定量配合吸入器の市場機会、促進要因、業界動向分析、2025~2034年予測

Fixed-dose Combination Inhalers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750302

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

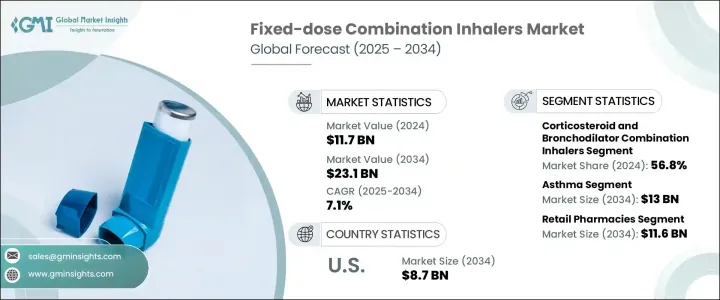

世界の定量配合吸入器市場は、2024年に117億米ドルと評価され、CAGR 7.1%で成長し、2034年には231億米ドルに達すると推定されています。

これらの吸入器は、2種類以上の有効医薬品成分をあらかじめ設定された比率で1つの装置から供給するもので、慢性呼吸器疾患を管理する患者に合理的なアプローチを提供します。喘息や慢性閉塞性肺疾患(COPD)のような呼吸器疾患が世界的に蔓延する中、併用療法の需要は著しく伸びています。この動向は、進化する臨床ガイドライン、併用治療プロトコルを遵守する医師の増加、規制認可の増加、吸入器技術の進歩によってさらに推進されています。呼吸器疾患は、特に中等度から重度の症例において、一貫した長期管理を必要とするため、定量配合吸入器は、複数の個別の吸入器を使用するのに比べ、利便性とコンプライアンスを向上させます。

併用療法へのシフトは国際的な臨床ガイドラインの更新にも影響され、症状が軽い患者にも併用吸入薬が推奨されるようになりました。このため、すべての重症度レベルにおいて吸入器の使用が顕著に増加しています。これらの定量配合吸入器は、コルチコステロイドによって炎症を抑えると同時に、気管支拡張薬によって気流を改善することで、治療効果を高めます。単一デバイスによる投与の利便性は、処方された治療のアドヒアランスを高める上で重要な役割を果たしています。慢性呼吸器疾患の負担が増大する中、ヘルスケアプロバイダーは、より良い臨床結果をもたらし、増悪のリスクを最小限に抑えるために、併用療法を優先しています。この市場はまた、患者と介護者の両方にとって使用を簡素化する吸入器の設計における継続的な技術革新からも恩恵を受けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 117億米ドル |

| 予測金額 | 231億米ドル |

| CAGR | 7.1% |

配合別から、市場はコルチコステロイドと気管支拡張薬の配合吸入薬、長時間作用性β作動薬(LABA)と吸入コルチコステロイド(ICS)の配合吸入薬、3種配合吸入薬、その他の配合吸入薬に分類されます。2024年には、コルチコステロイドと気管支拡張剤の配合吸入剤が56.8%と最大の売上シェアを占め、持続的な呼吸器症状を管理する上でこれらの製剤が臨床的に広く好まれることが原動力となっています。これらの吸入剤は、気道の炎症を抑え、気流を改善するのに特に効果的です。この2つの作用により、症状コントロールが改善されるだけでなく、救急薬の必要性も減少するため、ヘルスケアプロバイダーの間で好んで使用されています。

適応症別に基づき、市場は喘息、慢性閉塞性肺疾患、その他の疾患に区分されます。喘息セグメントは2024年に57.4%と最大のシェアを占め、2034年には130億米ドルに達すると予測されています。喘息と診断される人が世界的に増加しており、特に小児の間で増加していることが、このセグメントの優位性に大きく寄与しています。喘息は慢性かつ再発性の疾患で、症状が安定している時期でも継続的な治療が必要となることが多くあります。このため、定量配合吸入器の反復購入が促進され、安定した収益が得られます。さらに、必要に応じて吸入薬を組み合わせて処方するという最新の臨床的アプローチにより、対象となる患者層が拡大し、このセグメントの成長をさらに後押ししています。

これらの吸入器の流通は主に小売薬局、病院薬局、オンライン薬局を通じて行われています。このうち小売薬局が市場を独占しており、2034年までに116億米ドルに達すると予測されています。慢性呼吸器疾患では定期的な薬の補充が必要であり、小売薬局はこうした継続的なニーズを満たすのに必要な利便性とアクセス性を提供しています。小売薬局は都市部や郊外に広く存在するため、患者は処方箋や薬剤師による相談に簡単にアクセスでき、服薬アドヒアランスを向上させ、着実な市場成長を支えています。

地域別では、北米が引き続き主要市場であり、米国が大きな役割を果たしています。米国の定量配合吸入器市場は2024年に45億米ドルと評価され、2034年には87億米ドルに成長すると予測されています。喘息とCOPDの有病率の高さと、臨床治療プロトコルのコンプライアンスの高さが需要を促進しています。米国の医師は、吸入薬の併用を優先するエビデンスに基づいた治療戦略に従っており、処方率の上昇につながっています。さらに、全国に張り巡らされた薬局網が製品の入手性とリフィルの利便性を高め、使用量の増加に寄与しています。

世界的には、市場は寡占的な構造を維持しており、少数の主要プレーヤーが競合情勢を支配しています。市場シェア全体の約75%は、強力な呼吸器領域のポートフォリオと機器の専門知識を有する大手製薬企業4社が占めています。これらの企業は競争力を維持するため、研究開発に多額の投資を続けています。一方、新興国ではジェネリック医薬品メーカーや地域メーカーが、価格に敏感な人々のニーズに応え、費用対効果の高い代替品を提供することで支持を集めています。市場はまた、使いやすさと患者の転帰を向上させる吸入器デバイスの技術革新に支えられ、1日1回投与オプションや3剤併用療法への傾向が強まっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 喘息および慢性呼吸器疾患の発生率の増加

- 併用療法の使用を支持するガイドライン

- 吸入器技術の進歩

- 複合吸入療法の承認増加

- 業界の潜在的リスク&課題

- 定量配合吸入器の高コスト

- 不適切な使用と副作用に関する懸念

- 促進要因

- 成長可能性分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- 特許分析

- 規制情勢

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:配合別、2021~2034年

- 主要動向

- コルチコステロイドと気管支拡張薬の配合

- 長時間作用型β刺激薬と吸入コルチコステロイドの配合

- 3種配合

- その他

第6章 市場推計・予測:適応症別、2021~2034年

- 主要動向

- 喘息

- 慢性閉塞性肺疾患

- その他

第7章 市場推計・予測:流通チャネル別、2021~2034年

- 主要動向

- 小売薬局

- 病院薬局

- オンライン薬局

第8章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- AstraZeneca

- Boehringer Ingelheim

- Chiesi Farmaceutici

- Cipla

- GlaxoSmithKline

- Glenmark Pharmaceuticals

- Hikma Pharmaceuticals

- Lupin

- Mylan(Viatris)

- Novartis

- Orion

- Sun Pharmaceutical Industries

- Teva Pharmaceuticals

- Vectura Group

- Zydus Group

目次

The Global Fixed-Dose Combination Inhalers Market was valued at USD 11.7 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 23.1 billion by 2034. These inhalers deliver two or more active pharmaceutical ingredients in a pre-set ratio through a single device, offering a streamlined approach for patients managing chronic respiratory conditions. With respiratory illnesses like asthma and chronic obstructive pulmonary disease (COPD) becoming more prevalent globally, the demand for combination therapies has grown significantly. This trend is further propelled by evolving clinical guidelines, growing physician adherence to combination treatment protocols, increasing regulatory approvals, and advancements in inhaler technologies. As respiratory conditions require consistent and long-term management, particularly in moderate to severe cases, fixed-dose inhalers offer enhanced convenience and compliance compared to using multiple separate inhalers.

The shift toward combination therapies is also influenced by updates in international clinical guidelines, which now recommend combination inhalers even for patients with mild symptoms. This has led to a noticeable uptick in inhaler usage across all severity levels. These fixed-dose inhalers enhance treatment efficacy by reducing inflammation through corticosteroids while simultaneously improving airflow using bronchodilators. The convenience of single-device administration plays a critical role in increasing adherence to prescribed treatments. With the growing burden of chronic respiratory diseases, healthcare providers are prioritizing combination therapies to deliver better clinical outcomes and minimize the risk of exacerbations. The market is also benefiting from ongoing innovations in inhaler designs that simplify usage for both patients and caregivers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.7 Billion |

| Forecast Value | $23.1 Billion |

| CAGR | 7.1% |

In terms of combination types, the market is categorized into corticosteroid and bronchodilator combination inhalers, long-acting beta-agonist (LABA) and inhaled corticosteroid (ICS) inhalers, triple combination inhalers, and other combinations. In 2024, corticosteroid and bronchodilator combination inhalers held the largest revenue share at 56.8%, driven by widespread clinical preference for these formulations in managing persistent respiratory symptoms. These inhalers are particularly effective in reducing airway inflammation and improving airflow, which are central to managing both asthma and COPD. The dual action not only improves symptom control but also reduces the need for rescue medications, making them a preferred choice among healthcare providers.

Based on indication, the market is segmented into asthma, chronic obstructive pulmonary disorder, and other conditions. The asthma segment accounted for the largest share at 57.4% in 2024 and is projected to reach a value of USD 13 billion by 2034. The increasing number of individuals diagnosed with asthma globally, especially among children, is significantly contributing to this segment's dominance. Asthma is a chronic and relapsing illness that often requires continuous therapy even during periods of symptom stability. This drives repeat purchases of fixed-dose inhalers and supports consistent revenue generation. Additionally, the updated clinical approach of prescribing combination inhalers for as-needed use has expanded the eligible patient base, further propelling growth in this segment.

The distribution of these inhalers is primarily through retail pharmacies, hospital pharmacies, and online pharmacies. Among these, retail pharmacies dominated the market and are anticipated to reach a value of USD 11.6 billion by 2034. Chronic respiratory diseases necessitate regular medication refills, and retail pharmacies offer the convenience and accessibility required to meet these ongoing needs. Their widespread presence in urban and suburban regions ensures patients have easy access to their prescriptions and pharmacist consultations, which improves adherence and supports steady market growth.

Regionally, North America continues to be a leading market, with the U.S. playing a major role. The fixed-dose combination inhalers market in the U.S. was valued at USD 4.5 billion in 2024 and is projected to grow to USD 8.7 billion by 2034. The high prevalence of asthma and COPD, along with strong compliance with clinical treatment protocols, is fueling demand. Physicians in the U.S. follow evidence-based treatment strategies that prioritize combination inhalers, leading to higher prescription rates. Furthermore, extensive pharmacy networks across the country enhance product availability and refill convenience, contributing to increased usage.

Globally, the market maintains an oligopolistic structure, with a few key players dominating the competitive landscape. Around 75% of the total market share is held by four major pharmaceutical companies with strong respiratory portfolios and device expertise. These firms continue to invest heavily in research and development to maintain their competitive edge. Meanwhile, generic and regional manufacturers are gaining traction in emerging economies by offering cost-effective alternatives, catering to the needs of price-sensitive populations. The market is also witnessing a growing inclination toward once-daily dosing options and triple therapy combinations, supported by innovations in inhaler devices that enhance usability and patient outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of asthma and chronic respiratory diseases

- 3.2.1.2 Favorable guidelines supporting the use of combination therapy

- 3.2.1.3 Advancements in inhaler technologies

- 3.2.1.4 Growing approval of combination inhaler therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of fixed dose combination inhalers

- 3.2.2.2 Concerns related to improper use and side effects

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Patent analysis

- 3.9 Regulatory landscape

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Combination, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Corticosteroid and bronchodilator combination inhalers

- 5.3 Long-acting beta agonist and inhaled corticosteroid combination inhalers

- 5.4 Triple combination

- 5.5 Other combinations

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Asthma

- 6.3 Chronic obstructive pulmonary disorder

- 6.4 Other indications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Retail pharmacies

- 7.3 Hospital pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AstraZeneca

- 9.2 Boehringer Ingelheim

- 9.3 Chiesi Farmaceutici

- 9.4 Cipla

- 9.5 GlaxoSmithKline

- 9.6 Glenmark Pharmaceuticals

- 9.7 Hikma Pharmaceuticals

- 9.8 Lupin

- 9.9 Mylan (Viatris)

- 9.10 Novartis

- 9.11 Orion

- 9.12 Sun Pharmaceutical Industries

- 9.13 Teva Pharmaceuticals

- 9.14 Vectura Group

- 9.15 Zydus Group

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日