ロボット戦闘車両の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Robotic Combat Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750303

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

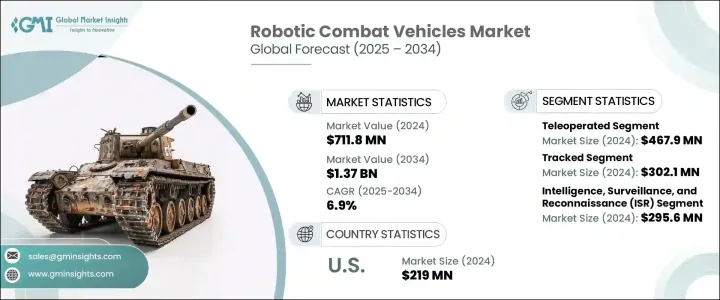

世界のロボット戦闘車両市場は、2024年に7億1,180万米ドルと評価され、世界の防衛予算の増加と人工知能(AI)および自律技術の進歩により、CAGR 6.9%で成長し、2034年には13億7,000万米ドルに達すると推定されています。

各国が国防支出を増やし続ける中、軍事能力の近代化と兵力の有効性の強化に注目が集まっています。RCVは、作戦能力を強化する一方で、人的リスクを大幅に軽減する能力を備えているため、世界的に軍事戦略に不可欠な存在となりつつあります。

人間の介入を最小限に抑えながらリスクの高い環境での任務を可能にすることで、ロボット戦闘車両は戦場を再構築しています。ロボット戦闘車両を使用することで、軍隊は兵士を不必要な危険にさらすことなく、偵察から直接戦闘に至るまで、複雑な作戦をより効率的に実施することができます。これらの車両には高度なセンサー、AIシステム、兵器が搭載されており、監視、捜索救助、さらには攻撃作戦など、従来は人間の兵士が行っていた作業を行うことができます。こうした高度な無人システムに対する需要が高まっている背景には、現代戦争の複雑化があります。今日の軍事作戦では、特に地形が課題であったり、敵の適応能力が高かったりする状況において、より多用途でダイナミックなソリューションが求められています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 7億1,180万米ドル |

| 予測金額 | 13億7,000万米ドル |

| CAGR | 6.9% |

市場は動作モード別によって自律型と遠隔操作型に区分されます。遠隔操作型RCVのセグメントは、2024年に4億6,790万米ドルを創出しました。これは、市街地戦闘や動的戦闘地帯などの複雑な環境でリアルタイム制御を必要とするシステムの需要によるものです。これらのシステムは、軍事要員に高い柔軟性を提供する一方で、任務の信頼性と倫理的配慮に不可欠な人間の制御を維持します。軍が完全自律型システムへと移行していく中で、遠隔操作型RCVは、こうした技術に適応するための重要な中間段階としての役割を果たします。

機動性別から、市場は車輪付き、追跡型、ハイブリッドに分けられます。追跡型RCVセグメントは、2024年に3億210万米ドルを生み出しました。これらの追跡型車両は険しい地形で優れた機動性を発揮するため、困難な環境での前線活動や戦闘状況に最適です。高度な武器やセンサー装置など、より重い積載物を運ぶことができるため、直接戦闘や火力支援の役割における需要がさらに高まっています。さらに、追跡車両は安定性と反動吸収性が高いため、迅速な機動や実戦シナリオに適しています。

米国のロボット戦闘車両(2024年)の市場規模は2億1,900万米ドルでした。これは、地上および空中作戦用の無人システムに対する軍の重点的な取り組みなど、防衛プログラムやイニシアティブに対する政府の多額の支出によるものです。さらに、陸軍のロボット戦闘車構想や海軍の無人システムロードマップなどのプログラムは、これらの技術への関心の高まりに寄与しています。進化する脅威と相まって、軍人のリスクを軽減する必要性が高まっていることも、米国におけるRCVの需要をさらに高めています。

ロボット戦闘車両市場の主要企業数社は、AI主導の機能を統合し、ロボットシステムの堅牢性を向上させることで、積極的に製品提供を強化しています。General Dynamics Land Systems、BAE Systems、Teledyne FLIRなどの主要企業は、これらの車両の機能性と自律性の向上をリードしています。また、偵察、監視、ロジスティクスといった多様な軍事ニーズに対応するため、製品ポートフォリオの拡大にも注力しています。政府機関や防衛請負業者との協力関係も、長期契約を確保し市場での存在感を高めるためにこれらの企業が用いる戦略です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 増加する世界の防衛予算

- AIと自律航法の進歩

- モジュール式戦闘プラットフォームの開発

- 高リスク地域における無人ソリューションの需要

- 軍事近代化プログラムの強化

- 業界の潜在的リスク・課題

- 高額な開発・運用コスト

- サイバーセキュリティの脆弱性

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:動作モード別、2021 ~2034年

- 主要動向

- 自律型

- 遠隔操作型

第6章 市場推計・予測:機動性別、2021 ~2034年

- 主要動向

- 車輪付き

- 追跡型

- ハイブリッド

第7章 市場推計・予測:用途別、2021 ~2034年

- 主要動向

- 情報、監視、偵察(ISR)

- 直接戦闘・火力支援

- 戦闘工学

- 医療搬送

- その他

第8章 市場推計・予測:地域別、2021 ~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- BAE Systems

- Elbit Systems

- General Dynamics Land Systems

- HDT Global

- Israel Aerospace Industries

- Kratos Defense and Security Solutions

- Milrem Robotics

- Nexter Systems

- Oshkosh Defense

- Qinetiq

- Rheinmetall

- Teledyne FLIR

- Textron Systems

目次

The Global Robotic Combat Vehicles Market was valued at USD 711.8 million in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 1.37 billion by 2034, driven by rising global defense budgets and advancements in artificial intelligence (AI) and autonomous technologies. As countries continue to increase their defense spending, there is a heightened focus on modernizing military capabilities and enhancing force effectiveness. RCVs are becoming increasingly integral to military strategies globally due to their ability to significantly reduce the risk to human personnel while enhancing operational capabilities.

By enabling missions in high-risk environments with minimal human intervention, robotic combat vehicles are reshaping the battlefield. Their use allows military forces to conduct complex operations more efficiently, from reconnaissance to direct combat, without exposing soldiers to unnecessary danger. These vehicles are equipped with advanced sensors, AI systems, and weaponry that enable them to perform tasks traditionally carried out by human soldiers, such as surveillance, search-and-rescue, and even offensive operations. The growing demand for these advanced unmanned systems is driven by the increasing complexity of modern warfare. Military operations today require more versatile and dynamic solutions, especially in situations where the terrain is challenging or the enemy is highly adaptive.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $711.8 Million |

| Forecast Value | $1.37 Billion |

| CAGR | 6.9% |

The market is segmented by the mode of operation into autonomous and teleoperated systems. The teleoperated RCVs segment generated USD 467.9 million in 2024, due to the demand for systems that require real-time control in complex environments, such as urban combat or dynamic combat zones. These systems offer military personnel greater flexibility while still retaining human control, which is vital for mission reliability and ethical considerations. As militaries transition toward fully autonomous systems, teleoperated RCVs serve as an important intermediary step in adapting to these technologies.

In terms of mobility, the market is divided into wheeled, tracked, and hybrid vehicles. The tracked RCV segment generated USD 302.1 million in 2024. These tracked vehicles offer superior mobility on rugged terrain, making them ideal for frontline operations and combat situations in difficult environments. Their ability to carry heavier payloads, including advanced weaponry and sensor equipment, further increases their demand in direct combat and fire support roles. Additionally, tracked vehicles provide greater stability and recoil absorption, making them well-suited for rapid maneuvers and live-fire scenarios.

U.S. Robotic Combat Vehicles Market was valued at USD 219 million in 2024 due to substantial government spending on defense programs and initiatives, such as the military's focus on unmanned systems for ground and aerial operations. Furthermore, programs like the Army's Robotic Combat Vehicle initiative and the Navy's unmanned systems roadmap contribute to the growing interest in these technologies. The increasing need to reduce risks to military personnel, coupled with evolving threats, further fuels demand for RCVs in the U.S.

Several key players in the Robotic Combat Vehicles Market are actively enhancing their offerings by integrating AI-driven capabilities and improving the robustness of their robotic systems. Companies like General Dynamics Land Systems, BAE Systems, and Teledyne FLIR are leading the way in advancing the functionality and autonomy of these vehicles. They are also focusing on expanding their product portfolios to cater to diverse military needs, such as reconnaissance, surveillance, and logistics. Collaborations with government agencies and defense contractors are another strategy used by these players to secure long-term contracts and reinforce their market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising global defense budgets

- 3.3.1.2 Advancements in ai and autonomous navigation

- 3.3.1.3 Development of modular combat platforms

- 3.3.1.4 Demand for unmanned solutions in high-risk zones

- 3.3.1.5 Increasing military modernization programs

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High development and operational costs

- 3.3.2.2 Cybersecurity vulnerabilities

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Mode of Operation, 2021 – 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Autonomous

- 5.3 Teleoperated

Chapter 6 Market Estimates and Forecast, By Mobility, 2021 – 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Wheeled

- 6.3 Tracked

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Intelligence, surveillance, and reconnaissance (ISR)

- 7.3 Direct Combat & Fire Support

- 7.4 Combat Engineering

- 7.5 Medical Evacuation

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BAE Systems

- 9.2 Elbit Systems

- 9.3 General Dynamics Land Systems

- 9.4 HDT Global

- 9.5 Israel Aerospace Industries

- 9.6 Kratos Defense and Security Solutions

- 9.7 Milrem Robotics

- 9.8 Nexter Systems

- 9.9 Oshkosh Defense

- 9.10 Qinetiq

- 9.11 Rheinmetall

- 9.12 Teledyne FLIR

- 9.13 Textron Systems

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日