|

市場調査レポート

商品コード

1750446

車載ソーラーパネルの市場機会、成長促進要因、産業動向分析、2025~2034年予測Vehicle-Integrated Solar Panels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 車載ソーラーパネルの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月08日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

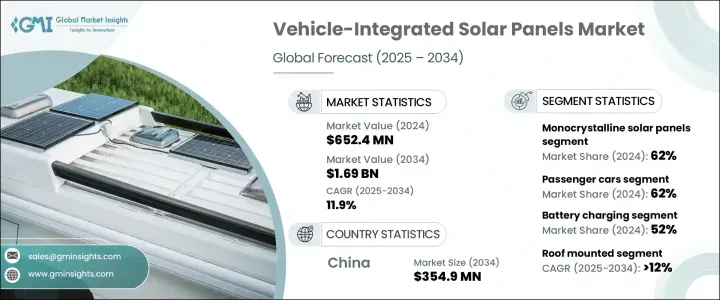

世界の車載ソーラーパネル市場は、2024年に6億5,240万米ドルと評価され、電動モビリティへの移行が広まり、再生可能エネルギーへの世界の後押しが強まる中、車両統合型ソーラーシステムの需要が牽引し、CAGR 11.9%で成長し、2034年には16億9,000万米ドルに達すると予測されています。

輸送システムの近代化に伴い、自動車メーカーは外部充電システムへの依存を減らすため、太陽光発電を自動車に直接統合することを検討するようになっています。VISPはクリーンで自立的なエネルギー生成を可能にし、車載バッテリーへの負担を軽減すると同時に、電気自動車の走行距離の延長に貢献します。

環境意識、不安定な燃料価格、脱炭素交通ソリューションに対する政府支援の高まりが市場成長に寄与しています。自動車メーカーは、より効率的な太陽電池材料の革新、車両設計との統合の強化、エネルギー変換率の最適化によって対応しています。消費者の関心は拡大しており、特に日照量の多い地域では、ソーラーカーによってエネルギー自給率を高めることができます。バイヤーは、耐熱ソーラー素材、シームレスなデザイン統合、リアルタイムのエネルギー追跡など、先進的な車両機能を優先しています。消費者直販のデジタル販売チャネルの進化は、ソーラー対応車と関連アフターマーケットキットの認知度を高め、メーカーがより幅広い層にリーチできるようにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億5,240万米ドル |

| 予測金額 | 16億9,000万米ドル |

| CAGR | 11.9% |

乗用車は2024年に62%のシェアを占めて市場をリードし、2034年までCAGR 12.3%で成長すると予想されます。これらの車両は、表面が平らで空気力学的に優れているため、VISP技術にとって理想的なプラットフォームとなります。この設計により、ソーラー・システムは限られたスペースでより高い発電量を得ることができます。日射量の多い地域では、自己充電能力は都市部や都市間の移動にとって特に貴重なものとなります。環境意識の高いドライバーに強くアピールする太陽電池一体型システムは、EV分野で急速に差別化要因になりつつあります。

単結晶ソーラーパネル・セグメントは62%のシェアを占め、2034年までのCAGRは12.2%と予想されています。これらのパネルは、優れたエネルギー変換効率と見た目の均一性が支持されています。日陰や高温の環境でもよく動作することで知られる単結晶パネルは、自動車のルーフトップやボンネットに最適です。洗練された外観と一貫した質感により、性能と美観が重視されるプレミアムEVに人気があります。

アジア太平洋の車載一体型ソーラーパネル市場は、2024年に48%のシェアを占める。強力な国内生産能力、コスト効率の高い製造、政府主導の再生可能モビリティ政策が、VISP採用における中国のリーダーシップを後押ししています。さらに、同国の強固なインフラ開発、スマート物流網の拡大、急速な都市化が、トラック搭載型ナックルブームクレーンのような汎用性の高いリフティング・ソリューションの必要性を煽っています。地元メーカーは、スケールメリットと合理化されたサプライチェーンの恩恵を受け、迅速な生産と競争力のある価格設定を可能にしています。

Sono Motors、Volkswagen、トヨタ自動車、BYD、日産自動車、Lightyear、Planet Solar、Aptera Motors、General Motors、Ford Motorといった主要な業界参加企業は、競争力を維持するために戦略的提携や技術アップグレードを進めています。その多くは、太陽電池の耐久性、エネルギー効率、EVプラットフォームとの統合を強化するための研究開発に投資しています。太陽電池技術企業との戦略的提携や、対象市場での試験車両の展開も一般的です。消費者向けオンライン直販モデルを最適化する企業もあれば、フリート採用やラストマイル物流用途のモジュール式VISPソリューションに注力する企業もあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- サービスプロバイダー

- 卸売業者

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 価格動向

- 製品

- 地域

- コスト内訳分析

- 影響要因

- 促進要因

- 電気自動車の普及の増加

- 太陽光パネルの効率における技術的進歩

- 太陽光発電技術のコスト低下

- 再生可能エネルギーに対する消費者の意識の高まり

- 環境規制と炭素削減目標

- 業界の潜在的リスク&課題

- 統合の初期コストが高め

- 耐久性と安全性に関する懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車

- 中型商用車

- 大型商用車

- 電気自動車(EV)

- 特殊車両

- レクリエーション車両(RV)

- ゴルフカート

- 軍用車両または緊急車両

第6章 市場推計・予測:ソーラーパネル別、2021-2034

- 主要動向

- 単結晶ソーラーパネル

- 多結晶ソーラーパネル

- 薄膜太陽電池パネル

- フレキシブルソーラーパネル

第7章 市場推計・予測:設置方法別、2021-2034

- 主要動向

- 屋根に取り付け

- フードを取り付けた

- 一体型ボディパネル

- 取り外し可能なパネル

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- 発電

- バッテリー充電

- 補助電源

- 暖房システム

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Aptera Motors

- BYD

- Cruise Car

- Ford Motor

- General Motors

- Hanergy Thin Film

- Honda Motor

- Hyundai Motor

- Lightyear

- LOMOcean

- Mahindra &Mahindra

- Nissan Motor

- Planet Solar

- Sono Motors

- Surat Exim

- Tesla

- Toyota Motor

- Venturi Automobiles

- Volkswagen

- Weifang Guangsheng New Energy

The Global Vehicle-Integrated Solar Panels Market was valued at USD 652.4 million in 2024 and is estimated to grow at a CAGR of 11.9% to reach USD 1.69 billion by 2034, driven by the demand for vehicle-integrated solar systems with the widespread shift toward electric mobility and the growing global push for renewable energy. As transportation systems modernize, vehicle manufacturers are increasingly looking to integrate solar power directly into vehicles to reduce reliance on external charging systems. VISPs enable clean, self-sustaining energy generation, helping extend the operational range of electric vehicles while alleviating pressure on onboard batteries.

Environmental awareness, volatile fuel prices, and growing government support for decarbonized transportation solutions contribute to market growth. Automakers are responding by innovating more efficient solar materials, enhancing their integration with vehicle designs, and optimizing energy conversion rates. Consumer interest is expanding, especially in sunny regions, where solar-powered cars can deliver greater energy independence. Buyers prioritize advanced vehicle features such as thermal-resistant solar materials, seamless design integration, and real-time energy tracking. The evolution of direct-to-consumer digital sales channels boosts visibility for solar-enabled vehicles and related aftermarket kits, allowing manufacturers to reach a broader demographic base.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $652.4 Million |

| Forecast Value | $1.69 Billion |

| CAGR | 11.9% |

Passenger vehicles led the market in 2024, making up 62% share, and are expected to grow at 12.3% CAGR through 2034. These vehicles provide ideal platforms for VISP technology due to their flat, aerodynamic surfaces. This design allows solar systems to generate higher electricity outputs from limited space. In regions with high solar exposure, the ability to self-charge becomes especially valuable for urban and intercity mobility. With a strong appeal among environmentally conscious drivers, solar-integrated systems are rapidly becoming a differentiator in the EV space.

The monocrystalline solar panels segment held 62% share and is expected to grow at a CAGR of 12.2% through 2034. These panels are favored for their superior energy conversion efficiency and visual uniformity. Known for operating well in shaded and high-temperature environments, monocrystalline panels are ideal for vehicle rooftops and hoods. Their sleek appearance and consistent texture make them popular for premium EVs where performance and aesthetics matter.

Asia Pacific Vehicle- Integrated Solar Panels Market held a 48% share in 2024. Strong domestic production capabilities, cost-effective manufacturing, and government-led renewable mobility policies have propelled China's leadership in VISP adoption. Additionally, the country's robust infrastructure development, expansion of smart logistics networks, and rapid urbanization have fueled the need for versatile lifting solutions like truck-mounted knuckle boom cranes. Local manufacturers benefit from economies of scale and streamlined supply chains, enabling faster production and competitive pricing.

Key industry participants such as Sono Motors, Volkswagen, Toyota Motor, BYD, Nissan Motor, Lightyear, Planet Solar, Aptera Motors, General Motors, and Ford Motor are pursuing strategic collaborations and technology upgrades to stay competitive. Many invest in R&D to enhance solar cell durability, energy efficiency, and integration with EV platforms. Strategic partnerships with solar tech firms and the rollout of pilot vehicles in target markets are also common. Some players optimize direct-to-consumer online sales models, while others focus on modular VISP solutions for fleet adoption and last-mile logistics applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Component supplier

- 3.2.3 Manufacturer

- 3.2.4 Service provider

- 3.2.5 Distributor

- 3.2.6 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing trend

- 3.9.1 Product

- 3.9.2 Region

- 3.10 Cost breakdown analysis

- 3.11 Impact on forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rising adoption of electric vehicles

- 3.11.1.2 Technological advancements in solar panel efficiency

- 3.11.1.3 Decreasing cost of solar technology

- 3.11.1.4 Growing consumer awareness of renewable energy

- 3.11.1.5 Environmental regulations and carbon reduction goals

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High initial cost of integration

- 3.11.2.2 Durability and safety concerns

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicles

- 5.3.2 Medium commercial vehicles

- 5.3.3 Heavy commercial vehicles

- 5.4 Electric vehicles (EVs)

- 5.5 Specialty Vehicles

- 5.5.1 Recreational vehicles (RVs)

- 5.5.2 Golf carts

- 5.5.3 Military or emergency vehicles

Chapter 6 Market Estimates & Forecast, By Solar Panel, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Monocrystalline solar panels

- 6.3 Polycrystalline solar panels

- 6.4 Thin-film solar panels

- 6.5 Flexible solar panels

Chapter 7 Market Estimates & Forecast, By Installation Method, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Roof mounted

- 7.3 Hood mounted

- 7.4 Integrated body panels

- 7.5 Removable panels

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Power generation

- 8.3 Battery charging

- 8.4 Auxiliary power supply

- 8.5 Heating systems

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Aptera Motors

- 10.2 BYD

- 10.3 Cruise Car

- 10.4 Ford Motor

- 10.5 General Motors

- 10.6 Hanergy Thin Film

- 10.7 Honda Motor

- 10.8 Hyundai Motor

- 10.9 Lightyear

- 10.10 LOMOcean

- 10.11 Mahindra & Mahindra

- 10.12 Nissan Motor

- 10.13 Planet Solar

- 10.14 Sono Motors

- 10.15 Surat Exim

- 10.16 Tesla

- 10.17 Toyota Motor

- 10.18 Venturi Automobiles

- 10.19 Volkswagen

- 10.20 Weifang Guangsheng New Energy