|

市場調査レポート

商品コード

1750476

画像誘導治療システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Image-guided Therapy Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 画像誘導治療システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月07日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

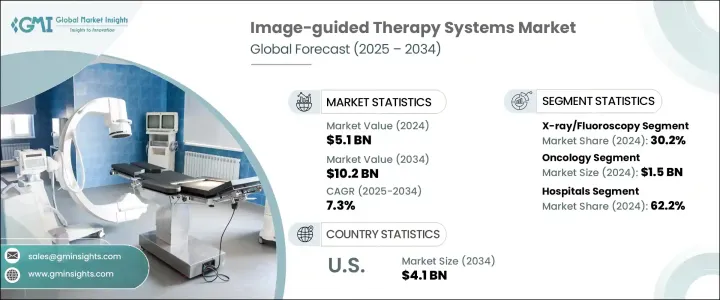

世界の画像誘導治療システム市場は、2024年には51億米ドルと評価され、神経疾患、心血管疾患、がんを含む慢性疾患の有病率の上昇に牽引され、CAGR 7.3%で成長し、2034年には102億米ドルに達すると推定されています。

精密医療への信頼の高まりは、低侵襲手技の強力な推進と相まって、リアルタイムの画像ベースのガイダンスを可能にするシステムの需要を大幅に押し上げています。AI対応画像、ロボット支援ナビゲーション、3D視覚化などの医療進歩は、精度の向上、手術期間の短縮、臨床転帰の改善によって外科手術に変革をもたらしつつあります。

痛みの軽減、回復時間の短縮、入院期間の短縮といった利点から、患者も医療提供者も、より低侵襲なアプローチを好むようになっています。人工知能と機械学習は、診断を合理化し、画像解釈を改善し、手技ナビゲーションを自動化することで、画像誘導治療の有用性を最適化します。世界のヘルスケアシステムが患者中心の価値観に基づく医療を目指す中、画像誘導ソリューションは手術の計画と実行に不可欠なものとなりつつあります。ハイブリッド手術室の導入は加速しており、高度な画像診断ツールを手術室に直接組み込んで術中にシームレスに使用することで、意思決定を強化し、合併症のリスクを低減しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 51億米ドル |

| 予測金額 | 102億米ドル |

| CAGR | 7.3% |

製品カテゴリー別では、X線透視誘導システムが2024年のシェア30.2%を占め、循環器科、整形外科、インターベンショナル・ラジオロジーなどの分野での強い需要を反映しています。最小限の外傷でリアルタイムの画像ガイド下インターベンションを実行できることが、病院や外来で広く採用されている主な要因です。これらのシステムで画像処理機能が向上したことで、医師は複雑な手技をより高い精度とリスク低減で実施できるようになり、これが同分野の継続的な成長に寄与しています。

腫瘍学セグメントは2024年に15億米ドルを生み出しました。がん患者が世界的に増加し続ける中、臨床医は放射線照射、生検、切除など、より的を絞った治療を行うために画像誘導システムを利用するようになっています。MRI、PET、CT、超音波などの画像ツールがリアルタイムで統合されたことで、術中のガイダンスが大幅に強化され、腫瘍の位置の特定、切開創の縮小、周辺組織を温存した個別化治療が可能になりました。これにより、ブラキセラピー、SBRT、RFアブレーションなどの手技において、これらのシステムの使用が加速しています。

米国画像誘導治療システム2024年の市場規模は21億米ドルで、2034年までに倍増すると予測されています。同国ではアウトカム重視のヘルスケアを推進しており、臨床効率とコスト効率の両方を実現する技術の導入が進んでいます。慢性疾患に直面する高齢者人口の増加も、対応可能な市場を拡大しています。病院や外来センターでは、画像誘導治療システムを統合して手技の精度を高め、患者の回復時間を最小限に抑えています。価値ベースの償還モデルへのシフトは、合併症の少ない、より良いアウトカムをサポートする機器への投資をプロバイダーに促しています。

存在感を高めるため、ストライカー、メドトロニック、シーメンス・ヘルティニアーズ、キヤノンメディカルシステムズ、インテュイティブ・サージカルなどの大手企業は、AIを搭載したソフトウェア、クラウド統合画像プラットフォーム、高度な手術ロボットに投資しています。これらの企業は、病院と戦略的パートナーシップを結び、専門性の高い新興企業を買収し、次世代製品パイプラインをサポートするために研究開発活動を拡大しています。これらの企業は、手技のアウトカムを向上させ、ヘルスケアプロバイダーのブランドロイヤリティを拡大するために、市場に特化したデバイスのカスタマイズや術後分析ツールに注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の有病率の上昇

- 画像およびナビゲーション技術の進歩

- 低侵襲手術の需要増加

- 政府の支援政策と民間投資

- 業界の潜在的リスク&課題

- 高い資本コストと維持費

- 新興市場へのアクセスが限られている

- 促進要因

- 成長可能性分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項トランプ政権の関税

- 貿易への影響

- テクノロジーの情勢

- 将来の市場動向

- 規制情勢

- ギャップ分析

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- X線透視検査

- 超音波

- コンピュータ断層撮影

- 磁気共鳴画像法

- 陽電子放出断層撮影

- その他の製品タイプ

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 心臓手術

- 脳神経外科

- 整形外科

- 消化器内科

- 泌尿器科

- 腫瘍学

- 耳鼻咽喉科手術

- その他の用途

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

- 調査・学術機関

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Accuray

- Analogic

- Brainlab

- Canon Medical Systems

- Fujifilm Holdings

- GE HealthCare

- Intuitive Surgical

- Karl Storz

- Koninklijke Philips

- Medtronic

- Olympus

- Siemens Healthineers

- Smith &Nephew

- Stryker

- Zimmer Biomet

The Global Image-guided Therapy Systems Market was valued at USD 5.1 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 10.2 billion by 2034, driven by the rising prevalence of chronic illnesses, including neurological disorders, cardiovascular conditions, and cancer. Increasing reliance on precision medicine, coupled with a strong push for minimally invasive procedures, has significantly boosted demand for systems that allow real-time, image-based guidance. Medical advancements such as AI-enabled imaging, robotic-assisted navigation, and 3D visualization are transforming surgery by enhancing precision, shortening procedure durations, and improving clinical outcomes.

Patients and providers alike are increasingly favoring less invasive approaches due to benefits like reduced pain, quicker recovery times, and shorter hospital stays. Artificial intelligence and machine learning optimize the utility of image-guided therapy by streamlining diagnostics, improving imaging interpretation, and automating procedural navigation. As global healthcare systems move toward patient-centered and value-based care, image-guided solutions are becoming an essential part of surgical planning and execution. The adoption of hybrid operating rooms is accelerating and integrating advanced imaging tools directly into the surgical suite for seamless intraoperative use, which enhances decision-making and lowers the risk of complications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $10.2 Billion |

| CAGR | 7.3% |

Among product categories, X-ray and fluoroscopy-guided systems accounted for a 30.2% share in 2024, reflecting strong demand in fields such as cardiology, orthopedics, and interventional radiology. The ability to perform real-time image-guided interventions with minimal trauma is a key factor behind their widespread adoption across hospitals and ambulatory settings. Improved imaging functionality in these systems enables physicians to carry out complex procedures with higher accuracy and reduced risk, which is contributing to ongoing segment growth.

The oncology segment generated USD 1.5 billion in 2024. As cancer cases continue to rise globally, clinicians are turning to image-guided systems for more targeted therapies, including radiation, biopsies, and ablations. Real-time integration of imaging tools like MRI, PET, CT, and ultrasound has greatly enhanced intra-procedural guidance, allowing for better tumor localization, smaller incisions, and personalized treatments that spare surrounding tissue. This has accelerated the use of these systems in procedures such as brachytherapy, SBRT, and RF ablation.

U.S. Image-guided Therapy Systems Market was valued at USD 2.1 billion in 2024 and is projected to double by 2034. The country's push for outcome-driven healthcare is encouraging the adoption of technologies that deliver both clinical and cost efficiency. A growing elderly population facing chronic illnesses is also expanding the addressable market. Hospitals and outpatient centers integrate image-guided therapy systems to improve procedural precision and minimize patient recovery time. The shift toward value-based reimbursement models incentivizes providers to invest in equipment that supports better outcomes with fewer complications.

To strengthen their presence, leading firms like Stryker, Medtronic, Siemens Healthineers, Canon Medical Systems, and Intuitive Surgical are investing in AI-powered software, cloud-integrated imaging platforms, and advanced surgical robotics. These companies are forming strategic partnerships with hospitals, acquiring specialized startups, and expanding R&D efforts to support next-generation product pipelines. They focus on market-specific device customization and post-operative analytics tools to enhance procedural outcomes and extend brand loyalty among healthcare providers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic diseases

- 3.2.1.2 Advancements in imaging and navigation technologies

- 3.2.1.3 Growing demand for minimally invasive surgeries

- 3.2.1.4 Supportive government policies and private investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and maintenance costs

- 3.2.2.2 Limited access in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerationsTrump administration tariffs

- 3.4.1 Impact on trade

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.8 Gap analysis

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 X-ray/fluoroscopy

- 5.3 Ultrasound

- 5.4 Computed tomography

- 5.5 Magnetic resonance imaging

- 5.6 Positron emission tomography

- 5.7 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiac surgery

- 6.3 Neurosurgery

- 6.4 Orthopedic surgery

- 6.5 Gastroenterology

- 6.6 Urology

- 6.7 Oncology

- 6.8 ENT surgery

- 6.9 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Research and academic institutions

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accuray

- 9.2 Analogic

- 9.3 Brainlab

- 9.4 Canon Medical Systems

- 9.5 Fujifilm Holdings

- 9.6 GE HealthCare

- 9.7 Intuitive Surgical

- 9.8 Karl Storz

- 9.9 Koninklijke Philips

- 9.10 Medtronic

- 9.11 Olympus

- 9.12 Siemens Healthineers

- 9.13 Smith & Nephew

- 9.14 Stryker

- 9.15 Zimmer Biomet