|

市場調査レポート

商品コード

1750471

HVACバルブの市場機会と促進要因、業界動向分析、2025年~2034年予測HVAC Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| HVACバルブの市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年05月15日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

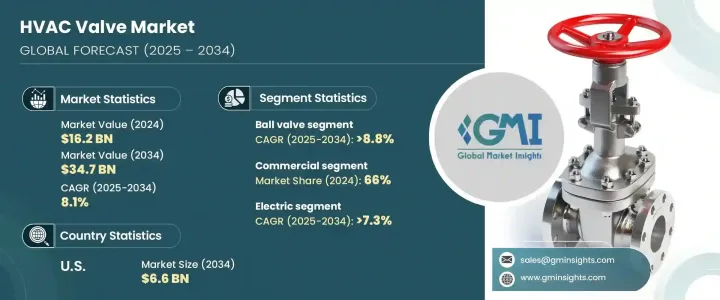

世界のHVACバルブ市場は、2024年に162億米ドルと評価され、世界の建設活動の急増に牽引され、住宅、商業、産業部門全体で暖房、換気、空調(HVAC)システムの需要増加につながり、CAGR 8.1%で成長し、2034年には347億米ドルに達すると推定されています。

バルブは、流体の流れ、圧力、温度を調整し、最適な性能とエネルギー効率を確保することによって、これらのシステムで重要な役割を果たしています。

エネルギー効率の高いスマートビルディングへの動向が、HVACバルブ市場を後押ししています。新しい建築物には、リアルタイムの監視と制御のためのセンサー、接続性、分析機能を備えたインテリジェントバルブを備えた高度なHVACシステムが組み込まれています。これらのスマートバルブにより、施設管理者はエネルギー消費の最適化、故障の早期発見、予知保全の実行が可能になり、運用コストの削減と機器寿命の延長が実現します。モノのインターネット(IoT)技術をHVACシステムに統合することで、自動化されたインテリジェントバルブソリューションの需要が加速しています。これらのスマートバルブは、リアルタイムのモニタリング、リモートアクセス、高度な制御機能を提供し、施設管理者がエネルギー使用を最適化し、システムの応答性を向上させることを可能にします。商業ビルや産業ビルがますますスマートビルディングの枠組みを採用するにつれ、ビル管理システム(BMS)とシームレスに通信するバルブのニーズが高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 162億米ドル |

| 予測金額 | 347億米ドル |

| CAGR | 8.1% |

2024年のHVACバルブ市場では、ボールバルブが4.3%と大きなシェアを占めています。ボールバルブの人気は、そのシンプルな構造、タイトなシャットオフ動作、HVACシステムのエアフローと流体フロー管理に適していることに起因しています。ボールバルブは、低トルク動作、密閉性、高耐久性により、新規設置や改造プロジェクトで広く使用されており、冷暖房アプリケーションの効率化と無菌化に貢献しています。さらに、ボールバルブは自動化技術をサポートし、スマートHVACシステムに適合します。

2024年のHVACバルブ市場は、商業部門が66%のシェアを占めました。オフィス、ショッピングモール、病院、ホテル、データセンター、学校などの商業ビルでは、流体や空気の流れを正確に調整するために複雑なHVACシステムが必要です。これらの建物におけるスマートでエネルギー効率の高いHVACシステムの採用は、政府基準への準拠、コスト削減、LEEDのようなグリーン認証の取得の必要性によって推進されています。この動向は、精密な制御とビル管理システムとの統合を提供する高度なHVACバルブの需要を促進しています。

米国HVACバルブ市場は2024年に67%のシェアを占め、エネルギースタープログラムやカナダのエネルギー効率規制などの厳しいエネルギー効率規制や持続可能性イニシアティブによって、2034年までに66億米ドルを生み出すと予測されています。これらの規制は、エネルギーを節約し、環境基準に準拠するために、インテリジェントなIoTベースのバルブを含む効率的なHVACシステムの採用を奨励しています。同地域におけるスマートビルディングとオートメーションへの注目は、ビル管理システム(BMS)対応のHVACバルブの需要をさらに後押ししています。さらに、古い建物における既存のHVACシステムの改修は、高度なバルブソリューションの需要増加に寄与しています。

世界のHVACバルブ業界の主要企業は、Honeywell、Johnson Controls、Schneider Electric、Siemens、Belimo、Danfoss、Pentair、AVK、Flowserve、Mueller Industries、Samson、Taco、Bray、Nexus、IDCなどです。これらの企業は、市場での存在感を高めるため、製品の革新、戦略的パートナーシップ、M&Aに注力しています。スマートな機能と強化された性能を備えた先進的なHVACバルブの開発は、主要メーカーの重点分野です。さらに、持続可能なHVACシステムに対する需要の高まりに対応するため、企業は環境に優しくエネルギー効率の高いソリューションを開発するための研究開発に投資しています。

市場での存在感を高めるため、HVACバルブ業界の企業はいくつかの重要な戦略を採用しています。これらには、顧客の進化するニーズに対応するための新しいバルブ設計や機能の導入など、技術革新や技術進歩による製品ポートフォリオの拡大が含まれます。IoTやオートメーションなどのスマート技術の統合は、市場の重要な動向であり、メーカーがリアルタイムの監視・制御機能を備えた高度なソリューションを提供することを可能にしています。技術プロバイダー、HVACシステムメーカー、流通業者との戦略的提携や協力関係により、企業は製品提供を強化し、より幅広い顧客層にリーチすることができます。さらに、合併や買収は、市場統合や新しい市場や技術へのアクセスを得るための一般的な戦略です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 製造業者

- 原材料サプライヤー

- 流通チャネル

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 成長する建設業界

- 都市化とスマートシティの取り組み

- 気候変動と異常気象

- 業界の潜在的リスク&課題

- 初期費用が高め

- 新興市場での認知度が低い

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 産業構造と集中

- 競争強度評価

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 製品の位置付け

- 価格性能比ポジショニング

- 地理的プレゼンス

- イノベーション能力

- 戦略的ダッシュボード

- 競合ベンチマーキング

- 製造能力

- 製品ポートフォリオの強さ

- 流通ネットワーク

- 研究開発投資

- 戦略的取り組みの評価

- 主要プレーヤーのSWOT分析

- 将来の競争見通し

第5章 市場推計・予測:バルブタイプ別、2021-2034

- 主要動向

- ボールバルブ

- グローブバルブ

- バタフライバルブ

- チェックバルブ

- ゲートバルブ

- 圧力逃し弁

- 制御弁

- 電磁弁

- その他

第6章 市場推計・予測:オペレーションタイプ別、2021-2034

- 主要動向

- マニュアル

- 空気圧

- 油圧式

- 電気

- スマート/コネクテッド

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 暖房システム

- 冷却システム

- 換気システム

- 地域冷房

- 冷凍

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 住宅用

- 商業用

- オフィスビル

- 小売り

- おもてなし

- ヘルスケア

- 教育機関

- その他

- 産業

- 石油・ガス

- 製造業

- 食品と飲料

- 医薬品

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- AVK

- Belimo

- Bray

- Danfoss

- Flowserve

- Honeywell

- IDC

- Johnson Controls

- Mueller Industries

- Nexus

- Pentair

- Samson

- Schneider Electric

- Siemens

The Global HVAC Valve Market was valued at USD 16.2 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 34.7 billion by 2034 driven by the surge in construction activities worldwide, leading to increased demand for heating, ventilation, and air conditioning (HVAC) systems across residential, commercial, and industrial sectors. Valves play a crucial role in these systems by regulating fluid flow, pressure, and temperature, ensuring optimal performance and energy efficiency.

The trend toward energy-efficient and smart buildings is propelling the HVAC valve market. New constructions incorporate advanced HVAC systems with intelligent valves featuring sensors, connectivity, and analytics for real-time monitoring and control. These smart valves enable facility managers to optimize energy consumption, detect faults early, and perform predictive maintenance, reducing operational costs and extending equipment lifespan. Integrating Internet of Things (IoT) technology into HVAC systems accelerates the demand for automated and intelligent valve solutions. These smart valves offer real-time monitoring, remote access, and advanced control capabilities, allowing facility managers to optimize energy usage and improve system responsiveness. As commercial and industrial buildings increasingly adopt smart building frameworks, the need for valves that seamlessly communicate with Building Management Systems (BMS) is rising.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.2 Billion |

| Forecast Value | $34.7 Billion |

| CAGR | 8.1% |

In 2024, ball valves held a significant share of the HVAC valve market, accounting for 4.3%. Their popularity is attributed to their simple structure, tight shut-off action, and suitability for airflow and fluid flow management in HVAC systems. Ball valves are widely used in new installations and retrofitting projects due to their low torque operation, close seal, and high durability, which contribute to the efficiency and asepsis of heating and cooling applications. Additionally, ball valves support automation technologies, making them compatible with smart HVAC systems.

The commercial sector dominated the HVAC valve market in 2024, representing a 66% share. Commercial buildings such as offices, shopping malls, hospitals, hotels, data centers, and schools require complex HVAC systems to regulate fluid and air flow accurately. The adoption of smart and energy-efficient HVAC systems in these buildings is driven by the need to comply with government standards, reduce costs, and achieve green certifications like LEED. This trend fuels the demand for advanced HVAC valves that offer precise control and integration with building management systems.

United States HVAC Valve Market held a 67% share in 2024 and is projected to generate USD 6.6 billion by 2034, driven by stringent energy efficiency regulations and sustainability initiatives, such as the Energy Star program and Canada's Energy Efficiency Regulations. These regulations are encouraging the adoption of efficient HVAC systems, including intelligent and IoT-based valves, to conserve energy and comply with environmental standards. The focus on smart buildings and automation in the region further supports the demand for Building Management System (BMS)-compatible HVAC valves. Additionally, the retrofitting of existing HVAC systems in older buildings is contributing to the increased demand for advanced valve solutions.

Key players in the Global HVAC Valve Industry include Honeywell, Johnson Controls, Schneider Electric, Siemens, Belimo, Danfoss, Pentair, AVK, Flowserve, Mueller Industries, Samson, Taco, Bray, Nexus, and IDC. These companies focus on product innovation, strategic partnerships, and mergers and acquisitions to strengthen their market presence. Developing advanced HVAC valves with smart features and enhanced performance is a key focus area for leading manufacturers. Additionally, companies are investing in research and development to develop eco-friendly and energy-efficient solutions to meet the growing demand for sustainable HVAC systems.

To strengthen their market presence, companies in the HVAC valve industry are adopting several key strategies. These include expanding their product portfolios through innovation and technological advancements, such as introducing new valve designs and features to cater to the evolving needs of customers. Integrating smart technologies, such as IoT and automation, is a significant trend in the market, enabling manufacturers to offer advanced solutions with real-time monitoring and control capabilities. Strategic partnerships and collaborations with technology providers, HVAC system manufacturers, and distributors enable companies to enhance their product offerings and reach a broader customer base. Additionally, mergers and acquisitions are common strategies for market consolidation and gaining access to new markets and technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Distribution channel

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact on forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing construction industry

- 3.8.1.2 Urbanization and smart city initiatives

- 3.8.1.3 Climate change and weather extremes

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial costs

- 3.8.2.2 Limited awareness in emerging markets

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Industry structure and concentration

- 4.2.1 Competitive intensity assessment

- 4.2.2 Company market share analysis

- 4.2.3 Competitive positioning matrix

- 4.3 Product positioning

- 4.3.1 Price-performance positioning

- 4.3.2 Geographic presence

- 4.3.3 Innovation capabilities

- 4.4 Strategic dashboard

- 4.5 Competitive benchmarking

- 4.5.1 Manufacturing capabilities

- 4.5.2 Product portfolio strength

- 4.5.3 Distribution network

- 4.5.4 R&D investments

- 4.6 Strategic initiatives assessment

- 4.7 SWOT analysis of key players

- 4.8 Future competitive outlook

Chapter 5 Market Estimates & Forecast, By Valve Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Ball valves

- 5.3 Globe valves

- 5.4 Butterfly valves

- 5.5 Check valves

- 5.6 Gate valves

- 5.7 Pressure relief valves

- 5.8 Control valves

- 5.9 Solenoid valves

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Operation Type, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Pneumatic

- 6.4 Hydraulic

- 6.5 Electric

- 6.6 Smart/connected

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Heating systems

- 7.3 Cooling systems

- 7.4 Ventilation systems

- 7.5 district cooling

- 7.6 Refrigeration

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Office buildings

- 8.3.2 Retail

- 8.3.3 hospitality

- 8.3.4 Healthcare

- 8.3.5 Educational institute

- 8.3.6 Others

- 8.4 Industrial

- 8.4.1 Oil and gas

- 8.4.2 Manufacturing

- 8.4.3 Food and beverage

- 8.4.4 Pharmaceuticals

- 8.4.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AVK

- 10.2 Belimo

- 10.3 Bray

- 10.4 Danfoss

- 10.5 Flowserve

- 10.6 Honeywell

- 10.7 IDC

- 10.8 Johnson Controls

- 10.9 Mueller Industries

- 10.10 Nexus

- 10.11 Pentair

- 10.12 Samson

- 10.13 Schneider Electric

- 10.14 Siemens