ニチノールベースの医療機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Nitinol-based Medical Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750337

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

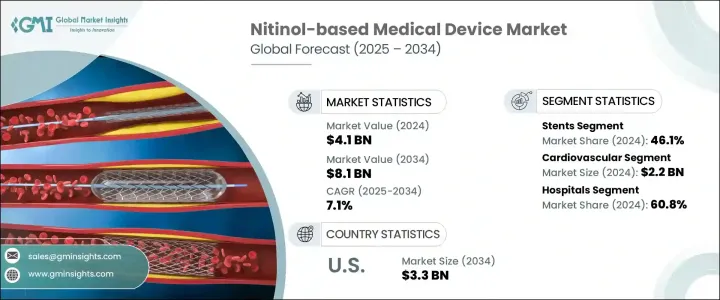

ニチノールベースの医療機器の世界市場は、2024年には41億米ドルと評価され、高度で低侵襲な医療介入が必要とされる心血管疾患、末梢動脈疾患、神経疾患などの慢性疾患の有病率の増加に牽引され、CAGR 7.1%で成長し、2034年には81億米ドルに達すると推定されています。

ニチノールは、超弾性と形状記憶というユニークな特性で知られるニッケルチタン合金で、患者の予後を改善するために医療機器への利用が増加しています。

ニチノールは、変形後に所定の形状に戻る能力と、機械的応力に対する耐性により、様々な医療用途に理想的です。これらの特性は、柔軟性と耐久性が重要なステント、ガイドワイヤー、整形外科用インプラントなどの機器において特に有益です。この材料の生体適合性と耐食性は、長期的な移植への適性をさらに高めます。これらの特性により、ニチノール製器具は長期間にわたって人体内で機能性と構造的完全性を維持し、拒絶反応や劣化のリスクを低減します。この信頼性により、ニチノールは心臓血管、神経血管、整形外科治療で使用される永久インプラントとして好ましい選択肢となっています。低侵襲処置の需要が高まるにつれ、ニチノールベースの器具の採用が増加し、市場の拡大に寄与すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 41億米ドル |

| 予測金額 | 81億米ドル |

| CAGR | 7.1% |

2024年の病院セグメントのシェアは60.8%で、手術時間の短縮、患者の外傷の最小化、回復結果の改善を目的とした先進医療機器の導入が増加していることが背景にあります。ステント、ガイドワイヤー、フィルター、整形外科用インプラントなど、ニチノールをベースとする器具は、形状記憶や超弾性といった独自の特性により病院に不可欠なものとなっています。特に心臓血管や神経血管の手技において、複雑な解剖学的構造をナビゲートするステントの優れた性能は、手技の成功率の向上と入院期間の短縮につながります。

2024年には、血管障害の有病率の上昇とニチノールステントが提供する臨床的利点に後押しされ、ステント部門は46.1%のシェアでトップの座を維持しました。これらのステントは、特に末梢動脈疾患や冠動脈閉塞の患者において、自己拡張性と複雑な血管経路にシームレスに適合する能力が評価されています。特に末梢動脈疾患や冠動脈閉塞の患者において、これらのステントは複雑な血管経路にシームレスに適合する能力が評価されています。ヘルスケアプロバイダーが動脈疾患管理のために侵襲性が低く、効果の高い治療オプションを優先しているため、需要は増加し続けています。

北米のニチノールベースの医療機器2024年の市場シェアは40%を占めたが、これは同地域の強固なヘルスケア・インフラ、確立された償還制度、先進医療技術の早期導入に起因しています。大手メーカーの存在と、病院や専門クリニックにおけるニチノールベースのツールの広範な臨床的統合が、急速に進化するこの医療機器分野における北米の牙城をさらに強固なものにしています。

世界のニチノールベースの医療機器業界の主要企業には、Boston Scientific Corporation、Medtronic plc、Abbott Laboratories、Terumo Corporation、B. Braun Melsungen AGなどがあります。これらの企業は、ニチノールベースのデバイスの革新と性能向上のための研究開発に注力しています。戦略的提携、合併、買収は、各社が製品ポートフォリオと市場範囲の拡大を目指す中で一般的に行われています。市場ポジションを強化するため、ニチノールベースの医療機器業界の企業はいくつかの重要な戦略を採用しています。これには、ニチノールをベースとしたデバイスの革新と性能向上のための研究開発への投資が含まれます。戦略的提携、合併、買収は、企業が製品ポートフォリオと市場リーチを拡大することを目的としているため、一般的です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 低侵襲手術の需要増加

- 心血管疾患および整形外科疾患の有病率の上昇

- 医療機器製造における技術の進歩

- 世界的に高齢化が進む

- 業界の潜在的リスク&課題

- ニチノールベースのデバイスの高コスト

- 厳格な規制承認プロセス

- 促進要因

- 成長可能性分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項トランプ政権の関税

- 貿易への影響

- テクノロジーの情勢

- 将来の市場動向

- 規制情勢

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 競争市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ステント

- ガイドワイヤー

- カテーテル

- その他の製品

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 心血管系

- 整形外科

- 歯科

- 神経学的

- 泌尿器科

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

- 研究・学術機関

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- Acandis

- Admedes Schuessler

- Arthrex

- B Braun

- Becton、Dickinson and Company

- Biotronik

- Boston Scientific

- Cook Medical

- Endosmart

- Jotec

- Medtronic

- MicroPort

- Stryker

- Terumo

目次

The Global Nitinol-based Medical Device Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 8.1 billion by 2034 driven by the increasing prevalence of chronic diseases such as cardiovascular conditions, peripheral artery disease, and neurological disorders, which necessitate advanced, minimally invasive medical interventions. Nitinol, a nickel-titanium alloy known for its unique properties of superelasticity and shape memory, is increasingly utilized in medical devices to improve patient outcomes.

Nitinol's ability to return to a predetermined shape after deformation and its resistance to mechanical stress make it ideal for various medical applications. These properties are particularly beneficial in devices like stents, guidewires, and orthopedic implants, where flexibility and durability are crucial. The material's biocompatibility and corrosion resistance further enhance its suitability for long-term implantation. These properties ensure that nitinol devices maintain their functionality and structural integrity within the human body over extended periods, reducing the risk of rejection or degradation. This reliability makes nitinol a preferred choice for permanent implants used in cardiovascular, neurovascular, and orthopedic treatments. As the demand for minimally invasive procedures grows, the adoption of nitinol-based devices is expected to rise, contributing to the market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $8.1 Billion |

| CAGR | 7.1% |

The hospital segment held a 60.8% share in 2024, driven by the increasing incorporation of advanced medical devices aimed at reducing operative time, minimizing patient trauma, and improving recovery outcomes. Nitinol-based devices-such as stents, guidewires, filters, and orthopedic implants-have become integral to hospitals due to their unique properties like shape memory and super-elasticity, which are critical in minimally invasive interventions. Their superior performance in navigating complex anatomies, particularly during cardiovascular and neurovascular procedures, translates into higher procedural success rates and reduced length of hospital stays.

In 2024, the stents segment maintained its leading position with a 46.1% share, fueled by the rising prevalence of vascular disorders and the clinical advantages provided by nitinol stents. These stents are valued for their self-expanding properties and ability to conform seamlessly to complex vascular pathways, especially in patients with peripheral artery disease or coronary blockages. The demand continues to rise as healthcare providers prioritize less invasive, highly effective treatment options for managing arterial conditions.

North America Nitinol-based Medical Device Market held 40% share in 2024, attributed to the region's robust healthcare infrastructure, well-established reimbursement systems, and early adoption of advanced medical technologies. The presence of leading manufacturers and widespread clinical integration of nitinol-based tools in hospitals and specialty clinics has further reinforced North America's stronghold in this rapidly evolving medical device space.

Key players in the Global Nitinol-Based Medical Device Industry include Boston Scientific Corporation, Medtronic plc, Abbott Laboratories, Terumo Corporation, and B. Braun Melsungen AG. These companies are focusing on research and development to innovate and enhance the performance of nitinol-based devices. Strategic collaborations, mergers, and acquisitions are common as companies aim to expand their product portfolios and market reach. To strengthen their market position, companies in the nitinol-based medical device industry are adopting several key strategies. These include investing in research and development to innovate and improve the performance of nitinol-based devices. Strategic collaborations, mergers, and acquisitions are common as companies aim to expand their product portfolios and market reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for minimally invasive surgeries

- 3.2.1.2 Rising prevalence of cardiovascular and orthopedic disorders

- 3.2.1.3 Technological advancements in medical device manufacturing

- 3.2.1.4 Growing geriatric population globally

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of nitinol-based devices

- 3.2.2.2 Stringent regulatory approval processes

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerationsTrump administration tariffs

- 3.4.1 Impact on trade

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.8 Patent analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Stents

- 5.3 Guidewires

- 5.4 Catheters

- 5.5 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiovascular

- 6.3 Orthopedic

- 6.4 Dental

- 6.5 Neurological

- 6.6 Urology

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Research and academic institutes

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Acandis

- 9.3 Admedes Schuessler

- 9.4 Arthrex

- 9.5 B Braun

- 9.6 Becton, Dickinson and Company

- 9.7 Biotronik

- 9.8 Boston Scientific

- 9.9 Cook Medical

- 9.10 Endosmart

- 9.11 Jotec

- 9.12 Medtronic

- 9.13 MicroPort

- 9.14 Stryker

- 9.15 Terumo

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日