|

市場調査レポート

商品コード

1750439

フックリフトトレーラーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Hooklift Trailer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| フックリフトトレーラーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月15日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

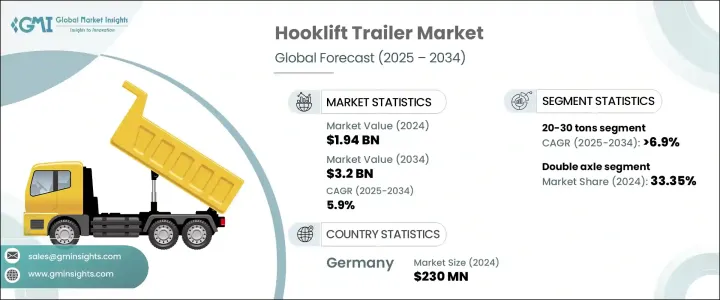

世界のフックリフトトレーラー市場は、2024年に19億4,000万米ドルと評価され、世界の建設、解体、インフラ開拓の急増により、CAGR 5.9%で成長し、2034年には32億米ドルに達すると推定されています。

これらのトレーラーは、その柔軟性、耐久性、効率性から、廃棄物処理、農業、鉱業、物流において不可欠な資産と見なされるようになってきています。産業界が時間と資源を最適化するためにモジュール式輸送システムにシフトする中、フックリフトトレーラーは多機能運搬能力を提供し、単一の車両プラットフォームで様々なコンテナタイプの使用を可能にします。

この適応性は、密集した都市部、遠隔の掘削地域、広大な農地など、現場の状況や貨物の種類が大きく異なる地域で特に魅力的です。さらに、オペレーションがダウンタイムとオペレーション・コストの削減に重点を置くようになるにつれ、高度な油圧システムとIoTベースのトラッキングのようなスマート・テクノロジーが重要な機能になってきています。これらの統合は、リアルタイムの診断とメンテナンス警告を提供し、総所有コストを下げながら、フリートの信頼性と生産性を向上させます。遠隔監視と予知保全を可能にすることで、オペレーターは問題が深刻化する前に特定することができ、計画外のダウンタイムと修理コストを削減することができます。さらに、これらのシステムを通じて収集されたパフォーマンス・データは、情報に基づいた意思決定を可能にし、燃料使用量とドライバーの行動を最適化します。長期的には、この可視性のレベルは、より良い資産管理、より長い機器寿命、より効率的なスケジューリングと運用効率をサポートします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 19億4,000万米ドル |

| 予測金額 | 32億米ドル |

| CAGR | 5.9% |

二軸トレーラーは2024年に33.35%のシェアを占め、2034年までのCAGRは6.7%と予測されます。耐荷重強度と操縦性のバランスで知られる両軸トレーラーは、農業、建設、廃棄物処理などの分野で高い支持を得ています。その設計は、厳しい条件下でも安定したハンドリングと長寿命を保証します。強化されたフレームとマルチコンテナ適合性により、これらのトレーラーは日常的な産業利用においてより効果的になり、新しい低燃費システムはさらに持続可能なソリューションへの関心の高まりを支えています。

容量20~30トンのフックリフトトレーラーは、2024年に34.23%の市場シェアを確保しました。この重量クラスは、積載量と多用途性の間で重要なバランスをとり、都市廃棄物、解体資材、採掘資源の輸送に理想的です。このセグメントの成長は、地形や物流のニーズが変化する作業において、移動を最小限に抑え、燃料消費を削減するという価値を反映しています。

ドイツフックリフトトレーラー2024年の市場規模は2億3,000万米ドル、市場シェアは28.6%。同国は、スマートな廃棄物システム、持続可能な開発、効率的な物流に注力しており、トレーラーの需要を支え続けています。Meiller、Krampeなどの地元メーカーは、自動化、長期耐久性、EU輸送基準への準拠を重視したイノベーションを推進してきました。

市場でのプレゼンスを拡大するため、Palfinger、Stellar Industries、SwapLoader、Hiab、Stronga、Hyva Group、VDL Containersystemen、Marrel SASなどの主要プレーヤーは、製品革新、統合油圧、テレマティクスに投資しています。その多くは、地域的なパートナーシップを形成し、アフターセールス・サポートを強化し、多様なエンドユーザー・ニーズに合わせたモジュラー機器オプションを提供しています。これらの戦略は、世界なフックリフトトレーラー空間における性能ベンチマークを設定しながら、各社が増大する需要に対応するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 部品サプライヤー

- 製造業者

- フリートオペレーター

- 販売代理店

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 価格動向

- 地域

- 車軸

- コスト内訳分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 建設および解体活動の増加

- 都市化とインフラ開発

- 効率的な物流の需要

- 公共インフラへの政府投資

- 業界の潜在的リスク&課題

- 初期投資コストが高め

- メンテナンスと運用の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:車軸別、2021-2034

- 主要動向

- シングルアクスル

- ダブルアクスル

- トリプルアクスル

- 多軸

第6章 市場推計・予測:耐荷重別、2021-2034

- 主要動向

- 10トン以下

- 10~20トン

- 20~30トン

- 30トン以上

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 建設・解体

- 都市廃棄物管理

- リサイクル事業

- 農業

- 鉱業と採石業

- 物流・輸送

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第9章 企業プロファイル

- Fahrzeugbau KEMPF

- Fliegl Agrartechnik

- Fors MW

- Fortuna Fahrzeugbau GmbH

- Hiab Corporation

- Hyva Group

- Joskin

- Krampe Fahrzeugbau

- Marrel SAS

- Meiller Group

- Metaltech

- MS DORSE

- Palfinger AG

- Palmse Metall

- Peeters Group

- Peter Kroger GmbH

- Stellar Industries

- Stronga

- SwapLoader USA

- VDL Containersystemen BV

The Global Hooklift Trailer Market was valued at USD 1.94 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 3.2 billion by 2034, driven by the surge in construction, demolition, and infrastructure development worldwide. These trailers are increasingly viewed as essential assets in waste handling, agriculture, mining, and logistics due to their flexibility, durability, and efficiency. As industries shift toward modular transport systems to optimize time and resources, hooklift trailers offer multi-functional hauling capabilities, allowing the use of various container types with a single vehicle platform.

This adaptability is particularly appealing in areas where jobsite conditions and cargo types vary widely, including dense urban locations, remote excavation areas, and expansive farmland. Additionally, as operations focus more on reducing downtime and operational costs, advanced hydraulic systems and smart technologies like IoT-based tracking are becoming key features. These integrations provide real-time diagnostics and maintenance alerts, improving fleet reliability and productivity while lowering total cost of ownership. By enabling remote monitoring and predictive maintenance, operators can identify issues before they escalate, reducing unplanned downtime and repair costs. Additionally, performance data collected through these systems allows for informed decision-making, optimizing fuel usage and driver behavior. Over time, this level of visibility supports better asset management, longer equipment lifespans, and more efficient scheduling and operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.94 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 5.9% |

The double axle trailers segment held a prominent 33.35% share in 2024 and is projected to grow at a CAGR of 6.7% through 2034. Known for balancing load-bearing strength with maneuverability, they're highly favored across sectors like agriculture, construction, and waste processing. Their design ensures stable handling and extended lifespan, even under demanding conditions. Reinforced frames and multi-container compatibility have made these trailers more effective for daily industrial use, while new fuel-efficient systems further support growing interest in sustainable solutions.

Hooklift trailers with a 20-30 ton capacity secured a 34.23% market share in 2024. This weight class strikes a critical balance between payload and versatility, making it ideal for transporting municipal waste, demolition materials, and mined resources. The segment's growth reflects its value in minimizing trips and reducing fuel consumption across operations with variable terrain and logistical needs.

Germany Hooklift Trailer Market generated USD 230 million and held 28.6% market share in 2024. The country's focus on smart waste systems, sustainable development, and efficient logistics continues to support trailer demand. Local manufacturers like Meiller, Krampe, and others have pushed innovations that emphasize automation, long-term durability, and compliance with EU transport standards.

To expand market presence, key players like Palfinger, Stellar Industries, SwapLoader, Hiab, Stronga, Hyva Group, VDL Containersystemen, and Marrel SAS are investing in product innovation, integrated hydraulics, and telematics. Many are forming regional partnerships, enhancing after-sales support, and offering modular equipment options tailored to diverse end-user needs. These strategies are helping companies meet growing demand while setting performance benchmarks in the global hooklift trailer space.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component suppliers

- 3.2.2 Manufacturers

- 3.2.3 Fleet operators

- 3.2.4 Distributors

- 3.2.5 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Price trend

- 3.7.1 Region

- 3.7.2 Axle

- 3.8 Cost breakdown analysis

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact on forces

- 3.11.1 Growth drivers

- 3.11.1.1 Increase in construction and demolition activities

- 3.11.1.2 Urbanization and infrastructure development

- 3.11.1.3 Demand for efficient logistics

- 3.11.1.4 Government investments in public infrastructure

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High initial investment cost

- 3.11.2.2 Maintenance and operational complexity

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Axle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Single axle

- 5.3 Double axle

- 5.4 Triple axle

- 5.5 Multi- axle

Chapter 6 Market Estimates & Forecast, By Load Capacity, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Below 10 tons

- 6.3 10–20 tons

- 6.4 20–30 tons

- 6.5 Above 30 tons

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Construction & demolition

- 7.3 Municipal waste management

- 7.4 Recycling operations

- 7.5 Agriculture

- 7.6 Mining & quarrying

- 7.7 Logistics & transportation

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Fahrzeugbau KEMPF

- 9.2 Fliegl Agrartechnik

- 9.3 Fors MW

- 9.4 Fortuna Fahrzeugbau GmbH

- 9.5 Hiab Corporation

- 9.6 Hyva Group

- 9.7 Joskin

- 9.8 Krampe Fahrzeugbau

- 9.9 Marrel SAS

- 9.10 Meiller Group

- 9.11 Metaltech

- 9.12 MS DORSE

- 9.13 Palfinger AG

- 9.14 Palmse Metall

- 9.15 Peeters Group

- 9.16 Peter Kroger GmbH

- 9.17 Stellar Industries

- 9.18 Stronga

- 9.19 SwapLoader USA

- 9.20 VDL Containersystemen BV