|

市場調査レポート

商品コード

1750448

衛星フェーズドアレイアンテナの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Satellite Phased Array Antenna Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 衛星フェーズドアレイアンテナの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月02日

発行: Global Market Insights Inc.

ページ情報: 英文 162 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

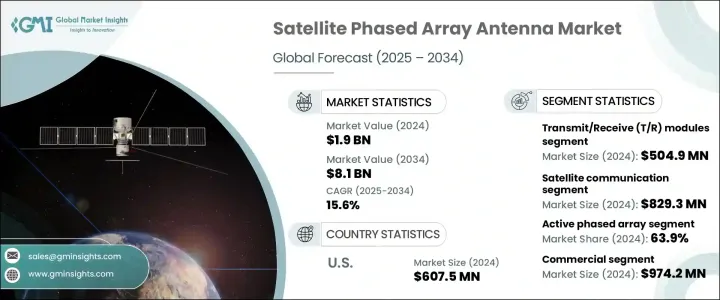

衛星フェーズドアレイアンテナの世界市場規模は、2024年に19億米ドルとなり、政府・民間部門からの投資の増加、5G技術の展開、モノのインターネット(IoT)デバイスの台頭、低軌道(LEO)衛星の利用拡大などを背景に、CAGR15.6%で成長し、2034年までには81億米ドルに達すると予測されています。

より多くの組織や政府が通信インフラの改善や宇宙探査に注力する中、信頼性の高い接続や監視のためには高性能なビームステアリングアンテナが不可欠となっています。

しかし、特にトランプ政権が中国からの輸入品に課した関税などの課題は、市場に顕著な影響を与えました。これらの関税は、中国から調達することが多い半導体やRFモジュールなどの組立部品の価格を引き上げ、米国を拠点とするメーカーの製造コストを引き上げました。このようなグローバルサプライチェーンの混乱により、企業は新たな貿易ソースを模索し、生産戦略を調整するようになり、市場に複雑さが加わりました。さらに、進行中の防衛近代化構想や、宇宙探査や衛星ベースのインフラへの政府投資の増加が、高度衛星通信システムの需要に大きく寄与しています。各国が軍事力の強化を優先する中、信頼性が高く高性能な衛星通信技術の必要性は、国家安全保障、情報収集、監視に不可欠となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 19億米ドル |

| 予測金額 | 81億米ドル |

| CAGR | 15.6% |

2024年、送受信(T/R)モジュールは5億490万米ドルの貢献をしました。これらのモジュールは、衛星通信システムに必要な高速、低遅延機能を確保する上で重要な役割を果たしています。小型化されたT/Rモジュールを組み込んだ、より小型でエネルギー効率の高いアンテナに対する需要の高まりは、軍事・商業の両分野で拡大しています。優れたシグナルインテグリティと熱管理を備えたこれらのアンテナは、高性能で電子的に操縦可能な衛星通信システムの汎用性を高めています。

市場はアレイのタイプによっても区分され、2024年にはアクティブフェーズドアレイが63.9%の市場シェアで優位を占めると予想されています。アクティブアレイは、ビームの敏捷性、信号利得、精度において大きな利点を提供します。これらのアンテナは、素子ごとに個別の送受信モジュールを持ち、ダイナミックビームフォーミング、冗長性、信号強度の向上を可能にします。これらの特長により、アクティブフェーズドアレイは、迅速な追跡と堅牢な接続性が不可欠なLEO衛星コンステレーション、防衛システム、モバイル通信プラットフォームなどの用途に最適です。

米国の衛星フェーズドアレイアンテナの市場は、衛星通信、防衛、宇宙開発への投資の増加が牽引し、2024年に6億750万米ドルの規模を生み出しました。LEO衛星コンステレーションや高度な軍事通信システムへの需要が、NASAや国防総省などの機関からの強力な支援を受けて、引き続き市場を牽引しています。

ViaSat、Boeing、Honeywell International、ALCAN Systemsなど、世界の衛星フェーズドアレイアンテナ市場に参入している企業は、その地位を確固たるものにするために重要な戦略を採用しています。これらの企業は、高性能衛星システムに対する需要の高まりに対応するため、特にビームステアリング技術の製品ラインナップの拡充に注力しています。また、政府機関や非公開会社とのコラボレーションも重要な戦略であり、宇宙探査や防衛プロジェクトのための資金を活用することを可能にしています。さらに、市場をリードする企業は、アンテナの効率と小型化を強化するための研究開発に多額の投資を行っており、より俊敏でスケーラブルなソリューションに対する需要が高まる中、競争力を維持できるようにしています。これらの戦略により、世界市場での継続的な優位性が確保されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 成長促進要因

- 世界な接続性に対する需要の急増

- 政府と民間部門の投資の増加

- 5G技術の展開とモノのインターネット(IoT)デバイスの普及

- 軍事・防衛における衛星フェーズドアレイアンテナの応用の増加

- アンテナ技術の進歩

- 業界の潜在的リスク・課題

- 衛星フェーズドアレイアンテナに関連する高い製造コスト

- ビームステアリングと制御の複雑さ

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- マイクロコントローラ/マイクロプロセッサ

- フィールドプログラマブルゲートアレイ(FPGA)

- パワーアンプ(PA)

- 低雑音増幅器(LNA)

- 位相シフター

- 送信/受信(T/R)モジュール

- その他

第6章 市場推計・予測:アレイタイプ別、2021年~2034年

- 主要動向

- アクティブフェーズドアレイ

- パッシブフェーズドアレイ

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 衛星通信

- レーダー・センシング

- ナビゲーション・トラッキング

- モバイル接続

- 地球観測

- 電子戦

- その他

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 商業用

- 防衛・セキュリティ

- 研究・学術機関

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Airbus

- Av-Comm Space &Defence

- ALCAN Systems

- Anokiwave

- AST &Science

- Boeing

- C-COM Satellite Systems

- Chengdu Ruidiwei

- Get SAT Ltd

- Honeywell International Inc.

- Iridium Communications Inc

- KEYCOM Corporation

- Requtech

- ThinKom Solutions、Inc.

- ViaSat

The Global Satellite Phased Array Antenna Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 15.6% to reach USD 8.1 billion by 2034, driven by increasing investments from both government and private sectors, the roll-out of 5G technology, the rise of Internet of Things (IoT) devices, and the expanding use of Low Earth Orbit (LEO) satellites. As more organizations and governments focus on improving communications infrastructure and space exploration, the need for high-performance, beam-steering antennas becomes critical for reliable connectivity and surveillance.

However, challenges such as tariffs imposed on Chinese imports, particularly by the Trump administration, had a notable impact on the market. These tariffs raised the production costs for U.S.-based manufacturers by increasing the price of assembly components such as semiconductors and RF modules, which are often sourced from China. This disruption in the global supply chain led companies to explore new trade sources and adjust production strategies, adding complexity to the market. Additionally, the ongoing defense modernization initiatives and increased government investments in space exploration and satellite-based infrastructure are significantly contributing to the demand for advanced satellite communication systems. As countries prioritize enhancing their military capabilities, the need for reliable, high-performance satellite communication technologies has become essential for national security, intelligence gathering, and surveillance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $8.1 Billion |

| CAGR | 15.6% |

In 2024, Transmit/Receive (T/R) modules contributed USD 504.9 million. These modules play a vital role in ensuring the high-speed, low-latency functionality required for satellite communication systems. The increasing demand for smaller, energy-efficient antennas that incorporate miniaturized T/R modules is expanding across both military and commercial sectors. These antennas, with superior signal integrity and thermal management, provide enhanced versatility for high-performance, electronically steerable satellite communication systems.

The market is also segmented by array type, with active phased arrays expected to dominate with a market share of 63.9% in 2024. Active arrays offer significant advantages in beam agility, signal gain, and precision. These antennas have individual transmit/receive modules for each element, enabling dynamic beamforming, redundancy, and improved signal strength. These features make active phased arrays ideal for applications in LEO satellite constellations, defense systems, and mobile communication platforms, where rapid tracking and robust connectivity are essential.

United States Satellite Phased Array Antenna Market generated USD 607.5 million in 2024, driven by increasing investments in satellite communication, defense, and space exploration. The demand for LEO satellite constellations and advanced military communication systems continues to drive the market forward, with strong support from agencies like NASA and the Department of Defense.

Companies in the Global Satellite Phased Array Antenna Market, including ViaSat, Boeing, Honeywell International, and ALCAN Systems, are adopting key strategies to solidify their positions. These companies are focusing on expanding their product offerings, particularly in beam-steering technology, to meet the growing demand for high-performance satellite systems. Collaboration with government organizations and private space companies has also been a critical strategy, enabling them to leverage funding for space exploration and defense projects. Additionally, market leaders are investing heavily in research and development to enhance antenna efficiency and miniaturization, ensuring that they remain competitive as the demand for more agile, scalable solutions rises. These strategies ensure their ongoing dominance in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.3.1 Supply-side impact (raw materials)

- 3.2.1.3.1.1 Price volatility in key materials

- 3.2.1.3.1.2 Supply chain restructuring

- 3.2.1.3.1.3 Production cost implications

- 3.2.1.3.2 Demand-side impact (selling price)

- 3.2.1.3.2.1 Price transmission to end markets

- 3.2.1.3.2.2 Market share dynamics

- 3.2.1.3.2.3 Consumer response patterns

- 3.2.1.3.1 Supply-side impact (raw materials)

- 3.2.1.4 Key companies impacted

- 3.2.1.5 Strategic industry responses

- 3.2.1.5.1 Supply chain reconfiguration

- 3.2.1.5.2 Pricing and product strategies

- 3.2.1.5.3 Policy engagement

- 3.2.1.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Surge in demand for global connectivity

- 3.7.1.2 Growth in government and private sector investments

- 3.7.1.3 Rollout of 5G technology and the proliferation of Internet of Things (IoT) devices

- 3.7.1.4 Increasing applications of satellite phased array antenna in military and defense

- 3.7.1.5 Rising advancements in antenna technology

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High manufacturing cost associated with the satellite phased array antenna

- 3.7.2.2 Complexity in beam steering and control

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Microcontrollers / microprocessors

- 5.3 Field programmable gate arrays (FPGAs)

- 5.4 Power amplifiers (PAs)

- 5.5 Low noise amplifiers (LNAs)

- 5.6 Phase shifters

- 5.7 Transmit/receive (T/R) modules

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Array Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Active phased array

- 6.3 Passive phased array

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Satellite communication

- 7.3 Radar & sensing

- 7.4 Navigation & tracking

- 7.5 Mobile connectivity

- 7.6 Earth observation

- 7.7 Electronic warfare

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Defense & security

- 8.4 Research & academic institutions

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airbus

- 10.2 Av-Comm Space & Defence

- 10.3 ALCAN Systems

- 10.4 Anokiwave

- 10.5 AST & Science

- 10.6 Boeing

- 10.7 C-COM Satellite Systems

- 10.8 Chengdu Ruidiwei

- 10.9 Get SAT Ltd

- 10.10 Honeywell International Inc.

- 10.11 Iridium Communications Inc

- 10.12 KEYCOM Corporation

- 10.13 Requtech

- 10.14 ThinKom Solutions, Inc.

- 10.15 ViaSat