|

市場調査レポート

商品コード

1892860

光干渉断層計(OCT)市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Optical Coherence Tomography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 光干渉断層計(OCT)市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年12月11日

発行: Global Market Insights Inc.

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

概要

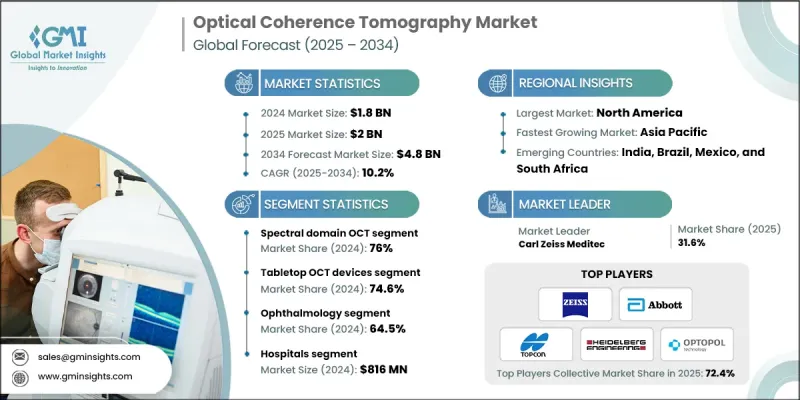

世界の光干渉断層計(OCT)市場は、2024年に18億米ドルと評価され、2034年までにCAGR10.2%で成長し、48億米ドルに達すると予測されております。

OCTは低コヒーレンス光を用いた非侵襲的な画像診断法であり、生体組織の極めて詳細な断面画像を生成します。診断精度の向上、組織深部への到達深度拡大、画像取得速度の高速化を目的とした研究開発が加速する中、市場は成長を続けております。こうした進歩により、様々な臨床環境において次世代診断ツールや治療モニタリングシステムの導入が促進されております。コンパクトで携帯可能なOCT装置への需要の高まりも開発動向に影響を与えており、特に医療提供者が地方診療所、移動診療所、在宅ケア施設、外来センターなどにおけるポイントオブケア検査のためのアクセス可能なソリューションを求める中で顕著です。移動性とワークフロー効率化への移行が進む中、メーカー各社はより広範な臨床用途を想定した、簡素化され使いやすいイメージングシステムの導入を促進しております。主要な眼疾患に対する早期発見戦略の導入拡大は、現代の眼科医療におけるOCT技術への依存度をさらに強固にしております。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年度 | 2025-2034 |

| 開始時価値 | 18億米ドル |

| 予測金額 | 48億米ドル |

| CAGR | 10.2% |

スペクトルドメインOCTセグメントは、2024年に76%のシェアを占めました。このセグメントが主導的な地位にあるのは、網膜の健康に影響を与える慢性眼疾患の発生率が増加しており、正確で迅速、かつ高解像度の画像診断の必要性が高まっているためです。SD-OCT装置は網膜診断だけでなく、前眼部、角膜疾患、視神経の評価にも頻繁に活用されています。疾患の病期判定から治療後の経過観察まで、多様な臨床業務に対応可能な適応性により、包括的な視力評価に不可欠な存在となっております。

卓上型OCT装置セグメントは、2024年に74.6%のシェアを占めました。これらのシステムは、安定した高精度な画像提供と複数スキャン技術との互換性を備えているため、眼科専門家の間で依然として好まれる選択肢です。緑内障の進行、網膜疾患、前眼部の健康状態の分析を支援する能力により、眼科センター、専門施設、病院部門での広範な利用が支えられています。現代の卓上型装置は、複数の画像技術を単一プラットフォームに統合し、効率的な診断ワークステーションを形成することが多いです。

米国における光干渉断層計(OCT)市場は、2024年に6億3,100万米ドルに達し、2034年までに16億米ドルに達すると予測されています。メディケアおよび民間保険会社によるOCT関連処置の広範な保険適用は、患者と医療提供者の双方にとってのコスト削減につながり、市場導入を促進しています。保険適用は視神経分析、網膜スキャン、OCT血管造影など複数の用途に適用され、眼科診療においてOCTを日常的な臨床ワークフローに組み込むことを後押ししています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- OCTコンポーネントのOEMメーカー

- メーカー

- 規制当局

- 販売代理店およびサプライヤー

- 最終用途

- 業界への影響要因

- 促進要因

- 眼疾患の増加傾向

- OCT技術の進歩

- 非侵襲的診断技術の普及拡大

- 新興経済国における医療投資と意識の高まり

- 業界の潜在的リスク&課題

- 治療法の高コスト

- OCTシステムの操作および解釈に関する訓練を受けた熟練専門家の不足

- 市場機会

- AIを活用した診断アルゴリズムと自動分析

- 小児科および集中治療分野におけるOCTの応用拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- アジア太平洋地域

- 技術動向

- 現在の技術動向

- 深部組織可視化のためのスイープ光源OCT

- 非侵襲的血管マッピングのためのOCT血管造影

- ポータブルかつマルチモーダルOCTデバイスによるポイントオブケア診断

- 新興技術

- 超高感度イメージングのための量子強化OCT

- リアルタイム収差補正のための適応光学統合

- 3.動的3D組織可視化のための超高速OCT

- 現在の技術動向

- 特許分析

- 主要特許保有者および技術リーダー

- 特許満了分析と影響

- 特許訴訟および紛争

- 地域別特許保護戦略

- 価格分析、2024

- 将来の市場動向

- 予測診断のためのAI駆動型OCTプラットフォーム

- クラウドベースのOCTデータ管理と遠隔医療の統合

- 眼科領域を超えたOCT応用分野の拡大

- サプライチェーンと流通分析

- 原材料調達

- 製造拠点分析

- 流通チャネルのマッピングとパートナーネットワーク

- サプライチェーンの脆弱性とリスク軽減策

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

第5章 市場推計・予測:技術別、2021-2034

- 主要動向

- スペクトル領域OCT

- スイープソースOCT

- 時間領域OCT

第6章 市場推計・予測:製品・サービス別、2021-2034

- 主要動向

- 機器

- 卓上型OCT装置

- カテーテルベースOCT装置

- ハンドヘルドOCT装置

- ドップラーOCT装置

- 部品交換サービスおよびソフトウェアライセンシング・アップグレード

- その他のサービス

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 眼科

- 循環器学

- 皮膚科

- 腫瘍学

- その他の用途

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 診断画像センター

- 外来手術センター

- その他の用途

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott Laboratories

- Agfa-Gevaert

- Canon

- Carl Zeiss Meditec

- Gentuity

- Heidelberg Engineering

- Huvitz

- Metall Zug AG(Haag-Streit Group)

- Moptim(Shenzhen Certainn Technology)

- NIDEK

- Nikon Corporation(Optos plc)

- NinePoint Medical

- Notal Vision

- Novacam Technologies

- OPTOPOL Technology

- Philophos

- Tomey

- Topcon Corporation

- TowardPi(Beijing)Medical Technology

- Visionx

- Vivolight

- YSENMED

- ZD medical