|

市場調査レポート

商品コード

1750447

直接デジタル制御システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測Direct Digital Control System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 直接デジタル制御システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月13日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

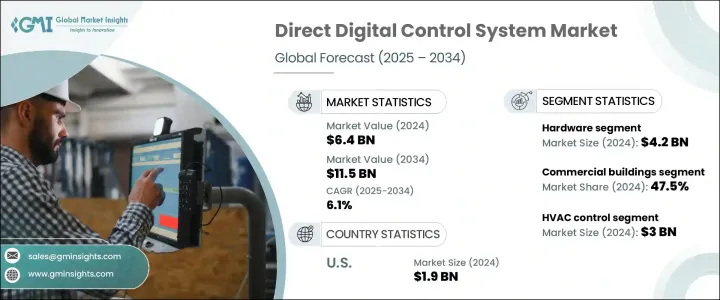

直接デジタル制御システムの世界市場規模は、2024年に64億米ドルとなり、急速な都市化と工業化に伴うスマートインフラストラクチャの需要増加により、CAGR 6.1%で成長し、2034年には115億米ドルに達すると予測されています。

これらのシステムは、建物内のHVAC、照明、エネルギー運用を管理し、効率、快適性、持続可能性を高めるのに役立ちます。特にインド、アフリカ、ラテンアメリカなどの開発途上地域で都市の拡大が続く中、インテリジェントな自動ビル管理システムの需要が急増しています。DDCシステムは、エネルギーの最適化、自動化、手作業の軽減に役立ち、大規模なインフラ・プロジェクトに不可欠なものとなっています。

これらのシステムは、暖房、換気、空調(HVAC)、照明、その他の重要なビル機能をシームレスに制御し、全体的な効率と持続可能性を向上させる。快適性を確保しながらエネルギー消費を最適化できることが、商業、住宅、工業の各分野で広く採用されている主な要因です。しかし、関税政策による混乱が、中国、EU、カナダなどの主要製造地域からの重要な電子部品、センサー、コントローラーの輸入を妨げているなどの課題に市場は直面しています。こうした地政学的要因は、プロジェクトのスケジュールを遅らせ、DDCシステムメーカーのコストを増加させる可能性があります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 64億米ドル |

| 予測金額 | 115億米ドル |

| CAGR | 6.1% |

DDCシステム市場は主にハードウェア、ソフトウェア、サービスに区分され、ハードウェアが支配的なセグメントです。2024年のハードウェア分野の市場規模は42億米ドルです。コントローラー、センサー、アクチュエーターなどの中核部品は、DDCシステムが効果的に機能するために不可欠です。スマートインフラへの需要が世界的、特に新興市場で高まるにつれ、リアルタイムの監視、正確な自動化、効率的なエネルギー管理を可能にする高度なハードウェアソリューションへのニーズが高まっています。このハードウェアは、さまざまなビル機能を高レベルで制御し、エネルギー効率と居住者の快適性を確保します。

エネルギー使用量が多く、インフラが複雑な商業ビルは、2024年のシェア47.5%を占めました。DDCシステムは、効率的なエネルギー管理と居住者の快適性が強く求められるオフィスビル、ショッピングモール、空港、ホテルなどで広く使用されています。こうした建物は複雑な性質を持つため、DDCシステムは運用の自動化に理想的な選択肢となり、運用コストの削減と建物全体の性能向上につながります。持続可能性とエネルギー効率に対する意識の高まりも、DDCシステムを商業施設のエネルギー資源管理の魅力的なソリューションにしています。

米国直接デジタル制御システム2024年の市場規模は19億米ドルであり、商業ビル、施設、産業ビルにおけるこれらのシステムの広範な採用が牽引しています。厳しいエネルギー効率規制と、古い建物を高度な自動化ソリューションで改修する動向の高まりが、米国での市場拡大に大きく寄与しています。さらに、DDC業界の大手プレイヤーの存在が市場の成長と技術革新をさらに後押しし、さまざまな部門向けに高品質で効率的なシステムの安定供給を保証しています。

世界の直接デジタル制御システム業界の主要企業には、シュナイダーエレクトリック社、アズビル社、ハネウェルインターナショナル社、ジョンソンコントロールズ社などがあります。DDCシステム市場におけるプレゼンスを強化するため、各社は製品の性能と費用対効果を高める研究開発に多額の投資を行っています。エネルギー効率と拡張性の向上に注力することで、スマート・ビル・ソリューションに対する需要の高まりに応えることを目指しています。また、多くの企業が、包括的な設置、メンテナンス、システム統合サービスを含むサービスの提供を拡大しており、顧客がDDCシステムの価値を最大限に引き出せるようにしています。商業・産業界との戦略的パートナーシップは、各社の市場拡大に貢献しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界の対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 影響要因

- 促進要因

- スマートビルディング技術の導入増加

- 急速な都市化と工業化

- エネルギー効率に対する需要の高まり

- 老朽化したインフラと改修需要

- 自動化および制御システムにおける技術的進歩

- 業界の潜在的リスク&課題

- 初期設置コストが高め

- 統合の複雑さ

- 促進要因

- 成長可能性分析

- テクノロジーとイノベーションの情勢

- 主なニュースと取り組み

- 将来の市場動向

- ポーター分析

- PESTEL分析

- 規制情勢

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ハードウェア

- コントローラー

- センサー

- アクチュエータ

- 入出力モジュール

- その他

- ソフトウェア

- 制御アルゴリズム

- インターフェースと視覚化ツール

- データ分析ソフトウェア

- その他

- サービス

- インストールと統合

- メンテナンスとサポート

- コンサルティングとトレーニング

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- HVAC制御

- 照明制御

- 産業オートメーション

- エネルギー管理システム(EMS)

- その他

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 住宅

- 商業ビル

- オフィススペース

- 小売店

- おもてなし

- 産業施設

- 製造工場

- 倉庫

- 公共施設

- 病院

- 学校

- 政府庁舎

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Allison Mechanical、Inc.

- Arvin Air Systems

- Azbil Corporation

- Computrols、Inc.

- DEOS AG

- Honeywell International Inc.

- Innotech

- Johnson Controls Inc.

- KMC Controls

- Lennox International Inc.

- Mason &Barry

- Matrix HG、Inc.

- Mitsubishi Electric Corporation

- Schneider Electric

- Siemens

- Winona Heating &Ventilating

- WODFA Company

The Global Direct Digital Control System Market was valued at USD 6.4 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 11.5 billion by 2034, driven by the increasing demand for smart infrastructure, fueled by rapid urbanization and industrialization. These systems help manage HVAC, lighting, and energy operations within buildings, enhancing efficiency, comfort, and sustainability. As urban expansion continues, particularly in developing regions such as India, Africa, and Latin America, the demand for intelligent, automated building management systems is surging. DDC systems help in energy optimization, automation, and reducing manual labor, making them indispensable for large-scale infrastructure projects.

These systems allow for seamless control of heating, ventilation, air conditioning (HVAC), lighting, and other critical building functions, improving overall efficiency and sustainability. Their ability to optimize energy consumption while ensuring comfort is a key factor behind their widespread adoption in the commercial, residential, and industrial sectors. However, the market faces challenges, such as the disruptions caused by tariff policies, which have hindered the import of critical electronic components, sensors, and controllers from major manufacturing regions like China, the EU, and Canada. These geopolitical factors can delay project timelines and increase costs for DDC system manufacturers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.4 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 6.1% |

The DDC system market is primarily segmented into hardware, software, and services, with hardware being the dominant segment. In 2024, the hardware segment was valued at USD 4.2 billion. The core components, including controllers, sensors, and actuators, are essential for the effective functioning of DDC systems. As the demand for smart infrastructure grows globally, especially in emerging markets, there is an increasing need for advanced hardware solutions that enable real-time monitoring, precise automation, and efficient energy management. This hardware facilitates high-level control across various building functions, ensuring energy efficiency and occupant comfort.

Commercial buildings, with their high energy usage and complex infrastructure, represented a 47.5% share in 2024. DDC systems are extensively used in office buildings, shopping malls, airports, and hotels, where there is a strong need for efficient energy management and occupant comfort. The complex nature of these buildings makes DDC systems an ideal choice for automating operations, thereby reducing operational costs and enhancing overall building performance. The increasing awareness of sustainability and energy efficiency also makes DDC systems an attractive solution for managing energy resources in commercial facilities.

U.S. Direct Digital Control System Market was valued at USD 1.9 billion in 2024, driven by the widespread adoption of these systems across commercial, institutional, and industrial buildings. Strict energy efficiency regulations and the growing trend of retrofitting older buildings with advanced automation solutions have significantly contributed to the market's expansion in the U.S. Additionally, the presence of major players in the DDC industry further supports the growth and innovation in the market, ensuring a steady supply of high-quality and efficient systems for various sectors.

Key players in the Global Direct Digital Control System Industry include Schneider Electric, Azbil Corporation, Honeywell International Inc., and Johnson Controls Inc. To strengthen their presence in the DDC system market, companies are heavily investing in research and development to enhance the performance and cost-effectiveness of their products. By focusing on improving energy efficiency and scalability, they aim to cater to the growing demand for smart building solutions. Many players are also expanding their service offerings to include comprehensive installation, maintenance, and system integration services, ensuring clients can maximize the value of DDC systems. Strategic partnerships with commercial and industrial players help companies expand their market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 key companies impacted

- 3.2.4 strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increased adoption of smart building technologies

- 3.3.1.2 Rapid urbanization and industrialization

- 3.3.1.3 Rising demand for energy efficiency

- 3.3.1.4 Aging infrastructure and retrofitting demand

- 3.3.1.5 Technological advancements in automation and control systems

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High initial installation costs

- 3.3.2.2 Complexity of integration

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Technological & innovation landscape

- 3.6 Key news and initiatives

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Regulatory landscape

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Controllers

- 5.2.2 Sensors

- 5.2.3 Actuators

- 5.2.4 Input/output modules

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Control algorithms

- 5.3.2 Interface & visualization tools

- 5.3.3 Data analytics software

- 5.3.4 Others

- 5.4 Services

- 5.4.1 Installation & integration

- 5.4.2 Maintenance & support

- 5.4.3 consulting & training

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 HVAC control

- 6.3 Lighting control

- 6.4 Industrial automation

- 6.5 Energy management systems (EMS)

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By End use, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Residential buildings

- 7.3 Commercial buildings

- 7.3.1 office spaces

- 7.3.2 retail stores

- 7.3.3 hospitality

- 7.4 Industrial facilities

- 7.4.1 manufacturing plants

- 7.4.2 warehouses

- 7.5 Institutional buildings

- 7.5.1 hospitals

- 7.5.2 schools

- 7.5.3 government buildings

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Allison Mechanical, Inc.

- 9.2 Arvin Air Systems

- 9.3 Azbil Corporation

- 9.4 Computrols, Inc.

- 9.5 DEOS AG

- 9.6 Honeywell International Inc.

- 9.7 Innotech

- 9.8 Johnson Controls Inc.

- 9.9 KMC Controls

- 9.10 Lennox International Inc.

- 9.11 Mason & Barry

- 9.12 Matrix HG, Inc.

- 9.13 Mitsubishi Electric Corporation

- 9.14 Schneider Electric

- 9.15 Siemens

- 9.16 Winona Heating & Ventilating

- 9.17 WODFA Company