|

市場調査レポート

商品コード

1750341

変圧器部品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Transformer Component Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 変圧器部品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月16日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

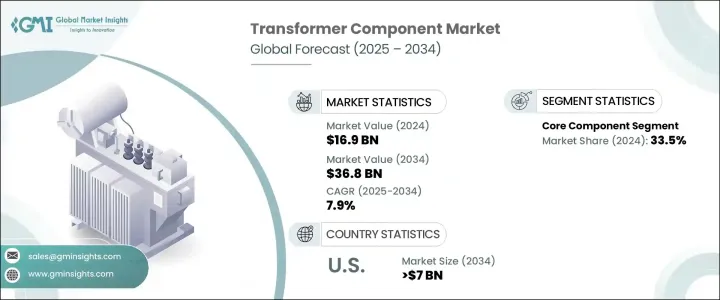

世界の変圧器部品市場は、2024年には169億米ドルと評価され、エネルギー需要の増加に対応するために各国が電力インフラのアップグレードと拡大に多額の投資を行っていることから、CAGR 7.9%で成長し、2034年には368億米ドルに達すると推定されています。

この成長の主な要因は、再生可能エネルギー統合への世界のシフトと新興経済諸国で見られる急速な工業化です。政府と民間部門が送電網の近代化とエネルギーの信頼性向上に向けた取り組みを強化する中、先進変圧器部品に対する需要は増加の一途をたどっています。また、いくつかの地域で電化と都市開拓が進んでいることも、市場の追い風となっています。さらに、技術主導の進歩が変圧器部品の将来を形作り、より効率的でコンパクトな信頼性の高いものとなっています。

産業が発展するにつれ、エネルギー損失の削減、システム性能の向上、持続可能性の確保に重点が置かれ続けています。進展は続いているもの、市場は原材料コストの変動や世界・サプライ・チェーンの混乱に関連する課題に直面しています。これらの要因は、メーカーにとって不安定な環境を作り出しており、メーカーは製品の品質と納期を維持しようとしながら、材料価格の上昇にも対応しています。このような制約がある中でも、競合設計、特にコア構造、断熱材、冷却技術の革新は、各社の競争力維持と需要増への対応に役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 169億米ドル |

| 予測金額 | 368億米ドル |

| CAGR | 7.9% |

アジア太平洋地域は世界の変圧器部品市場において主導的地位を占めており、2034年には115億米ドルを超えると予測されています。この地域の成長は、都市人口の拡大と産業活動の活発化によって、電気インフラへの投資が加速していることと強く結びついています。この地域全体で、送電網の信頼性と容量を強化する取り組みが、変圧器部品への持続的な需要を生み出しています。一方、北米も、老朽化した電力インフラの近代化と再生可能エネルギーの普及拡大に伴い、力強い勢いを見せています。送電網アーキテクチャのアップグレードとスマートグリッドシステムの採用が、安定的かつ効率的なエネルギー配給を支える高性能変圧器部品の必要性を高めています。このような変化により、ユーティリティ企業や電力会社は、運用ロスを削減し、サービスの信頼性を高めることを目的とした新技術の採用を迫られています。

変圧器部品市場では、巻線アセンブリ、タップチェンジャー、絶縁材料、コア構造などの分野で広く改善が見られます。これらの開発は、エネルギー効率が高く、長持ちするシステムへの期待の高まりに直接応えるものです。2024年には、コアコンポーネントセグメントが市場全体の33.5%を占め、2034年までのCAGRは9%を超えると予想されています。この分野は、エネルギー損失を最小限に抑え、性能を最適化するように設計された先端材料の導入により進化を続けています。アモルファス鋼やシリコン系鋼などの材料は、コア損失を減らし、変圧器ユニットの全体的な効率に貢献するために採用されています。

冷却システムにおいては、エネルギーの浪費を減らし、運転の安全性を向上させるために、新しい技術と導電性材料が導入されています。連続転置導体(CTC)のような技術革新は、損失を低減しながら高性能の冷却をサポートする能力によって人気を集めています。これらの進歩は、産業および公益事業ネットワークの増大する電力需要を満たし、電力網の長期的な信頼性を確保するために不可欠です。

米国の変圧器部品市場は、近年一貫した成長を見せています。2022年の市場規模は26億米ドルで、2023年には29億米ドル、2024年には32億米ドルに増加します。2034年には、この数字は70億米ドルを超えると予測されています。この成長の主な要因は、再生可能エネルギーと送電網アップグレードへの投資が増加していることです。スマートグリッドシステムを開発し、エネルギー回復力を強化しようとする動きは、改良された巻線コア、効率的な絶縁材料、最新の部品アセンブリに対する大きな需要を生み出しています。ユーティリティ・プロバイダーや商業事業者は、中断のないサービスと効率的なエネルギーの流れを確保するため、インフラの強化に注力しています。

世界の変圧器部品市場の大手企業は、幅広い製品群と信頼性の高い販売体制により、強力な足場を維持し続けています。2024年には、上位5社合計で市場シェアの35%以上を占める。これらの企業の成功は、エンドツーエンドのソリューションを提供し、ユーティリティプロバイダーと長期的な関係を築き、進化する市場ニーズに対応するための調査と技術革新に継続的に投資する能力に根ざしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 競合情勢

- 企業の市場シェア分析

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:コンポーネントタイプ別、2021年~2034年

- 主要動向

- コア

- 巻き取り

- 断熱システム

- タップチェンジャー

- その他

第6章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第7章 企業プロファイル

- Alamo Transformer Supply Company(ATSCO)

- Amran Inc.

- BHEL

- Eaton

- EIS Legacy、LLC

- ELSCO Transformers

- Emerald Transformer

- ERMCO

- Hitachi Energy

- Howard Industries

- Johnson Bros. Roll Forming Co.

- LCS Company

- Magnetics

- Mapes &Sprowl Steel

- Metglas Inc.

- Power Asset Recovery Corporation

- Renco Electronics

- TC Metal

- Tempel

- The H-J Family of Companies

- Triad Magnetics

- VoltageShift Engineering Solutions LLP

- Von Roll USA

The Global Transformer Component Market was valued at USD 16.9 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 36.8 billion by 2034 as countries invest heavily in upgrading and expanding their power infrastructure to meet rising energy demands. This growth is primarily being fueled by the global shift toward renewable energy integration and the rapid industrialization observed in developing economies. As governments and private sectors intensify efforts to modernize power grids and improve energy reliability, the demand for advanced transformer components continues to rise. The market is also benefiting from increasing electrification and urban development across several regions. Furthermore, technology-driven advancements are shaping the future of transformer components, making them more efficient, compact, and reliable.

As the industry evolves, the focus remains on reducing energy losses, enhancing system performance, and ensuring sustainability. Despite ongoing progress, the market is facing challenges related to raw material cost fluctuations and disruptions in global supply chains. These factors are creating a volatile environment for manufacturers, who are also navigating rising material prices while trying to maintain product quality and delivery timelines. Even with these constraints, innovation in component design, particularly in core construction, insulation, and cooling technologies, is helping companies stay competitive and meet growing demand.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.9 Billion |

| Forecast Value | $36.8 Billion |

| CAGR | 7.9% |

Asia Pacific holds the leading position in the global transformer component market and is projected to exceed USD 11.5 billion by 2034. The region's growth is strongly tied to accelerating investments in electrical infrastructure, driven by expanding urban populations and increased industrial activity. Across this region, efforts to enhance grid reliability and capacity are generating sustained demand for transformer components. Meanwhile, North America is also witnessing strong momentum as the region modernizes its aging power infrastructure and expands its renewable energy footprint. Upgrades in grid architecture and the adoption of smart grid systems are boosting the need for high-performance transformer components that can support stable and efficient energy distribution. These changes are pushing utilities and power companies to adopt new technologies aimed at reducing operational losses and enhancing service reliability.

The transformer component market is seeing widespread improvements in areas such as winding assemblies, tap changers, insulation materials, and core structures. These developments are a direct response to growing expectations for energy-efficient and long-lasting systems. In 2024, the core component segment accounted for 33.5% of the overall market and is expected to grow at a CAGR exceeding 9% through 2034. This segment continues to evolve with the introduction of advanced materials that are designed to minimize energy losses and optimize performance. Materials such as amorphous and silicon-based steels are being adopted to reduce core losses and contribute to the overall efficiency of transformer units.

In cooling systems, new technologies and conductive materials are being introduced to reduce energy waste and improve operational safety. Innovations like Continuous Transposed Conductors (CTC) are gaining popularity due to their ability to support high-performance cooling while lowering losses. These advancements are critical for meeting the growing power demands of industrial and utility networks and for ensuring the long-term reliability of the electrical grid.

The transformer component market in the United States has shown consistent growth over recent years. In 2022, the market was valued at USD 2.6 billion, rising to USD 2.9 billion in 2023 and USD 3.2 billion in 2024. By 2034, this figure is projected to surpass USD 7 billion. This growth is largely attributed to the nation's increasing investment in renewable energy and grid upgrade initiatives. The push to develop smart grid systems and enhance energy resilience is generating significant demand for improved winding cores, efficient insulation materials, and modern component assemblies. Utility providers and commercial operators are focusing on strengthening infrastructure to ensure uninterrupted service and efficient energy flow.

Leading players in the global transformer component market continue to maintain a strong foothold due to their broad product offerings and reliable distribution frameworks. In 2024, the top five companies collectively held over 35% of the market share. Their success is rooted in their ability to provide end-to-end solutions, foster long-term relationships with utility providers, and continually invest in research and innovation to meet evolving market needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Competitive landscape, 2025

- 4.2 Company market share analysis

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Component Type, 2021 – 2034 (‘000 Units, USD Million)

- 5.1 Key trends

- 5.2 Core

- 5.3 Winding

- 5.4 Insulation system

- 5.5 Tap changers

- 5.6 Others

Chapter 6 Market Size and Forecast, By Region, 2021 – 2034 (‘000 Units, USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 France

- 6.3.3 Russia

- 6.3.4 UK

- 6.3.5 Italy

- 6.3.6 Spain

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 South Korea

- 6.4.4 India

- 6.4.5 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 Qatar

- 6.5.4 Egypt

- 6.5.5 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

Chapter 7 Company Profiles

- 7.1 Alamo Transformer Supply Company (ATSCO)

- 7.2 Amran Inc.

- 7.3 BHEL

- 7.4 Eaton

- 7.5 EIS Legacy, LLC

- 7.6 ELSCO Transformers

- 7.7 Emerald Transformer

- 7.8 ERMCO

- 7.9 Hitachi Energy

- 7.10 Howard Industries

- 7.11 Johnson Bros. Roll Forming Co.

- 7.12 LCS Company

- 7.13 Magnetics

- 7.14 Mapes & Sprowl Steel

- 7.15 Metglas Inc.

- 7.16 Power Asset Recovery Corporation

- 7.17 Renco Electronics

- 7.18 TC Metal

- 7.19 Tempel

- 7.20 The H-J Family of Companies

- 7.21 Triad Magnetics

- 7.22 VoltageShift Engineering Solutions LLP

- 7.23 Von Roll USA