バイオコハク酸の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Bio-Succinic Acid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750434

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

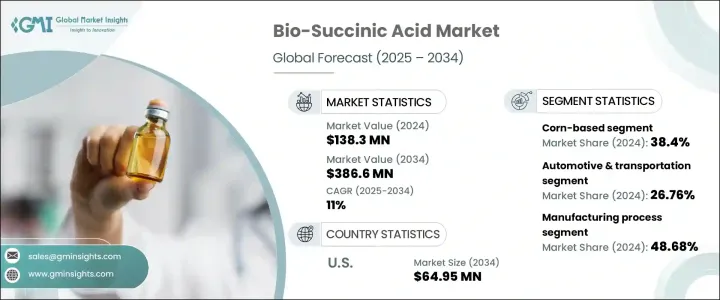

バイオコハク酸の世界市場は、2024年には1億3,830万米ドルとなり、2034年にはCAGR 11%で成長し3億8,660万米ドルに達すると推定されています。

産業界も政府も環境に優しい解決策を重視する中、バイオコハク酸は様々な用途で再生可能かつ生分解性の選択肢を提供するグリーン製品として支持を集めています。持続可能性が重視されるようになり、環境への影響に関する規制も厳しくなったことで、バイオコハク酸は化学業界において重要な役割を果たすようになりました。

バイオコハク酸は、バイオベースのポリマーを製造する際の重要な構成要素であるため、様々な産業で持続可能な材料へのシフトが進んでいることが、バイオコハク酸の需要を大きく押し上げています。こうしたポリマーの中でも、ポリブチレンサクシネート(PBS)は、その生分解性、汎用性、多くの用途で石油ベースのプラスチックに取って代わる可能性から、際立っています。PBSやその他の環境に優しいポリマーの生産に使用されるため、このようなPBSの需要の急増がバイオコハク酸のニーズを促進し、バイオコハク酸の市場をさらに拡大しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1億3,830万米ドル |

| 予測金額 | 3億8,660万米ドル |

| CAGR | 11% |

トウモロコシ分野のバイオコハク酸市場は、2024年に38.4%のシェアを占めました。トウモロコシは炭水化物が豊富な資源であるため、バイオコハク酸を生産する発酵ベースのプロセスに特に適しています。その入手可能性、費用対効果、安定した信頼できる供給能力により、大規模生産に好ましい原料となっています。トウモロコシを原料とするバイオコハク酸の採用が拡大しているのは、その確立されたサプライチェーンと発酵技術の拡張性によるものです。バイオコハク酸の需要が拡大するにつれ、代替原料の検討も行われています。

発酵ベースのプロセスセグメントは、その費用対効果と再生可能原料への依存性により49%のシェアを占めています。この方法は、環境への影響を低減したスケーラブルな生産を可能にするため、大規模製造に適した選択肢となっています。しかし、グルコースや糖類からの直接合成のような新しいアプローチが台頭してきており、制御された条件下でより高い収率を提供しています。化学触媒も注目されているが、コストが高く、環境への影響も懸念されるため、普及には限界があります。発酵と触媒反応を組み合わせたハイブリッド・プロセスは、コストとのバランスを取りながら生産効率と持続可能性を向上させるソリューションとして模索されています。

米国バイオコハク酸米国市場は2024年に2,238万米ドルを生み出し、2034年には6,495万米ドルに達すると予測されています。米国はバイオコハク酸の主要生産国であり、高度な製造インフラとグリーン技術に対する政府の強力な支援の恩恵を受けています。

バイオコハク酸世界市場の主要プレーヤーは、Corbion N.V.、川崎化成工業、BASF SE、三井物産、Reverdiaなどです。各社は市場シェアを拡大するため、製品ポートフォリオの拡大、生産効率の向上、新規原料の開拓に注力しています。例えば、Corbion N.V.とReverdiaは、収率を最適化しコストを削減するために高度な発酵プロセスを活用しており、三井物産は生産に農業廃棄物のような再生可能原料の使用を模索しています。こうした戦略を採用することで、これらの企業は、産業界がより持続可能な解決策へと向かう中、バイオコハク酸に対する需要の高まりに資本投下できる体制を整えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

注:上記の貿易統計は主要国についてのみ提供されます

- 利益率分析

- 規制情勢

- 影響要因

- 促進要因

- バイオベースの化学物質と持続可能な代替品の需要の高まり

- 持続可能で環境に優しい製品に対する消費者の強い好み

- 環境に優しく生分解性のある製品を促進する政府規制

- 業界の潜在的リスク&課題

- 石油由来の代替品に比べて生産コストが高め

- 原材料の入手が限られており、拡張性に影響している

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:原材料別、2021 –2034

- 主要動向

- トウモロコシベース

- サトウキビベース

- キャッサバベース

- リグノセルロース系バイオマス(木材、農業廃棄物など)

- その他(藻類、微生物発酵など)

第6章 市場推計・予測:最終用途産業別、2021 –2034

- 主要動向

- 自動車・輸送

- 包装業界

- 繊維産業

- 建設・インフラ

- 消費財

- ヘルスケアと医薬品

- 農業

- エネルギー部門

第7章 市場推計・予測:製造工程別、2021 –2034

- 主要動向

- 発酵ベースの生産

- グルコースと糖からの直接合成

- 化学触媒

- ハイブリッドプロセス(発酵と触媒の組み合わせ)

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- AHB Global

- BASF SE

- Corbion N.V.

- Kawasaki Kasei Chemicals

- Mitsubishi Chemical Corporation

- Mitsui &Co.、Ltd

- Myriant Corporation

- Nippon Shokubai

- Reverdia

- Roquette Freres

目次

The Global Bio-Succinic Acid Market was valued at USD 138.3 million in 2024 and is estimated to grow at a CAGR of 11% to reach USD 386.6 million by 2034, driven by a rising consumer demand for sustainable, bio-based chemical alternatives to traditional petroleum-based products. As industries and governments alike focus on eco-friendly solutions, bio-succinic acid has gained traction as a green product, offering a renewable and biodegradable option in various applications. The increased emphasis on sustainability, coupled with stricter regulations on environmental impact, has made bio-succinic acid a key player in the chemical industry.

The increasing shift towards sustainable materials in various industries has significantly bolstered the demand for bio-succinic acid, as it is a key building block in the production of bio-based polymers. Among these polymers, polybutylene succinate (PBS) stands out due to its biodegradability, versatility, and potential to replace petroleum-based plastics in numerous applications. This surge in demand for PBS is driving the need for bio-succinic acid, as it is used in the production of PBS and other environmentally friendly polymers, further expanding the market for bio-succinic acid.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $138.3 Million |

| Forecast Value | $386.6 Million |

| CAGR | 11% |

The bio-succinic acid market from the corn segment held 38.4% share in 2024. Corn, being a carbohydrate-rich resource, is particularly well-suited for fermentation-based processes that yield bio-succinic acid. Its availability, cost-effectiveness, and ability to provide a consistent and reliable supply make it a preferred feedstock for large-scale production. The growing adoption of corn-based bio-succinic acid is driven by its established supply chain and the scalability of fermentation technologies. As demand for bio-succinic acid grows, alternative feedstocks are also being explored.

The fermentation-based process segment held 49% share due to its cost-effectiveness and reliance on renewable feedstocks. This method allows for scalable production with reduced environmental impact, making it the preferred choice for large-scale manufacturing. However, new approaches, such as direct synthesis from glucose and sugars, are emerging, offering higher yields under controlled conditions. Chemical catalysis is also gaining attention, although its higher costs and environmental concerns limit its widespread application. The hybrid process, combining fermentation and catalysis, is being explored as a solution to improve production efficiency and sustainability while balancing cost.

U.S Bio-Succinic Acid Market generated USD 22.38 million in 2024, with projections to reach USD 64.95 million by 2034, attributed to government incentives supporting bio-based chemicals and the growing industrial demand for renewable resources. The U.S. is a major producer of bio-succinic acid, benefiting from an advanced manufacturing infrastructure and strong governmental support for green technologies.

Key players in the Global Bio-Succinic Acid Market include Corbion N.V., Kawasaki Kasei Chemicals, BASF SE, Mitsui & Co., Ltd., and Reverdia. Companies are focusing on expanding their product portfolios, improving production efficiency, and exploring new raw materials to enhance their market share. For instance, Corbion N.V. and Reverdia have been leveraging advanced fermentation processes to optimize yields and reduce costs, while Mitsui & Co., Ltd. is exploring the use of renewable raw materials like agricultural waste for production. By adopting these strategies, these companies are positioning themselves to capitalize on the growing demand for bio-succinic acid as industries move toward more sustainable solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.3 Supply-side impact (raw materials)

- 3.2.3.1 Price volatility in key materials

- 3.2.3.2 Supply chain restructuring

- 3.2.3.3 Production cost implications

- 3.2.4 Demand-side impact (selling price)

- 3.2.4.1 Price transmission to end markets

- 3.2.4.2 Market share dynamics

- 3.2.4.3 Consumer response patterns

- 3.2.5 Key companies impacted

- 3.2.6 Strategic Industry Responses

- 3.2.6.1 Supply Chain Reconfiguration

- 3.2.6.2 Pricing and Product Strategies

- 3.2.6.3 Policy Engagement

- 3.2.7 Outlook and Future Considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major Exporting Countries

- 3.3.2 Major Importing Countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for bio-based chemicals and sustainable alternatives

- 3.6.1.2 Strong consumer preference for sustainable and green products

- 3.6.1.3 Government regulations promoting eco-friendly and biodegradable products

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs compared to petroleum-based alternatives

- 3.6.2.2 Limited availability of raw materials, affecting scalability

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Raw Material Source, 2021 – 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Corn-based

- 5.3 Sugarcane-based

- 5.4 Cassava-based

- 5.5 Lignocellulosic biomass (wood, agricultural waste, etc.)

- 5.6 Others (algae, microbial fermentation, etc.)

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Automotive & transportation

- 6.3 Packaging industry

- 6.4 Textile industry

- 6.5 Construction & infrastructure

- 6.6 Consumer goods

- 6.7 Healthcare & pharmaceuticals

- 6.8 Agriculture

- 6.9 Energy sector

Chapter 7 Market Estimates and Forecast, By Manufacturing Process, 2021 – 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Fermentation-based production

- 7.3 Direct synthesis from glucose & sugars

- 7.4 Chemical catalysis

- 7.5 Hybrid process (combination of fermentation & catalysis)

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AHB Global

- 9.2 BASF SE

- 9.3 Corbion N.V.

- 9.4 Kawasaki Kasei Chemicals

- 9.5 Mitsubishi Chemical Corporation

- 9.6 Mitsui & Co., Ltd

- 9.7 Myriant Corporation

- 9.8 Nippon Shokubai

- 9.9 Reverdia

- 9.10 Roquette Freres

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日