モバイルCアームの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Mobile C-arm Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750437

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

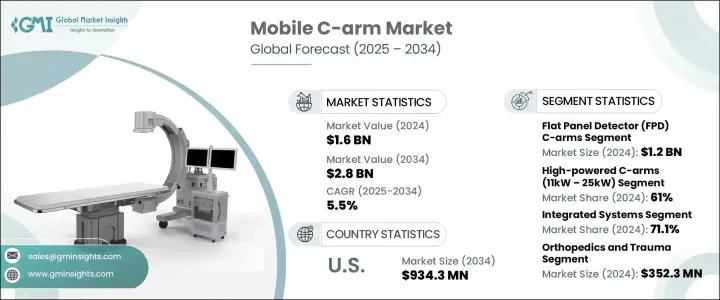

モバイルCアームの世界市場規模は、2024年に16億米ドルとなり、CAGR 5.5%で成長し、2034年には28億米ドルに達すると予測されています。

モバイルCアームシステムは、診断や外科手術中にリアルタイムでX線可視化を提供するように設計された先進的なポータブルイメージングツールです。画像フィードバックを即座に提供する機能は、臨床判断の支援、手術精度の向上、患者の転帰の改善に重要な役割を果たしています。心血管疾患、がん、神経疾患などの慢性疾患の世界の負担増は、これらの疾患の診断や治療に正確な画像診断が必要とされることが多いため、市場拡大の主な要因となっています。低侵襲手術に対する需要の高まりは、画像技術の進歩と相まって、先進地域と発展途上地域の両方で高性能モバイルCアームユニットの必要性をさらに高めています。病院やヘルスケア施設は、特に緊急時の迅速な診断と手術効率の向上を保証するため、これらのシステムに継続的に投資しています。ヘルスケアのインフラが世界的、特に新興市場で近代化を続ける中、モバイルCアームはその可搬性、精度、使いやすさから、最新の手術ワークフローに不可欠なものとなりつつあります。

検出器タイプでは、市場はイメージインテンシファイアCアームとフラットパネルディテクタ(FPD)Cアームに区分されます。フラットパネルディテクタCアームは、画質が向上し、コントラスト分解能が高く、解剖学的可視化が強化されています。そのため、脊椎手術、整形外科外傷、心血管インターベンションなどの複雑な手技に最適です。また、これらの検出器は放射線効率に優れ、低線量で鮮明な画像を得ることができるため、患者とオペレーターの安全性が向上します。FPDベースのシステムは、より広く安定した撮像野を提供し、手技中の体位変換の必要性を制限することで、ワークフローの中断をさらに減らします。フラットパネル検出器技術へのシフトは、手術精度の向上と画像処理プロセスの合理化において重要な役割を果たしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 16億米ドル |

| 予測金額 | 28億米ドル |

| CAGR | 5.5% |

出力に基づいて、市場は高出力Cアーム(11kW~25kW)と低出力Cアーム(2kW~10kW)に分けられます。高出力Cアームセグメントは、2024年に9億8,980万米ドルを占め、市場の61%を占めました。これらの大容量システムは、深部組織のイメージングや長時間のイメージングを必要とする複雑な手技に好まれています。神経血管手術、整形外科手術、心臓血管手術など、要求の厳しい手術中に高解像度の結果を提供できることから、手術室では必須の機器となっています。また、高負荷下での性能により、より大きな解剖学的領域での使用に適しており、複雑な手技の際にも鮮明な視覚化を保証します。

設計面では、市場は一体型システムと個別構成システムに分類されます。一体型移動式Cアームは2024年に71.1%のシェアで優位を占めています。これらのシステムは、すべてのイメージング・コンポーネントを1つのコンパクトなユニットに統合しており、混雑した臨床環境やスペースに制約のある臨床環境で特に重宝されます。オールインワン設計により、操作が簡素化され、セットアップ時間が短縮され、ワークフローの効率が向上します。統合されたシステムの利便性は、迅速なイメージングアクセスが不可欠な救急部やICUのような高圧的な医療環境で特に有用です。

モバイルCアーム市場は、アプリケーション別に、整形外科・外傷、神経科、循環器科、消化器科、歯科、腫瘍科、その他の用途をカバーしています。整形外科・外傷分野は、2024年の売上高が3億5,230万米ドルで市場をリードしました。事故による負傷や加齢に伴う骨障害の増加により、リアルタイムの術中画像診断に対する需要が高まっています。モバイルCアームは、骨のアライメントやインプラントの埋入位置を正確に視覚化し、手術成績を大幅に向上させ、合併症を最小限に抑えます。リアルタイムの3D画像や放射線量制御などの技術的進歩が、整形外科医療におけるこれらのシステムの使用をさらに後押ししています。

最終用途に基づき、市場は病院、診断センター、その他のヘルスケア環境に区分されます。病院は、2024年の売上高が8億1,870万米ドルで市場をリードしています。幅広いサービスを提供し、患者の処理能力が高いことから、信頼性が高く高性能の画像処理システムが必要とされています。病院のモバイルCアームは、整形外科、泌尿器科、心臓血管治療など、さまざまな専門分野で使用されています。特に都市部での病院数の増加が、機器需要の増加に直接寄与しています。また、病院内に訓練を受けた専門家がいることで、モバイルCアームシステムの安全かつ効果的な使用が可能になり、採用率の向上につながっています。

地域別では、北米が2024年に5億6,370万米ドルで市場を席巻し、2034年には9億3,430万米ドルに達すると予測されています。米国がシェアの大半を占め、2024年には4億9,750万米ドルを記録しました。外科的介入を必要とする慢性疾患の増加により、この地域の病院や診療所は最先端の画像技術への投資を進めています。主要業界プレイヤーの存在感が強く、高度なヘルスケアインフラが整っていることが、この地域の市場成長をさらに後押ししています。

主要企業の市場競争は激しく、上位4社で世界シェアの45%近くを占めています。主要企業には、GEヘルスケアテクノロジーズ、シーメンス・ヘルスイニアーズ、Koninklijke Philips、Ziehm Imagingが含まれます。これらの企業は、絶え間ない技術革新、強力な世界販売網、戦略的な規制計画によって市場の優位性を維持しています。また、研究機関や公衆衛生機関との協力関係も、次世代画像ソリューションを市場に投入する努力を支えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 外科手術の増加

- 慢性疾患の有病率の上昇

- モバイルCアームマシンの技術的進歩

- 低侵襲手術の需要の高まり

- 業界の潜在的リスク&課題

- モバイルCアームマシンに関連する高コスト

- 熟練したヘルスケア専門家の不足

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 国別の対応

- 業界への影響

- 供給側の影響(製造コスト)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(消費者のコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(製造コスト)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーの情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:検出器の種類別、2021 –2034

- 主要動向

- フラットパネル検出器(FPD)Cアーム

- タイプ

- アモルファスシリコン(a-Si)検出器

- インジウムガリウム亜鉛酸化物(IGZO)検出器

- 相補型金属酸化膜半導体(CMOS)検出器

- サイズ

- 20cm×20cm

- 26 cm×26 cm

- 30cm×30cm

- その他のサイズ

- タイプ

- イメージインテンシファイアCアーム

第6章 市場推計・予測:出力別、2021 –2034

- 主要動向

- 低出力Cアーム(2kW~10kW)

- 高出力Cアーム(11kW~25kW)

第7章 市場推計・予測:設計構成別、2021 –2034

- 主要動向

- 統合システム

- 個別の構成システム

第8章 市場推計・予測:用途別、2021 –2034

- 主要動向

- 整形外科と外傷

- 心臓病学

- 神経学

- 消化器内科

- 腫瘍学

- 歯科

- その他の用途

第9章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 病院

- 診断センター

- その他のエンドユーザー

第10章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Fujifilm Holdings Corporation

- GE HealthCare Technologies

- Genoray Co

- Hologic

- Koninklijke Philips

- Nanjing Perlove Medical Equipment Co

- Shimadzu Corporation

- Siemens Healthineers

- SternMed

- Stephanix

- Turner Imaging Systems

- Ziehm Imaging

目次

The Global Mobile C-Arm Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 2.8 billion by 2034. Mobile C-arm systems are advanced, portable imaging tools designed to deliver real-time X-ray visualization during diagnostic and surgical procedures. Their ability to provide immediate imaging feedback plays a vital role in supporting clinical decisions, improving surgical accuracy, and enhancing patient outcomes. The rising global burden of chronic illnesses such as cardiovascular conditions, cancer, and neurological disorders is a key driver of market expansion, as these conditions often require precise imaging for diagnosis and treatment. Increasing demand for minimally invasive surgeries, coupled with advancements in imaging technology, is further boosting the need for high-performance mobile C-arm units in both developed and developing regions. Hospitals and healthcare facilities are continuously investing in these systems to ensure faster diagnostics and improved surgical efficiency, particularly in emergency settings. As healthcare infrastructure continues to modernize globally, especially in emerging markets, mobile C-arms are becoming integral to modern surgical workflows due to their portability, precision, and ease of use.

In terms of detector type, the market is segmented into image intensifier C-arms and flat panel detector (FPD) C-arms. Flat panel detector C-arms offer improved image quality, higher contrast resolution, and enhanced anatomical visualization. This makes them ideal for intricate procedures such as spinal surgeries, orthopedic trauma, and cardiovascular interventions. These detectors also offer better radiation efficiency, producing clearer images at lower doses, which enhances patient and operator safety. FPD-based systems further reduce workflow interruptions by providing a broader and more stable imaging field, limiting the need for repositioning during procedures. The shift toward flat panel detector technology is playing a crucial role in improving surgical precision and streamlining imaging processes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 5.5% |

Based on power output, the market is divided into high-powered C-arms (11kW-25kW) and low-powered C-arms (2kW-10kW). The high-powered C-arm segment accounted for USD 989.8 million in 2024, capturing 61% of the market. These high-capacity systems are preferred for complex procedures requiring deep tissue imaging and extended imaging durations. Their ability to deliver high-resolution results during demanding interventions, such as neurovascular, orthopedic, and cardiovascular surgeries, has made them essential equipment in operating rooms. Their performance under high workloads also makes them well-suited for use in larger anatomical regions, ensuring clearer visualizations during intricate procedures.

Design-wise, the market is categorized into integrated systems and separate configuration systems. Integrated mobile C-arms dominated with a 71.1% share in 2024. These systems combine all imaging components into a single compact unit, making them especially valuable in crowded or space-constrained clinical environments. Their all-in-one design simplifies operation, reduces setup time, and improves workflow efficiency. The convenience of integrated systems is especially useful in high-pressure medical environments such as emergency departments and ICUs, where rapid imaging access is essential.

By application, the mobile C-arm market covers orthopedics and trauma, neurology, cardiology, gastroenterology, dental, oncology, and other uses. The orthopedics and trauma segment led the market in 2024 with USD 352.3 million in revenue. The increasing volume of accident-related injuries and age-related bone disorders has elevated the demand for real-time intraoperative imaging. Mobile C-arms offer accurate visualization of bone alignment and implant placement, significantly enhancing surgical outcomes and minimizing complications. Technological advancements, such as real-time 3D imaging and radiation dose control, are further supporting the use of these systems in orthopedic care.

Based on end use, the market is segmented into hospitals, diagnostic centers, and other healthcare settings. Hospitals led the market with USD 818.7 million in revenue in 2024. Their wide service offerings and high patient throughput necessitate reliable, high-performance imaging systems. Mobile C-arms in hospitals are used across various specialties including orthopedics, urology, and cardiovascular care. The growing number of hospitals, especially in urban areas, directly contributes to increasing equipment demand. Additionally, the availability of trained professionals in hospitals enhances the safe and effective use of mobile C-arm systems, encouraging higher adoption rates.

Regionally, North America dominated the market with USD 563.7 million in 2024 and is projected to reach USD 934.3 million by 2034. The United States contributed the majority share, recording USD 497.5 million in 2024. The growing incidence of chronic conditions requiring surgical interventions is pushing hospitals and clinics in the region to invest in state-of-the-art imaging technology. The strong presence of key industry players and the availability of advanced healthcare infrastructure further drive market growth in the region.

The mobile C-arm market is highly competitive, with the top four players accounting for nearly 45% of the global share. Key companies include GE HealthCare Technologies, Siemens Healthineers, Koninklijke Philips, and Ziehm Imaging. These firms maintain market dominance through continuous innovation, strong global distribution, and strategic regulatory planning. Collaborations with research institutions and public health organizations also support their efforts in bringing next-generation imaging solutions to the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing number of surgical procedures

- 3.2.1.2 Rising prevalence of chronic diseases

- 3.2.1.3 Technological advancements of mobile C-arm machines

- 3.2.1.4 Rising demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with mobile C-arm machines

- 3.2.2.2 Dearth of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of Manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to Consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of Manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Detector Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Flat panel detector (FPD) C-arms

- 5.2.1 Type

- 5.2.1.1 Amorphous silicon (a-Si) detectors

- 5.2.1.2 Indium gallium zinc oxide (IGZO) detectors

- 5.2.1.3 Complementary metal-oxide semiconductor (CMOS) detectors

- 5.2.2 Size

- 5.2.2.1 20 cm × 20 cm

- 5.2.2.2 26 cm × 26 cm

- 5.2.2.3 30 cm x 30 cm

- 5.2.2.4 Other sizes

- 5.2.1 Type

- 5.3 Image intensifier C-arms

Chapter 6 Market Estimates and Forecast, By Power Output, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Low-powered C-arms (2kW - 10kW)

- 6.3 High-powered C-arms (11kW – 25kW)

Chapter 7 Market Estimates and Forecast, By Design Configuration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Integrated systems

- 7.3 Separate configuration systems

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Orthopedics and trauma

- 8.3 Cardiology

- 8.4 Neurology

- 8.5 Gastroenterology

- 8.6 Oncology

- 8.7 Dental

- 8.8 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Diagnostic centers

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Fujifilm Holdings Corporation

- 11.2 GE HealthCare Technologies

- 11.3 Genoray Co

- 11.4 Hologic

- 11.5 Koninklijke Philips

- 11.6 Nanjing Perlove Medical Equipment Co

- 11.7 Shimadzu Corporation

- 11.8 Siemens Healthineers

- 11.9 SternMed

- 11.10 Stephanix

- 11.11 Turner Imaging Systems

- 11.12 Ziehm Imaging

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日