外科用ハサミの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Surgical Scissors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750317

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

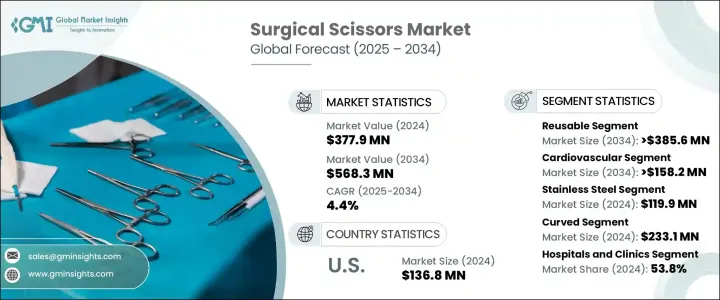

世界の外科用ハサミ市場は、2024年には3億7,790万米ドルと評価され、世界人口の高齢化と慢性疾患患者の増加による手術件数の増加を背景に、CAGR 4.4%で成長し、2034年には5億6,830万米ドルに達すると推定されています。

ヘルスケアシステムが需要増に対応するにつれ、病院や手術センターは高度で高精度の手術器具に投資するようになります。低侵襲手術の革新は、耐久性に優れ、患者の予後を改善するよう設計された手術器具の必要性をさらに押し上げています。精度と安全性が最優先事項となるにつれ、効率的な手術の遂行をサポートする高品質なハサミが不可欠となっています。

心血管障害、がん、糖尿病などの慢性疾患の増加に伴い、外科手術の件数は増加の一途をたどっています。この傾向は、特に高齢者の間で顕著であり、信頼性が高く効率的な外科用ハサミの需要が高まっています。多くのヘルスケア施設は、処置の精度を高め、手術時間を短縮するために、技術的に強化された電動工具に投資しています。市場でも、外科手術のインフラが整備されつつあり、先進的ツールの調達が進んでいるため、同様に需要が増加しています。様々な種類の中でも、再利用可能なハサミは、長期的な運用コストを削減し、ヘルスケアの持続可能性の目標に合致するため、強い支持を集めています。これらのハサミは、タングステンカーバイドや高級ステンレスのような材料で作られており、長寿命、シャープな切れ味、高い性能を提供しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 3億7,790万米ドル |

| 予測金額 | 5億6,830万米ドル |

| CAGR | 4.4% |

外科用ハサミ市場は、再利用型と使い捨て型の2つに大別されます。再利用可能なハサミセグメントは、予測CAGR 4.7%で成長し、2034年には3億8,560万米ドルに達すると予測されます。ヘルスケア施設が長期的なコスト削減に注力するにつれ、再利用可能な器具へのシフトが進んでいます。手術センターや病院では、滅菌して何度も再利用できるハサミの採用が増えており、使い捨ての代替品による廃棄物を最小限に抑えています。さらに、再利用可能なハサミは、ステンレスやタングステンカーバイドのような高品質の材料で作られており、その精度と耐久性を高めています。これらの材料は、手術中の縫合糸の信頼性を向上させています。

外科用ハサミ市場の心血管系手術セグメントは、CAGR 4.8%で成長し、2034年までに1億5,820万米ドルに達すると予測されています。心血管の外科用ハサミは、デリケートな心臓組織へのダメージを最小限に抑え、より良い手術結果を確実にするために、特別に鋭利な刃で設計されています。この鋏の先進的技術により、このような複雑で先進的処置に不可欠な高い精度が実現されています。

米国の外科用ハサミ2024年の市場規模は1億3,680万米ドルで、強力なヘルスケアシステム、手術件数の多さ、手術器具技術の絶え間ない革新から恩恵を受けています。米国は市場のリーダーであり続け、頻繁な新製品の導入と進歩により、さまざまなセグメントにおける手術器具の可用性と専門性を向上させています。その結果、米国市場は引き続き多額の投資を誘致し、精密で効率的な手術のためのより高度で専門的なツールの開発を推進しています。

競合を確保するため、Elixir Surgical、Surgicalholdings、INTEGRA、Storz、WPI、Teleflex、Aspen、HuFriedy、Stryker、KLS Martin、Medline、B. Braun、Millennium Surgical、BD、Scanlanなどの企業は、研究開発と精密製造に多額の投資を行っています。これらの企業は、人間工学に基づいた特殊なハサミの設計、製品ポートフォリオの拡大、世界の販売パートナーシップの強化に注力し、世界中で増大する外科手術の需要に応えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 外科用ハサミ技術の進歩

- 慢性疾患の有病率の上昇

- 低侵襲手術の需要

- 外来手術の急増

- 産業の潜在的リスク・課題

- 製品ライフサイクルが短い

- 再利用可能な器具による感染リスクへの懸念

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 国による対応

- 産業への影響

- 供給側の影響(製造コスト)

- 主要原料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(消費者のコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(製造コスト)

- 影響を受ける主要企業

- 戦略的な産業対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 施策関与

- 展望と今後の検討事項

- 貿易への影響

- 価格分析

- 技術

- ギャップ分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:ハサミタイプ別、2021~2034年

- 主要動向

- 再利用型

- 使い捨て型

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 心血管系

- 整形外科

- 消化器内科

- 神経学

- その他

第7章 市場推定・予測:材料別、2021~2034年

- 主要動向

- ステンレス

- チタン

- タングステン

- セラミック

- その他

第8章 市場推定・予測:先端形態別、2021~2034年

- 主要動向

- カーブ

- ストレート

- その他の先端形態

第9章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院とクリニック

- 外来手術センター

- その他

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Aspen

- B. Braun

- Becton、Dickinson and Company

- ELIXIR SURGICAL

- HuFriedy

- INTEGRA

- STORZ

- KLS Martin

- MEDLINE

- MILLENNIUM SURGICAL

- SCANLAN

- stryker

- Surgicalholdings

- Teleflex

- WPI

目次

The Global Surgical Scissors Market was valued at USD 377.9 million in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 568.3 million by 2034, fueled by the growing number of surgeries driven by an aging global population and an uptick in chronic disease cases. As healthcare systems respond to rising demand, hospitals and surgical centers invest in advanced, high-precision surgical instruments. Innovations in minimally invasive procedures further push the need for surgical tools that are both durable and designed to support better patient outcomes. As precision and safety become top priorities, high-quality scissors have become essential in supporting efficient surgical performance.

With the rise in chronic diseases such as cardiovascular disorders, cancer, and diabetes, the number of surgical interventions continues to grow. This trend, especially among elderly populations, fuels demand for highly reliable and efficient surgical scissors. Many healthcare facilities invest in technologically enhanced power tools to improve procedural accuracy and reduce operation time. Emerging markets are seeing a similar rise in demand due to developing surgical infrastructure, which is pushing procurement of sophisticated tools. Among various types, reusable scissors are gaining strong traction because they reduce long-term operational costs and align with healthcare sustainability goals. These scissors are crafted from materials like tungsten carbide or premium stainless steel and offer enhanced longevity, sharper cuts, and higher performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $ 377.9 Million |

| Forecast Value | $568.3 Million |

| CAGR | 4.4% |

The market for surgical scissors is divided into two main types: reusable and disposable. The reusable scissors segment is expected to grow with a projected CAGR of 4.7%, reaching USD 385.6 million by 2034. As healthcare facilities focus on reducing long-term costs, they are shifting toward reusable instruments. Surgical centers and hospitals are increasingly adopting scissors that can be sterilized and reused multiple times, thus minimizing waste from disposable alternatives. Additionally, reusable scissors are made from high-quality materials like stainless steel or tungsten carbide, which enhances their precision and durability. These materials improve the reliability of sutures during surgeries.

The cardiovascular procedures segment of the surgical scissors market is projected to grow at a CAGR of 4.8% and reach USD 158.2 million by 2034, driven by the precise demands of heart surgeries, where small, accurate incisions are critical for patient survival. Cardiovascular surgical scissors are specially designed with exceptionally sharp blades to minimize damage to delicate heart tissues, ensuring better surgical outcomes. The advanced engineering of these scissors allows for a high level of precision, essential for such complex and high-stakes procedures.

U.S. Surgical Scissors Market generated USD 136.8 million in 2024, benefiting from a strong healthcare system, a high volume of surgeries, and continuous innovations in surgical tool technology. The U.S. remains a leader in the market, with frequent new product introductions and advancements that improve the availability and specialization of surgical instruments across various fields. As a result, the U.S. market continues to attract significant investment, driving the development of more sophisticated and specialized tools for precise and efficient surgeries.

To secure a competitive edge, companies like Elixir Surgical, Surgicalholdings, INTEGRA, Storz, WPI, Teleflex, Aspen, HuFriedy, Stryker, KLS Martin, Medline, B. Braun, Millennium Surgical, BD, and Scanlan are heavily investing in R&D and precision manufacturing. These firms focus on designing ergonomic, specialty scissors, expanding their product portfolios, and strengthening global distribution partnerships to meet increasing surgical demands worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in surgical scissors technology

- 3.2.1.2 Rising prevalence of chronic diseases

- 3.2.1.3 Demand for minimally invasive procedures

- 3.2.1.4 Surge in outpatient surgeries

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Short product lifecycle

- 3.2.2.2 Concerns over infection risks with reusable instruments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Pricing analysis

- 3.7 Technology landscape

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Scissors Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Reusable

- 5.3 Disposable

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiovascular

- 6.3 Orthopedic surgery

- 6.4 Gastroenterology

- 6.5 Neurology

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Materials, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Stainless steel

- 7.3 Titanium

- 7.4 Tungsten

- 7.5 Ceramic

- 7.6 Other materials

Chapter 8 Market Estimates and Forecast, By Tip Shapes, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Curved

- 8.3 Straight

- 8.4 Other tip shapes

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals & clinics

- 9.3 Ambulatory surgery centers

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aspen

- 11.2 B. Braun

- 11.3 Becton, Dickinson and Company

- 11.4 ELIXIR SURGICAL

- 11.5 HuFriedy

- 11.6 INTEGRA

- 11.7 STORZ

- 11.8 KLS Martin

- 11.9 MEDLINE

- 11.10 MILLENNIUM SURGICAL

- 11.11 SCANLAN

- 11.12 stryker

- 11.13 Surgicalholdings

- 11.14 Teleflex

- 11.15 WPI

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日