計器着陸装置と視覚的着陸補助装置の市場機会と促進要因、産業動向分析、2025年~2034年予測

Instrument Landing System and Visual Landing Aids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 164 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750326

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

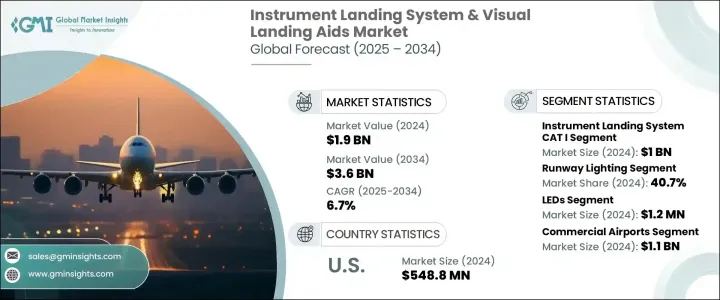

世界の計器着陸装置と視覚的着陸補助装置市場は、2024年には19億米ドルと評価され、航空交通量の増加、空港インフラの継続的な近代化、スマート空港の普及によって、CAGR 6.7%で成長し、2034年には36億米ドルに達すると予測されています。

世界の航空旅行が急増を続ける中、主に民間ジェット機の増加や利用者の増加により、精密着陸技術のニーズが高まっています。空港は、視界不良時の安全を確保し、遅延を減らし、運用効率を向上させるため、先進的な着陸システムに多額の投資を行っています。新興経済諸国の多くが新空港を建設している一方、先進地域は国際航空規格に適合するよう旧施設をアップグレードしています。航空交通量の増加に伴い、ILSと目視誘導システムの需要が高まっています。これらの技術は、安全性の向上と空港容量の最適化に不可欠だからです。

近代化は、これらのシステムの需要を煽る重要な要因です。政府やその他の関係機関は、国際基準を満たすために、ターミナル、滑走路、エアサイド施設の建設やアップグレードに投資しています。先進的なILSや視覚的着陸補助装置は、安全性、交通の流れ、あらゆる気象条件下での運用能力の向上に役立つため、不可欠なものとなりつつあります。さらに、空港運営者は、より多くの交通量をサポートするためのインフラ整備に注力しており、こうした精密システムの必要性をさらに高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 19億米ドル |

| 予測金額 | 36億米ドル |

| CAGR | 6.7% |

ILSの分類では、市場はCAT I、CAT II、CAT IIIシステムに分けられます。2024年には、CAT Iセグメントが10億米ドルを占め、費用対効果とほとんどの気象条件下での運用能力から、地方空港や中規模空港に支持されています。CAT Iシステムは、200フィートの高さで安全な着陸が可能であるため、CAT IIやCAT IIIを導入するための追加コストをかけずに運用の信頼性を高めたい空港にとっては実用的な選択肢となります。

市場には滑走路照明、進入路照明、誘導路照明も含まれ、2024年のシェアは滑走路照明が40.7%です。空港の成長とフライト数の増加に伴い、滑走路照明は夜間の安全な運航と視界不良時の着陸に不可欠となっています。LED照明技術の進歩によりメンテナンスが容易になり、費用対効果も向上したため、最新の照明システムの採用が加速しています。国際的な照明基準への準拠やインフラの近代化の推進が、こうした先進的なシステムの需要に寄与しています。

米国の計器着陸装置と視覚的着陸補助装置市場は、民間航空輸送量の復活と老朽化した空港インフラの近代化に対する重要な取り組みに牽引され、2024年には5億4,880万米ドルと評価されました。同国の航空業界は、増加する航空旅客に対応するため、特に安全性と運航効率の強化に重点を置いた包括的なアップグレードを行っています。連邦航空局(FAA)のネクストジェンプログラムのような重要なイニシアチブは、航空交通管制の近代化とフライトルーティングシステムの最適化を目的としたもので、こうした取り組みの中心となっています。

計器着陸装置と視覚的着陸補助装置の世界市場における主要企業は、コリンズ・エアロスペース(レイセオン・テクノロジーズ)、ハネウェル・インターナショナル、L3ハリス・テクノロジーズ、インドラ・システマスS.A.、タレス・グループなどです。各社は市場での存在感を高めるため、製品の革新や提携といった戦略を採用しています。例えば、Thales GroupとCollins Aerospaceは、安全性の向上とコスト削減のため、高度な着陸システムの開発に注力しています。ハネウェル・インターナショナル社は空港インフラの近代化に多額の投資を行っており、L3ハリス・テクノロジーズ社とインドラ・システマ社(Indra Sistemas S.A.)は着陸補助装置の効率を向上させるためのスマート技術の統合に注力しています。戦略的提携と研究開発への投資は、この急速に拡大する市場で競争力を獲得するための鍵となります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 航空交通量の急増

- 空港インフラの近代化

- スマート空港の出現

- 軍用航空基地および戦術空軍基地の増強

- 技術の進歩の高まり

- 業界の潜在的リスク&課題

- 高い資本コストと維持費

- 複雑さと統合の課題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:ILSカテゴリー別、2021年~2034年

- 主要動向

- 計器着陸装置 CAT I

- 計器着陸装置 CAT II

- 計器着陸装置 CAT III

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 滑走路照明

- アプローチ照明

- 誘導路照明

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- LED

- 白熱電球

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 商業空港

- 軍用空港

- ヘリポート

- 一般航空

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Advanced Navigation &Positioning Corporation(ANPC)

- Aeronautical &General Instruments Limited

- AGI Holdings LLC

- ATG Airports Ltd

- Carmanah Technologies Corp.

- Collins Aerospace(Raytheon Technologies)

- HENAME Co.、Ltd

- Honeywell International Inc.

- Indra Sistemas S.A.

- Intelcan Technosystems Inc.

- L3Harris Technologies

- NEC Corporation

- Normarc Flight Systems AS(a brand under Indra)

- Systems Interface Ltd

- Thales Group

目次

The Global Instrument Landing System and Visual Landing Aids Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 3.6 billion by 2034, driven by the rise in air traffic, the ongoing modernization of airport infrastructures, and the increasing prevalence of smart airports. As global air travel continues to surge, largely due to the growing fleet of commercial jets and more passengers, there is a growing need for precision landing technologies. Airports are making significant investments in advanced landing systems to ensure safety during low-visibility conditions, reduce delays, and improve operational efficiency. Many emerging economies are constructing new airports, while developed regions are upgrading older facilities to meet international aviation standards. With the increase in air traffic, the demand for ILS and visual guidance systems is rising, as these technologies are critical to enhancing safety and optimizing airport capacity.

Modernization is a key factor fueling the demand for these systems. Governments and other relevant bodies are investing in the construction and upgrading of terminals, runways, and airside facilities to meet international standards. Advanced ILS and visual landing aids are becoming more essential as they help improve safety, traffic flow, and the ability to operate in all weather conditions. Additionally, airport operators are focused on improving infrastructure to support higher traffic volumes, further driving the need for these precision systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 6.7% |

In terms of ILS categories, the market is divided into CAT I, CAT II, and CAT III systems. In 2024, the CAT I segment accounted for USD 1 billion, as it is favored by regional and mid-sized airports for its cost-effectiveness and ability to operate in most weather conditions. CAT I systems provide safe landings at decision heights of 200 feet, making them a practical choice for airports looking to enhance operational reliability without the added costs of CAT II or CAT III installations.

The market also includes runway, approach, and taxiway lighting, with the runway lighting segment holding a 40.7% share in 2024. As airports grow and the number of flights increases, runway lighting becomes critical for safe nocturnal operations and landings in poor visibility. Advances in LED lighting technology have made maintenance easier and more cost-effective, accelerating the adoption of modern lighting systems. Compliance with international lighting standards and the push for infrastructure modernization are contributing to the demand for these advanced systems.

U.S. Instrument Landing System & Visual Landing Aids Market was valued at USD 548.8 million in 2024, driven by the resurgence in commercial airline traffic and significant efforts to modernize aging airport infrastructure. The country's aviation industry is undergoing a comprehensive upgrade to accommodate the increasing volume of air travel, with a particular emphasis on enhancing safety and operational efficiency. Key initiatives, such as the FAA's NextGen program, are central to these efforts, designed to modernize air traffic control and optimize flight routing systems.

Key players in the Global Instrument Landing System & Visual Landing Aids Market include Collins Aerospace (Raytheon Technologies), Honeywell International Inc., L3Harris Technologies, Indra Sistemas S.A., and Thales Group. Companies are adopting strategies such as product innovation and partnerships to strengthen their market presence. For instance, Thales Group and Collins Aerospace are focusing on developing advanced landing systems to enhance safety and reduce costs. Honeywell International Inc. is investing heavily in the modernization of airport infrastructure, while L3Harris Technologies and Indra Sistemas S.A. are concentrating on integrating smart technologies to improve the efficiency of landing aids. Strategic collaborations and investments in research and development are key to gaining a competitive edge in this rapidly expanding market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Surge in air traffic growth

- 3.7.1.2 Modernization of airport infrastructure

- 3.7.1.3 Emergence of smart airports

- 3.7.1.4 Increasing military aviation & tactical airbases

- 3.7.1.5 Rising technological advancements

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High capital and maintenance costs

- 3.7.2.2 Complexity and integration challenges

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By ILS Category, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Instrument Landing System CAT I

- 5.3 Instrument Landing System CAT II

- 5.4 Instrument Landing System CAT III

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Runway lighting

- 6.3 Approach lighting

- 6.4 Taxiway lighting

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 LEDs

- 7.3 Incandescent lamps

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Commercial airports

- 8.3 Military airports

- 8.4 Heliports

- 8.5 General aviation

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Advanced Navigation & Positioning Corporation (ANPC)

- 10.2 Aeronautical & General Instruments Limited

- 10.3 AGI Holdings LLC

- 10.4 ATG Airports Ltd

- 10.5 Carmanah Technologies Corp.

- 10.6 Collins Aerospace (Raytheon Technologies)

- 10.7 HENAME Co., Ltd

- 10.8 Honeywell International Inc.

- 10.9 Indra Sistemas S.A.

- 10.10 Intelcan Technosystems Inc.

- 10.11 L3Harris Technologies

- 10.12 NEC Corporation

- 10.13 Normarc Flight Systems AS (a brand under Indra)

- 10.14 Systems Interface Ltd

- 10.15 Thales Group

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 164 Pages

- 納期

- 2~3営業日