|

市場調査レポート

商品コード

2027540

ペットアレルギー治療市場の機会、成長促進要因、業界動向分析、予測、2026年~2035年Pet Allergy Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| ペットアレルギー治療市場の機会、成長促進要因、業界動向分析、予測、2026年~2035年 |

|

出版日: 2026年04月14日

発行: Global Market Insights Inc.

ページ情報: 英文 152 Pages

納期: 2~3営業日

|

概要

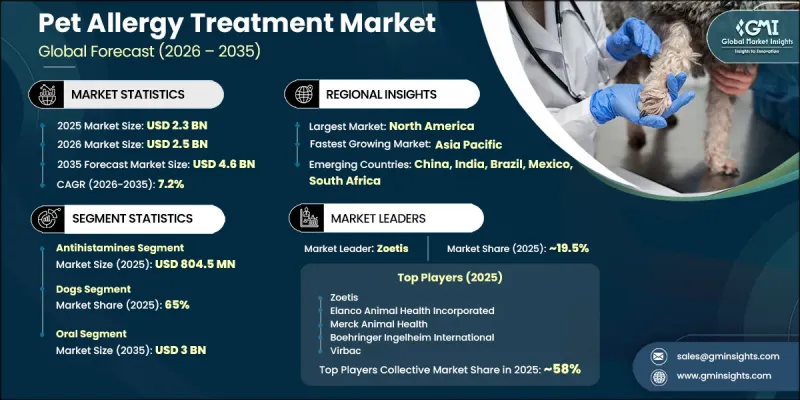

世界のペットアレルギー治療市場は、2025年に23億米ドルと評価され、CAGR7.2%で成長し、2035年までに46億米ドルに達すると推定されています。

市場の拡大は、早期発見と適時の治療に対するペットオーナーの意識の高まりに加え、獣医療へのアクセス改善によって支えられています。獣医学の進歩、特に治療法の革新と診断精度の向上は、治療成果を継続的に高め、治療法の普及を促進しています。ペット用アレルギー治療は、動物に影響を与える幅広いアレルギー症状を管理・抑制するように設計されています。これらのソリューションには、ペットの健康と生活の質を向上させることを目的とした、様々な医薬品や治療アプローチが含まれています。未治療のアレルギーが長期的な健康に及ぼす影響について、ペットオーナーの理解が深まるにつれ、効果的な治療法の需要が大幅に増加しています。また、市場では長期ケアソリューションへの移行が進んでおり、革新的な治療法が注目を集めています。予防医療への意識が高まり続けていることも、製品の受容性をさらに強化し、持続的な市場成長を支えています。獣医療インフラや製品開発への投資増加も、ペットアレルギー治療市場の全体的な拡大に寄与しています。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始金額 | 23億米ドル |

| 予測金額 | 46億米ドル |

| CAGR | 7.2% |

抗ヒスタミン薬セグメントは、2025年に8億450万米ドルの市場規模を記録しました。この優位性は、動物のアレルギー性疾患に対する主要な治療選択肢として広く採用されていることに起因しています。これらの薬剤は、症状を迅速に緩和する効果と良好な安全性プロファイルを備えているため、頻繁に推奨されています。投与方法の多様性と様々な剤形での入手しやすさも、強い市場需要をさらに後押ししています。軽度から中等度のアレルギー反応に対処できるこれらの治療法は、継続的な使用と商業的成功に大きく寄与しています。

2025年、犬向けセグメントは65%のシェアを占めました。このセグメントの成長は、伴侶動物としての犬の需要の高まりと、犬の医療への支出増加に後押しされています。ペットの飼育率の上昇と、動物の健康に対する意識の高まりが、この動向の主な要因となっています。犬におけるアレルギー疾患の発生率の増加は、専門的な治療法への需要をさらに加速させています。さらに、経済状況の改善や、高度で標的を絞った製品の入手可能性の高まりが、予測期間を通じてこのセグメントの拡大を支え続けています。

北米のペットアレルギー治療市場は、2025年に41.8%のシェアを占め、2035年までCAGR6.8%で成長すると予想されています。同地域は、高いペット飼育率とペットの福祉への関心の高まりにより、強固な地位を維持しています。獣医療への多額の支出と、業界をリードする企業の存在が、市場の優位性に寄与しています。先進的な治療ソリューションの早期導入や、ペットの健康状態に対する高い意識が、地域の成長をさらに後押ししています。整備された獣医療エコシステムに加え、ペット医療サービスの広範な受容が、市場における北米のリーダーシップを継続的に強化しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- ペットアレルギーの有病率の増加

- 市販薬(OTC)の入手可能性

- ペットの飼育頭数の増加と獣医療費の増加

- 獣医皮膚科学の進歩

- 業界の潜在的リスク&課題

- 医薬品の副作用

- 自然療法や家庭療法の普及拡大

- 市場機会

- 新興市場での拡大

- 個別化治療の開発

- 成長促進要因

- 規制情勢

- 北米

- 米国

- カナダ

- 欧州

- アジア太平洋地域

- 北米

- 技術・イノベーションの動向

- 現在の技術

- 新興技術

- パイプライン分析(1次調査に基づく)

- 価格分析(1次調査に基づく)

- 将来の市場動向

- AIおよび生成AIが市場に与える影響

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業のマトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:薬剤クラス別、2022年~2035年

- 抗ヒスタミン薬

- コルチコステロイド

- 免疫療法

- その他の薬剤分類

第6章 市場推計・予測:ペットタイプ別、2022年~2035年

- 犬

- 猫

- ウサギ

- その他のペットタイプ

第7章 市場推計・予測:投与経路別、2022年~2035年

- 経口

- 非経口

- 外用

第8章 市場推計・予測:流通チャネル別、2022年~2035年

- 動物病院の薬局

- 小売薬局

- オンライン薬局

第9章 市場推計・予測:地域別、2022年~2035年

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Antech Diagnostics

- Boehringer Ingelheim International

- Ceva Sante Animale

- Dechra

- Elanco

- IDEXX Laboratories

- Merck Animal Health

- Neogen Corporation

- Nextmune

- PetIQ

- Provetica

- Vetoquinol

- Virbac

- Zoetis