航空機用ワイヤー・ケーブルの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Aircraft Wire and Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750470

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

世界の航空機用ワイヤー・ケーブル市場は、2024年には18億米ドルと評価され、航空機の生産量の急増と、電動化および都市型エアモビリティプラットフォームの急速な進歩により、CAGR5.9%で成長し、2034年までには32億米ドルに達すると予測されています。

航空機が複雑なシステムや推進の電動化によって進化するにつれて、革新的な配線ソリューションの需要が急増し続けています。また、複数の利害関係者は、次世代航空機の高性能ケーブルへの依存度が高まるにつれて、軽量で熱的に安定した高電圧配線システムの役割が、商用および軍事用途の両方でさらに重要になると指摘しています。

企業幹部は、以前の貿易制限、特に輸入アルミニウムと鋼鉄への関税が航空宇宙バリューチェーンをいかに混乱させたかを振り返りました。このような政策変更によって原材料価格が上昇し、OEMや主要Tier-1サプライヤーの予算編成が複雑になりました。さらに、国際的な報復関税によって調達業務が混乱し、重要なケーブル材料の価格と調達が不安定になりました。世界に統合されたサプライチェーンを持つ企業は、調達の遅れとコスト上昇が製造スケジュールを圧迫し、最も深刻な後退に直面しました。エンジニアが指摘するように、今日の電気航空機やeVTOLプラットフォームでは、アビオニクス、バッテリー推進、熱制御などのシステム用に高度な配線が必要です。これらの用途では、重量を最小限に抑えながら過酷な条件にも耐えられるケーブルが必要です。アナリストは、先進的な航空機設計の動向により、航空宇宙企業は次世代航空機の目標に沿った堅牢でコンパクトなケーブルシステムの開発に多くの投資を行っていると強調しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 18億米ドル |

| 予測金額 | 32億米ドル |

| CAGR | 5.9% |

ワイヤ・ケーブル製品セグメントの航空機用ワイヤセグメントは、2024年に38.3%のシェアを占め、その理由は様々な航空機システム全体で電力、制御信号、データの伝送に不可欠な役割を担っているためです。業界のサプライヤーは、特に航空機プログラムが次世代電気アーキテクチャや自動化の拡大に移行するにつれて、耐熱性で軽量な配線ソリューションに対する需要が高まっていることを強調しています。また、電磁干渉や耐火性に関する規制圧力も設計パラメータを形成しており、耐空証明やフリート改修には高度なワイヤ構成が不可欠となっています。

固定翼航空機セグメントは、生産ラインの拡大と老朽化した航空機の継続的なアップグレードにより、2034年までに13億米ドルに達すると予想されています。航空エンジニアは、固定翼機は一般的に回転翼機や無人航空機よりも複雑な配線システムを必要とすると指摘しています。これらの航空機は通常、長距離運用と高度な安全機能をサポートする高密度なモジュール式ワイヤーハーネスを必要とします。

米国び航空機用ワイヤー・ケーブル市場は、民間航空宇宙および防衛セクターへの強力な資金供給に支えられ、2024年5億6,260万米ドルの規模となりました。業界関係者は、米国を拠点とするプログラムは過酷な条件下での信頼性と生存性を優先しているため、特殊なワイヤー材料やシールド技術の開発を促していると指摘します。米国は、より電動化された航空機プラットフォーム用に設計された高電圧および光ファイバーケーブルシステムの実験場であり、長期的な成長の可能性を示しています。

航空機用ワイヤー・ケーブルの世界市場で事業を展開する企業は、市場フットプリントを強化するために複数の戦略を採用しています。Ametek、Eaton、Aerospace Wire &Cable、Bergen Cable Technology、Amphenol、Collins Aerospaceなどの主な企業は、より軽量で熱的に安定したケーブルソリューションを開発するために研究開発投資を優先しています。多くの企業は、サプライチェーンの敏捷性を向上させ、需要の増大に対応するため、世界な製造能力を拡大しています。航空機のOEMやシステムインテグレーターとのコラボレーションも増加しており、進化する航空機設計に合わせた配線アーキテクチャが可能となっています。さらに、各社は製品ポートフォリオと競争力を強化する戦略的買収や認証取得に注力しています。こうした動きは、高度に技術的で規制主導の市場において、回復力と持続的成長を確保することを目的としています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 成長促進要因

- 航空機の生産と納入の増加

- 新興国における商業航空の拡大

- 軍用機の調達と改修の急増

- メンテナンス、修理、オーバーホール(MRO)部門の成長

- 都市航空モビリティと電気航空機プログラムへの投資増加

- 業界の潜在的リスク・課題

- 先進的な航空宇宙グレードの材料の高コスト

- 旧型航空機の改修における課題

- 成長促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 航空機用ワイヤー

- 航空機ケーブル

- 同軸ケーブル

- データケーブル

- 電源ケーブル

- 光ファイバーケーブル

- RFケーブル

- その他

- 航空機ハーネス

第6章 市場推計・予測:航空機タイプ別、2021年~2034年

- 主要動向

- 固定翼

- 回転翼

- 無人航空機

第7章 市場推計・予測:シールドタイプ別、2021年~2034年

- 主要動向

- シールドワイヤー・ケーブル

- シールドされていないワイヤー・ケーブル

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 飛行制御システム

- 照明システム

- データ転送

- 電力伝達

- 航空電子機器

- 着陸装置・ブレーキシステム

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Aerospace Wire &Cable

- Ametek

- Amphenol

- Bergen Cable Technology

- Collins Aerospace

- Eaton

- HUBER+SUHNER

- Lexco Cable

- Miracle Electronics Devices

- Molex

- Nexans

- PIC Wire &Cable

- Prysmian Group

- Radiall

- Sanghvi Aerospace

- TE Connectivity

- Tyler Madison

- WL Gore and Associates

目次

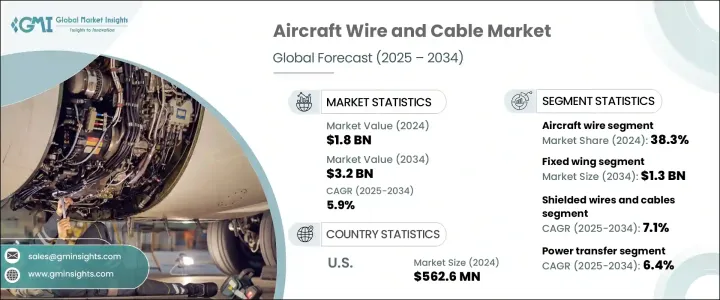

The Global Aircraft Wire and Cable Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 3.2 billion by 2034, driven by the surge in aircraft production volumes, paired with rapid advancements in electric and urban air mobility platforms. As aircraft evolve with complex systems and propulsion electrification, the demand for innovative wiring solutions continues to surge. Several stakeholders also pointed out that as next-generation aircraft become more reliant on high-performance cables, the role of lightweight, thermally stable, and high-voltage wiring systems becomes even more crucial in both commercial and military applications.

Company officials recalled how earlier trade restrictions, particularly the tariffs on imported aluminum and steel, disrupted the aerospace value chain. These policy changes elevated raw material prices, complicating budgeting for OEMs and major tier-1 suppliers. Additionally, international retaliatory tariffs disrupted sourcing operations, leading to instability in pricing and procurement of vital cabling materials. Firms with globally integrated supply chains faced the most severe setbacks, as sourcing delays and elevated costs strained manufacturing timelines. As noted by engineers, electrical aircraft and eVTOL platforms today demand sophisticated wiring for systems like avionics, battery propulsion, and thermal control. These applications require cables that can withstand extreme conditions while keeping weight minimal. Analysts emphasized that advanced aircraft design trends have driven aerospace firms to invest more in developing robust and compact cable systems that align with next-gen aviation goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 5.9% |

The aircraft wire segment in the wire and cable product segment held a 38.3% share in 2024, attributed to its essential role in transmitting power, control signals, and data throughout various aircraft systems. Industry suppliers emphasized that demand is growing for heat-resistant, lightweight wiring solutions, particularly as aircraft programs transition toward next-generation electric architectures and increased automation. Regulatory pressures around electromagnetic interference and fire resistance also shape design parameters, making advanced wire configurations vital for airworthiness certifications and fleet retrofits.

The fixed-wing aircraft segment is anticipated to reach USD 1.3 billion by 2034, driven by expanding production lines and continued upgrades to aging fleets. Aviation engineers pointed out that fixed-wing designs generally require more intricate cabling systems than rotary-wing or unmanned aerial vehicles, as they host a greater concentration of avionics, flight control, and cabin systems. These aircraft typically demand dense, modular wiring harnesses that support long-range operations and advanced safety features.

United States Aircraft Wire and Cable Market generated USD 562.6 million in 2024, underpinned by strong funding for the commercial aerospace and defense sectors. Industry insiders noted that U.S.-based programs prioritize reliability and survivability under harsh conditions, prompting the development of specialized wire materials and shielding technologies. The country remains a testing ground for high-voltage and fiber-optic cabling systems designed for more electric aircraft platforms, signaling long-term growth potential.

Companies operating in the Global Aircraft Wire and Cable Market are adopting multiple strategies to bolster their market footprint. Key players such as Ametek, Eaton, Aerospace Wire & Cable, Bergen Cable Technology, Amphenol, and Collins Aerospace have prioritized R&D investments to develop lighter, more thermally stable cable solutions. Many firms are expanding their global manufacturing capabilities to improve supply chain agility and meet growing demand. Collaborations with aircraft OEMs and system integrators are also rising, enabling tailored wiring architectures that align with evolving aircraft designs. In addition, companies are focusing on strategic acquisitions and certifications that enhance their product portfolios and competitive standing. These moves aim to ensure resilience and sustained growth in a highly technical and regulation-driven market.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising aircraft production and deliveries

- 3.3.1.2 Expansion of commercial aviation in emerging economies

- 3.3.1.3 Surge in military aircraft procurement and upgrades

- 3.3.1.4 Growth of the maintenance, repair, and overhaul (mro) sector

- 3.3.1.5 Rising investments in urban air mobility and electric aircraft programs

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost of advanced aerospace-grade materials

- 3.3.2.2 Challenges in retrofitting legacy aircraft

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 Pestel analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Aircraft wire

- 5.3 Aircraft cable

- 5.3.1 Coaxial cables

- 5.3.2 Data cables

- 5.3.3 Power cables

- 5.3.4 Fiber optic cables

- 5.3.5 RF cables

- 5.3.6 Others

- 5.4 Aircraft harness

Chapter 6 Market Estimates & Forecast, By Aircraft Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Fixed wing

- 6.3 Rotary wing

- 6.4 Unmanned aerial vehicles

Chapter 7 Market Estimates & Forecast, By Shielding Type, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Shielded wires and cables

- 7.3 Unshielded wires and cables

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Flight control systems

- 8.3 Lighting systems

- 8.4 Data transfer

- 8.5 Power transfer

- 8.6 Avionics

- 8.7 Landing gear & braking systems

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aerospace Wire & Cable

- 10.2 Ametek

- 10.3 Amphenol

- 10.4 Bergen Cable Technology

- 10.5 Collins Aerospace

- 10.6 Eaton

- 10.7 HUBER+SUHNER

- 10.8 Lexco Cable

- 10.9 Miracle Electronics Devices

- 10.10 Molex

- 10.11 Nexans

- 10.12 PIC Wire & Cable

- 10.13 Prysmian Group

- 10.14 Radiall

- 10.15 Sanghvi Aerospace

- 10.16 TE Connectivity

- 10.17 Tyler Madison

- 10.18 WL Gore and Associates

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日