|

市場調査レポート

商品コード

1750353

ポリケトンの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Polyketone (PK) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ポリケトンの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月06日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

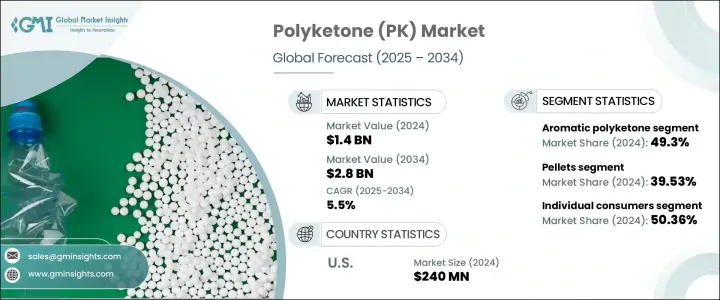

ポリケトンの世界市場は2024年に14億米ドルと評価され、いくつかの産業で高性能ポリマーの需要が増加しているため、CAGR 5.5%で成長し、2034年には28億米ドルに達すると推定されます。

この成長は、優れた耐薬品性、低吸湿性、改良された摩耗特性を提供する高度な代替材料の探索によって大きく後押しされています。ポリケトンはこうした特性から、ポリアミドやポリオキシメチレンといった従来の材料に代わる競争力のある材料として位置づけられています。ポリケトンの用途は、特に厳しい性能や規制基準を満たす材料を必要とする分野で拡大し続けています。環境意識の高まりと、軽量で燃費の良いソリューションの推進が、ポリケトンの採用を後押ししています。

ポリケトンの市場実績は、特に耐久性と耐薬品性が要求される分野で好調です。PKのような軽量ポリマーは、燃料システムや自動車構造部品のような高ストレス環境での使用が増加しています。ポリケトンは、製品性能を向上させ、自動車全体の重量を減らすと同時に、メーカーが厳しい排ガス規制を満たすのに役立っています。ポリケトンは過酷な条件下でも機械的強度を維持することができるため、特に燃料や潤滑油、高温にさらされることが多い場所では、従来のエンジニアリング・プラスチックに代わる貴重な選択肢となります。この材料は、ペレット、繊維、シート、フィルムなど様々な形状に適応できるため、エレクトロニクス、消費財、運輸などの産業でその魅力をさらに広げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 14億米ドル |

| 予測金額 | 28億米ドル |

| CAGR | 5.5% |

ペレットセグメントは、加工が容易で押出成形や射出成形などの標準的な製造技術に適合することから、2024年には39.53%のシェアを占めました。均一性、低吸湿性、優れた寸法安定性により、複雑な部品の精密な製造が可能です。さらに、過酷な化学物質や炭化水素に対する耐性が強いため、過酷な環境にさらされる部品に適しています。このような利点により、ペレットは、性能、安全性、規制への準拠が譲れない自動車のような要求の厳しい分野で、最適な形状となっています。

一方、環境に優しい代替品に対する消費者の意識が、個人消費者セグメントでの需要を押し上げ、2024年には50.36%のシェアを占める。人々は日常製品に持続可能な素材を求める傾向にあり、この傾向はポリケトンのリサイクル可能で環境に配慮した特性とよく合致しています。消費者の考え方の変化は、グリーン製品の販売を促進するだけでなく、企業が高性能の持続可能なポリマーを使って既存の製品を改良することを促しています。このシフトは、スポーツ用品、ウェアラブル・テクノロジー、キッチン用品、身の回りのアクセサリーなど、耐久性や機能に妥協することなく、環境に配慮したデザインをユーザーが求めるアイテムの生産において、ポリケトンに新たな可能性をもたらしました。

米国のポリケトン(PK)市場は2024年に2億4,000万米ドルと評価され、強固な産業枠組み、イノベーション重視の市場開拓、先端材料への高い需要に支えられて急成長を続けています。北米は、エレクトロニクス、航空宇宙、自動車セクターの活発な活動により、PK用途の主要拠点であり続けています。持続可能な技術と先端ポリマー科学を重視する地域性は、この地域におけるポリケトンの存在感を強化する上で重要な役割を果たしています。

ポリケトン(PK)業界の企業としては、Nexeo Plastics、Ensinger、HYOSUNG、MITSUI PLASTICS、Avientなどが挙げられます。市場においてより強固な地位を確保するため、各社は研究開発に多額の投資を行い、製品のイノベーションと応用分野の拡大に注力しています。自動車やエレクトロニクス分野のメーカーとの戦略的パートナーシップは、商業的な採用を後押しします。企業はまた、サプライチェーンの効率を改善し、持続可能な製造プロセスを導入しています。カスタムグレードを開発し、製品ポートフォリオを多様化することで、進化するエンドユーザーのニーズに対応し、長期的な競争力を強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

注:上記の貿易統計は主要国についてのみ提供されます

- 規制情勢

- 影響要因

- 促進要因

- 自動車業界の需要増加

- 電気自動車(EV)と持続可能なモビリティの台頭

- 高性能材料の需要増加

- 業界の潜在的リスク&課題

- 高い生産コスト

- 規制と環境に関する懸念

- 促進要因

- 政策関与

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 芳香族ポリケトン

- 脂肪族ポリケトン

- 共重合体ポリケトン

第6章 市場推計・予測:形態別、2021-2034

- 主要動向

- ペレット

- ファイバー

- フィルム

- シート

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 自動車部品

- 電気・電子工学

- 産業機械

- 消費財

- コーティング剤と接着剤

- 医療機器

- 包装

- その他

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- AKRO-PLASTIC

- Avient

- Distrupol

- Ensinger

- HYOSUNG

- K.D. Feddersen

- LEHVOSS

- MITSUI PLASTICS

- Nexeo Plastics

- POLYOLS &POLYMERS

- Rochling

- Specialist Engineering Plastics

- Technoform

The Global Polyketone Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 2.8 billion by 2034 due to increasing demand for high-performance polymers across several industries. This growth is largely fueled by the search for advanced material alternatives that offer superior chemical resistance, low moisture absorption, and improved wear properties. These characteristics position polyketones as a competitive substitute for traditional materials like polyamides and polyoxymethylene. Their applications continue to expand, especially in sectors requiring materials that meet stringent performance and regulatory standards. Rising environmental consciousness and the push for lightweight, fuel-efficient solutions drive adoption.

Polyketone's market performance has been strong, particularly in segments that demand durability and chemical resistance. Lightweight polymers like PK are increasingly used in high-stress environments, such as fuel systems and structural automotive components. They help manufacturers meet strict emissions standards while improving product performance and reducing overall vehicle weight. Polyketone's ability to maintain mechanical strength under extreme conditions makes it a valuable alternative to conventional engineering plastics, especially where exposure to fuels, lubricants, and high temperatures is common. The material's adaptability in various forms-like pellets, fibers, sheets, and films-has further widened its appeal across industries, including electronics, consumer goods, and transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 5.5% |

The pellets segment accounted for 39.53% share in 2024 due to their ease of processing and compatibility with standard manufacturing techniques such as extrusion and injection molding. Their uniformity, low moisture absorption, and excellent dimensional stability allow precision in manufacturing complex parts. Additionally, their strong resistance to harsh chemicals and hydrocarbons makes them a preferred choice for components exposed to aggressive environments. These advantages make pellets the go-to form in demanding sectors like automotive, where performance, safety, and compliance with regulations are non-negotiable.

Meanwhile, consumer awareness of eco-friendly alternatives has pushed demand within the individual consumer segment, representing a 50.36% share in 2024. People lean toward sustainable materials in everyday products, a trend that aligns well with polyketone's recyclable and environmentally conscious profile. The shift in consumer mindset is not only driving sales of green products but also encouraging companies to reformulate existing goods using high-performance sustainable polymers. This shift has opened new opportunities for polyketone in the production of items such as sporting goods, wearable tech, kitchenware, and personal accessories-areas where users are now expecting eco-conscious design without compromising on durability or function.

United States Polyketone (PK) Market was valued at USD 240 million in 2024 and continues to grow rapidly, backed by a robust industrial framework, innovation-focused development, and a high demand for advanced materials. North America remains a major hub for PK applications due to strong activity in the electronics, aerospace, and automotive sectors. Local emphasis on sustainable technologies and advanced polymer science plays a significant role in reinforcing polyketone's presence in the region.

The Polyketone (PK) industry players include Nexeo Plastics, Ensinger, HYOSUNG, MITSUI PLASTICS, and Avient. To secure a stronger position in the market, companies are heavily investing in research and development, focusing on product innovations and expanding application areas. Strategic partnerships with manufacturers across the automotive and electronics sectors help boost commercial adoption. Businesses are also improving supply chain efficiency and introducing sustainable manufacturing processes. By developing custom grades and diversifying product portfolios, they're addressing evolving end-user needs and reinforcing long-term competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.3 Supply-side impact (raw materials)

- 3.2.3.1 Price volatility in key materials

- 3.2.3.2 Supply chain restructuring

- 3.2.3.3 Production cost implications

- 3.2.4 Demand-side impact (selling price)

- 3.2.4.1 Price transmission to end markets

- 3.2.4.2 Market share dynamics

- 3.2.4.3 Consumer response patterns

- 3.2.5 Key companies impacted

- 3.2.6 Strategic industry responses

- 3.2.6.1 Supply chain reconfiguration

- 3.2.6.2 Pricing and product strategies

- 3.2.6.3 Policy engagement

- 3.2.7 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Growing demand in the automotive industry

- 3.5.1.2 Rise of electric vehicles (EVs) and sustainable mobility

- 3.5.1.3 Increasing demand for high-performance materials

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 High production costs

- 3.5.2.2 Regulatory & environmental concerns

- 3.5.1 Growth drivers

- 3.6 Policy engagement

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Aromatic polyketone

- 5.3 Aliphatic polyketone

- 5.4 Copolymer polyketone

Chapter 6 Market Estimates and Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Pellets

- 6.3 Fibers

- 6.4 Films

- 6.5 Sheets

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive components

- 7.3 Electrical & electronics

- 7.4 Industrial machinery

- 7.5 Consumer goods

- 7.6 Coatings & adhesives

- 7.7 Medical devices

- 7.8 Packaging

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 AKRO-PLASTIC

- 9.2 Avient

- 9.3 Distrupol

- 9.4 Ensinger

- 9.5 HYOSUNG

- 9.6 K.D. Feddersen

- 9.7 LEHVOSS

- 9.8 MITSUI PLASTICS

- 9.9 Nexeo Plastics

- 9.10 POLYOLS & POLYMERS

- 9.11 Rochling

- 9.12 Specialist Engineering Plastics

- 9.13 Technoform