing national infrastructure and advancing energy independence.

The market landscape for high-temperature superconductors is moderately competitive, with a mix of established corporations and niche innovators. Companies involved in this field often possess vertically integrated operations, advanced research capabilities, and collaborative partnerships to remain competitive. Larger enterprises bring in extensive manufacturing experience and infrastructure, while smaller players contribute through specialized technologies and materials development. Continued innovation, along with strategic alliances between industry, academia, and government, is vital for keeping pace with evolving demands in sectors such as healthcare, energy, and transportation. This ongoing collaboration is expected to shape the next phase of high-temperature superconductivity advancements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain structure

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries, 2021-2024 (kilo tons)

- 3.3.2 Major importing countries, 2021-2024 (kilo tons)

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing demand for energy-efficient solutions

- 3.8.1.2 Advancements in cryogenic technologies

- 3.8.1.3 Growing applications in healthcare sector

- 3.8.1.4 Rising investments in fusion energy research

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High manufacturing costs

- 3.8.2.2 Technical challenges in large-scale production

- 3.8.2.3 Cooling system complexities

- 3.8.1 Growth drivers

- 3.9 Market opportunities

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Market share analysis

- 4.2.1 Global market share by manufacturer

- 4.2.2 Regional market share by manufacturer

- 4.3 Competitive benchmarking

- 4.3.1 Product portfolio comparison

- 4.3.2 Technological capabilities comparison

- 4.3.3 R&D investment comparison

- 4.3.4 Manufacturing capacity comparison

- 4.4 Strategic initiatives & developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 Product launches & innovations

- 4.4.4 Expansion plans

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

Chapter 5 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 YBCO (Yttrium Barium Copper Oxide)

- 5.3 BSCCO (Bismuth Strontium Calcium Copper Oxide)

- 5.4 REBCO (Rare Earth Barium Copper Oxide)

- 5.5 MgB2 (Magnesium Diboride)

- 5.6 Iron-based superconduct

- 5.7 Nickelates

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Product Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 First-generation (1G) HTS wires

- 6.3 Second-generation (2G) HTS tapes

- 6.4 HTS bulk materials

- 6.5 HTS thin films

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Energy

- 7.2.1 Power cables

- 7.2.2 Transformers

- 7.2.3 Motors & generators

- 7.2.4 Fault current limiters

- 7.2.5 Energy storage systems

- 7.3 Healthcare

- 7.3.1 MRI systems

- 7.3.2 NMR equipment

- 7.3.3 Others

- 7.4 Transportation

- 7.4.1 Maglev trains

- 7.4.2 Electric aircraft

- 7.4.3 Ship propulsion

- 7.5 Electronics & communication

- 7.5.1 Microwave filters

- 7.5.2 RF & microwave devices

- 7.5.3 Quantum computing components

- 7.6 Research & scientific instruments

- 7.6.1 High-field magnets

- 7.6.2 Particle accelerators

- 7.6.3 Fusion reactors

- 7.7 Industrial applications

- 7.7.1 Induction heaters

- 7.7.2 Magnetic separation

- 7.7.3 Others

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 American Superconductor

- 9.2 Bruker

- 9.3 Fujikura

- 9.4 High Temperature Superconductors

- 9.5 IBM

- 9.6 Japan Superconductor Technology

- 9.7 Nexans

- 9.8 SuperOx

- 9.9 SuperPower

- 9.10 Theva

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日