|

市場調査レポート

商品コード

1750413

建築用コーティング剤、エナメル、プライマー、ステイン、溶剤、ラッカーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Architectural Coatings, Enamels, Primers, Stains, Solvents, and Lacquers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 建築用コーティング剤、エナメル、プライマー、ステイン、溶剤、ラッカーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月06日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

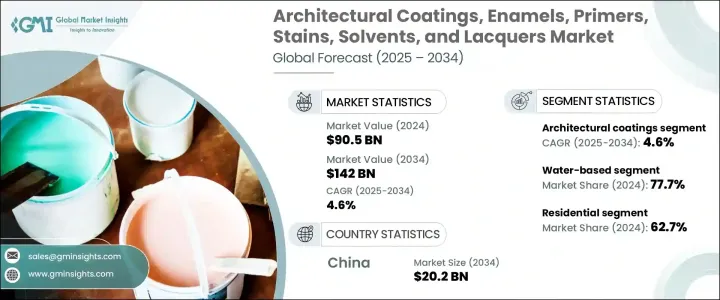

世界の建築用コーティング剤、エナメル、プライマー、ステイン、溶剤、ラッカー市場は、2024年には905億米ドルと評価され、エナメル、プライマー、ステイン、溶剤、ラッカーが様々な産業で特定の美的・機能的ニーズに応えることから、CAGR 4.6%で成長し、2034年には1,420億米ドルに達すると推定されます。

市場の成長は、特に新興諸国における急速な都市化と、成熟市場における改築やメンテナンス活動の増加が主な要因となっています。環境に優しいソリューションへの需要が高まり続ける中、建築用コーティング剤、エナメル、プライマー、ステイン、溶剤、ラッカー市場は低VOC(揮発性有機化合物)処方へのシフトを目の当たりにしています。持続可能な製品に対する嗜好の高まりは、環境への影響に対する意識の高まりと、室内空気の質に対する消費者の懸念が背景にあります。

さらに、コーティング技術の進歩により、住宅や商業施設によく見られる高湿度や長時間の紫外線暴露といった過酷な条件下での性能が向上しています。このような技術革新により、コーティングの適用範囲が拡大し、耐用年数や耐久性が向上しているため、消費者と業界関係者の双方にとって、コーティングはより魅力的なものとなっています。これらの地域では、都市部への移住者が増えるにつれて、新しい住宅や商業施設、公共インフラに対するニーズが高まっており、これらすべてが高品質の塗料に対する需要を後押ししています。アジア太平洋地域は建設と改修プロジェクトに重点を置いており、近代的で持続可能な生活への文化的変化と相まって、建築用コーティング剤の世界の急成長市場となっています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 905億米ドル |

| 予測金額 | 1,420億米ドル |

| CAGR | 4.6% |

建築用コーティング分野は、2024年に905億米ドルを生み出し、住宅と商業施設の両方で広く使用されているため、今後も拡大が続くと予測されます。これらの塗料は美観だけでなく、表面を摩耗や湿気、環境要因から保護する能力も評価されています。政府も消費者も持続可能性を優先しているため、環境に優しいとされる水性塗料や低VOC塗料の需要は特に強いです。さらに、速乾性で多面性を持つ塗料の技術革新は、利便性と性能の両方を提供するこれらの製品への嗜好の高まりに寄与しています。

住宅分野は2024年に62.7%のシェアを占めました。この動向の背景には、アジア太平洋地域を中心とした新興国における住宅需要の拡大があります。さらに、消費者の嗜好は進化しており、耐久性と環境に配慮した汎用性の高い高性能塗料への注目が高まっています。様々な表面に塗布できる多機能塗料のような、審美的な汎用性を向上させた塗料への需要は高まり続けており、住宅分野の成長をさらに後押ししています。都市部の住宅建設が、特に急速に開発が進む地域で加速するにつれて、持続可能で革新的な塗料へのニーズが高まり、業界関係者に新たなビジネスチャンスが生まれると予想されます。

中国の建築用コーティング剤、エナメル、プライマー、ステイン、溶剤、ラッカー2024年の市場規模は126億米ドルで、これは主に同国の急速な都市開拓によるものです。特にTier-2およびTier-3都市における消費の増加が、性能と美観を向上させたコーティング剤の需要を促進しています。消費者の嗜好が進化するにつれて、セルフクリーニングや抗菌性を含むプレミアム・コーティングの市場が拡大しています。各社は製品のイノベーションと流通網の拡大に注力し、この競争の激しい市場でより大きなシェアを獲得することを目指しています。

Sherwin-Williams、PPG Industries、AkzoNobel、Asian Paintsなど、建築用コーティング剤、エナメル、プライマー、ステイン、溶剤、ラッカー市場の主要企業は、市場シェアを強化するためにM&Aなどの戦略を採用しています。製品の革新もまた主要な焦点であり、これらの企業は変化する消費者ニーズに対応する新しいソリューションを導入するため、研究開発に多額の投資を行っています。さらに、戦略的パートナーシップや流通網の改善も、特に中国やインドといった急成長市場における企業のプレゼンス強化に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税の影響- 構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

注:上記の貿易統計は主要国についてのみ提供されます

- サプライヤーの情勢

- 利益率分析

- 規制情勢

- 影響要因

- 促進要因

- 住宅および商業建設活動の急増

- 環境に優しくVOC排出量が少ない製品への需要の高まり

- 処方と適用効率における技術革新

- 業界の潜在的リスク&課題

- 原材料費と投入コストの変動

- 溶剤系製品に対する規制圧力

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 建築用コーティング

- エナメル

- プライマー

- 汚れ

- 溶剤

- ラッカー

第6章 市場推計・予測:技術別、2021-2034

- 主要動向

- 水性

- 溶剤ベース

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 住宅用

- 商業用

- 産業用

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- AkzoNobel

- Asian Paints Limited

- Axalta Coating Systems

- BASF Coatings

- Benjamin Moore &Co.

- Hempel

- Jotun Group

- Kansai Paint

- Masco Corporation

- Nippon Paint Holdings

- PPG Industries

- RPM International

- Sherwin-Williams Company

- Tikkurila Oyj

The Global Architectural Coatings, Enamels, Primers, Stains, Solvents, and Lacquers Market was valued at USD 90.5 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 142 billion by 2034 as enamels, primers, stains, solvents, and lacquers, cater to specific aesthetic and functional needs across various industries. The market growth is largely driven by rapid urbanization, particularly in developing countries, and increased renovation and maintenance activities in mature markets. As the demand for eco-friendly solutions continues to rise, the architectural coatings, enamels, primers, stains, solvents, and lacquers market is witnessing a shift towards low-VOC (volatile organic compound) formulations. This growing preference for sustainable products is driven by increasing awareness of environmental impact and consumer concerns about indoor air quality.

Moreover, advancements in coating technologies have enhanced performance under extreme conditions, such as high humidity and prolonged UV exposure, which are common in both residential and commercial buildings. These innovations are expanding the range of applications and improving the longevity and durability of coatings, making them more attractive to both consumers and industry professionals. As more people in these regions migrate to urban areas, there is a corresponding need for new housing, commercial spaces, and public infrastructure, all of which drive demand for high-quality coatings. The region's focus on construction and renovation projects, paired with a cultural shift towards modern, sustainable living, positions Asia-Pacific as the fastest-growing market for architectural coatings globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $90.5 Billion |

| Forecast Value | $142 Billion |

| CAGR | 4.6% |

The architectural coatings segment generated USD 90.5 billion in 2024, and it is projected to continue its expansion due to its widespread use in both residential and commercial buildings. These coatings are valued not only for their aesthetic appeal but also for their ability to protect surfaces from wear, moisture, and environmental factors. The demand for water-based and low-VOC coatings, which are considered more eco-friendly, is particularly strong, as governments and consumers alike prioritize sustainability. Additionally, innovations in fast-drying, multi-surface paints have contributed to an increased preference for these products, offering both convenience and performance.

The residential segment held a 62.7% share in 2024. The expanding demand for housing in emerging economies, particularly in the Asia-Pacific region, is a key factor behind this trend. Furthermore, consumer preferences are evolving, with a stronger focus on versatile, high-performance coatings that are both durable and eco-friendly. The demand for coatings with improved aesthetic versatility, such as multi-functional paints that can be applied to various surfaces, continues to rise, further fueling growth in the residential sector. As urban housing construction accelerates, particularly in rapidly developing regions, the need for sustainable and innovative coatings is expected to grow, creating new opportunities for industry players.

China Architectural Coatings, Enamels, Primers, Stains, Solvents, and Lacquers Market generated USD 12.6 billion in 2024, largely due to the country's rapid urban development. Increased consumption, particularly in tier-2 and tier-3 cities, is fueling demand for coatings with enhanced performance and aesthetic appeal. The market for premium coatings, including those with self-cleaning or antibacterial properties, is growing as consumer preferences evolve. Companies are responding by focusing on product innovation and expanding their distribution networks, aiming to capture a larger share of this highly competitive market.

Leading companies in Architectural Coatings, Enamels, Primers, Stains, Solvents, and Lacquers Market, including Sherwin-Williams, PPG Industries, AkzoNobel, and Asian Paints, are adopting strategies such as mergers and acquisitions to consolidate market share. Product innovation is also a key focus, with these companies investing heavily in research and development to introduce new solutions that meet changing consumer needs. Additionally, strategic partnerships and improved distribution networks are helping companies strengthen their presence, particularly in rapidly growing markets like China and India.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact of trump administration tariffs - structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

note: the above trade statistics will be provided for key countries only.

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Surge in residential and commercial construction activity

- 3.7.1.2 Rising demand for eco-friendly and low-voc products

- 3.7.1.3 Technological innovation in formulations and application efficiency

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Volatile raw material and input costs

- 3.7.2.2 Regulatory pressure on solvent-based products

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Architectural coatings

- 5.3 Enamels

- 5.4 Primers

- 5.5 Stains

- 5.6 Solvents

- 5.7 Lacquers

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Water-based

- 6.3 Solvent-based

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Residenial

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 AkzoNobel

- 9.2 Asian Paints Limited

- 9.3 Axalta Coating Systems

- 9.4 BASF Coatings

- 9.5 Benjamin Moore & Co.

- 9.6 Hempel

- 9.7 Jotun Group

- 9.8 Kansai Paint

- 9.9 Masco Corporation

- 9.10 Nippon Paint Holdings

- 9.11 PPG Industries

- 9.12 RPM International

- 9.13 Sherwin-Williams Company

- 9.14 Tikkurila Oyj