|

市場調査レポート

商品コード

1750298

薄肉包装の市場機会、成長促進要因、産業動向分析、2025~2034年予測Thin Wall Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 薄肉包装の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月09日

発行: Global Market Insights Inc.

ページ情報: 英文 177 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

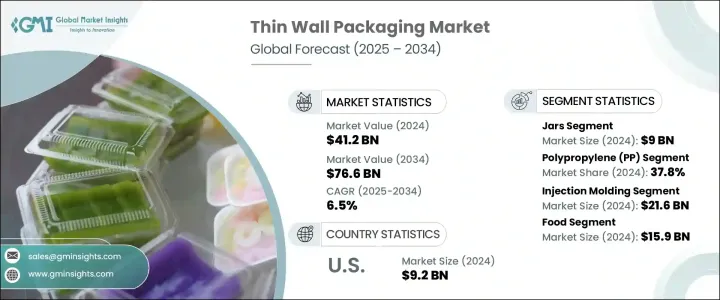

世界の薄肉包装市場は、2024年に412億米ドルと評価され、ライフスタイルパターンの変化、簡便な食品オプションに対する需要の増加、外食チャネルの拡大などを背景に、CAGR 6.5%で成長し、2034年には766億米ドルに達すると予測されています。

都市の中心部が成長し、消費者の日常生活が多忙になるにつれて、軽量で耐久性があり、コスト効率の高い包装形態の魅力が強まっています。薄肉包装は、製品の完全性を保ちながら、迅速な生産と材料使用の削減を可能にします。また、今日のペースの速い小売や食品配送のエコシステムに適合するフォーマットで、現代のサプライチェーンのニーズをサポートします。

持ち運びができ、電子レンジで温められ、再密封可能な容器への需要が高まる中、薄肉包装は都市部での食品消費に欠かせないものとなっています。これらの包装は、特に高密度地域における、外出先での食事やインスタントスナックに対する消費者の嗜好に合致しています。そのバリア特性と構造的完全性により、薄肉容器は持続可能性の目標をサポートしながら賞味期限を延ばすのに役立っています。薄肉容器は現在、乳製品、冷凍食品、スナック菓子の包装に広く選ばれています。消費者は、特に包装の好みがミニマリズムとエコ意識に傾くにつれて、実用性の高いこれらの選択肢に引き寄せられます。ジャーは再利用が可能で、パーソナルケア、家庭用品、食品用途に適しているため人気があります。ジャーは鮮度を保つ効果的な密封性を提供すると同時に、取り扱いも簡単です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 412億米ドル |

| 予測金額 | 766億米ドル |

| CAGR | 6.5% |

ジャーセグメントは2024年に90億米ドルを生み出し、薄肉包装の中で優位性を示しています。これらの容器は、軽量構造、材料使用量の削減、費用対効果の高い生産により、食品、パーソナルケア、家庭用製品のカテゴリーで広く使用されています。ジャーは幅広い用途に理想的な包装ソリューションを提供し、メーカーと消費者の双方に汎用性と機能性を提供します。人気が高まっているのは、その手頃な価格だけでなく、利便性、使いやすさ、持続可能性に対する消費者の嗜好にも起因しています。再利用可能で保管が容易なジャーは、特に繰り返し利用したり、分量を管理したりする必要のある製品に好ましい選択肢となっています。

ポリプロピレン(PP)セグメントは2024年に37.8%のシェアを占めました。このポリマーは強度、軽量性、手頃な価格を兼ね備えているため、特にサイクルの速い射出成形において薄肉包装に理想的です。耐湿性と化学的安定性により、食品用途に適しています。強化されたPP配合により、耐久性を損なうことなく薄肉化が可能になり、企業は規制上の圧力を満たしながら二酸化炭素排出量を削減することができます。

米国の薄肉包装(2024年)の市場規模は92億米ドルとなりました。惣菜やスナックの消費が増加し、軽量で保護性の高い包装ソリューションへの需要が高まっています。さらに、eコマースや宅配サービスの台頭が、材料削減と環境コンプライアンスを優先した包装イノベーションを促しています。この動向は、消費者の意識の高まりと政府主導の持続可能性イニシアティブによってさらに加速しています。

世界の薄肉包装業界の主要企業は、ILIP S.r.l.、Paccor GmbH、Amcor plc、Greiner Packaging International GmbH、Berry Global Inc.です。薄肉包装の世界市場における主要企業は、市場での存在感を高めるため、持続可能なイノベーション、戦略的合併、地域拡大に多額の投資を行っています。各社は軽量設計技術に注力し、バイオベースのポリプロピレンのようなリサイクル可能な素材を採用することで、グリーン包装の義務化に対応しています。いくつかの企業は飲食品ブランドと提携し、棚への陳列を改善し鮮度を長持ちさせるカスタマイズされたソリューションを提供しています。北米やアジア太平洋などの高成長地域における生産能力の拡大は、スピードと効率を向上させるための高度な射出成形機の採用とともに、最優先課題となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- インスタント食品や調理済み食品の需要の急増

- 持続可能性と軽量化の取り組みの成長

- フードデリバリーとQSRチャネルの台頭

- 新興経済における急速な都市化

- 射出成形とインモールドラベリング(IML)の進歩

- 業界の潜在的リスク&課題

- プラスチックの使用に関する厳しい環境規制

- 生鮮食品に対するバリア性の限界

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021~2034年

- 主要動向

- カップ

- タブ容器

- トレイ

- ジャー

- 蓋

- その他の容器

第6章 市場推計・予測:材質別、2021~2034年

- 主要動向

- ポリプロピレン(PP)

- ポリエチレン(PE)

- 高密度ポリエチレン(HDPE)

- 低密度ポリエチレン(LDPE)

- ポリスチレン(PS)

- ポリエチレンテレフタレート(PET)

- ポリ塩化ビニル(PVC)

- その他

第7章 市場推計・予測:生産工程別、2021~2034年

- 主要動向

- 熱成形

- 射出成形

- その他

第8章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 食べ物

- 乳製品

- 調理済み食品

- ベーカリー・菓子類

- 肉、鶏肉、魚介類

- 飲料

- パーソナルケア・化粧品

- 家庭用品

- 電気・電子工学

- 医薬品・栄養補助食品

- 産業

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- ALPLA Group

- Akshar Plastic

- Amcor Plc

- Berry Global Inc.

- Borouge

- Chemco Plast

- Cosmo Films

- Double H Plastics

- EVCO Plastics

- Greiner Packaging International GmbH

- ILIP S.r.l.

- IPL Plastics Inc.

- Mold-Masters

- Paccor

- Prabhoti Plastic Industries

- SABIC

- SP International Industries Pvt. Ltd.

The Global Thin Wall Packaging Market was valued at USD 41.2 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 76.6 billion by 2034, driven by shifting lifestyle patterns, increasing demand for convenience food options, and expanding foodservice channels. As urban centers grow and consumer routines become more hectic, the appeal of lightweight, durable, and cost-efficient packaging formats has intensified. Thin-wall packaging enables quicker production turnaround and reduced material use while delivering product integrity. It also supports modern supply chain needs with formats that fit today's fast-paced retail and food delivery ecosystems.

With rising demand for portable, microwaveable, and resealable containers, thin wall formats have become indispensable across urban food consumption. These packages align with consumers' preference for on-the-go meals and instant snacks, especially in high-density regions. Thanks to their barrier properties and structural integrity, thin wall containers help extend shelf life while supporting sustainability goals. They're now widely chosen for packaging dairy, frozen entrees, and snack foods. Consumers gravitate toward these options for practicality, especially as packaging trends lean more toward minimalism and eco-consciousness. Jars are popular for their reusable nature and suitability across personal care, household goods, and food applications. They offer an effective seal that maintains freshness while being easy to handle.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $41.2 Billion |

| Forecast Value | $76.6 Billion |

| CAGR | 6.5% |

The jars segment generated USD 9 billion in 2024, marking its dominance within the thin wall packaging landscape. These containers are extensively used across food, personal care, and household product categories due to their lightweight structure, reduced material usage, and cost-effective production. Jars offer an ideal packaging solution for a wide range of applications, providing both manufacturers and consumers with versatility and functionality. Their growing popularity stems not only from their affordability but also from consumer-driven preferences for convenience, ease of use, and sustainability. Reusability and easy storage make jars a preferred option, especially for products that require repeated access or portion control.

The polypropylene (PP) segment held a 37.8% share in 2024. This polymer's blend of strength, light weight, and affordability makes it ideal for thin wall packaging, especially in fast-cycle injection molding. Its moisture resistance and chemical stability make it a preferred choice for food-grade applications. Enhanced PP formulations allow thinner walls without compromising durability, enabling companies to reduce carbon footprints while meeting regulatory pressures.

United States Thin Wall Packaging Market generated USD 9.2 billion in 2024. Increased consumption of prepared meals and snacks has fueled demand for lightweight, protective packaging solutions. Additionally, the rise of e-commerce and home delivery services has prompted packaging innovations that prioritize material reduction and environmental compliance. This trend is further accelerated by growing consumer awareness and government-led sustainability initiatives.

Leading companies in the Global Thin Wall Packaging Industry comprise ILIP S.r.l., Paccor GmbH, Amcor plc, Greiner Packaging International GmbH, and Berry Global Inc. Key players in the Global Thin Wall Packaging Market are investing heavily in sustainable innovation, strategic mergers, and regional expansion to enhance market presence. Companies are focusing on lightweight design technologies and adopting recyclable materials like bio-based polypropylene to align with green packaging mandates. Several have partnered with food and beverage brands to offer customized solutions that improve shelf appeal and extend freshness. Expanding production capacity in high-growth regions such as North America and Asia Pacific is a top priority, alongside adopting advanced injection molding machinery to improve speed and efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Surge in demand for convenience and ready-to-eat foods

- 3.7.1.2 Growth in sustainability and lightweighting initiatives

- 3.7.1.3 Rise of food delivery and QSR channels

- 3.7.1.4 Rapid urbanization in emerging economies

- 3.7.1.5 Increasing advancements in injection molding and in-mold labeling (IML)

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Stringent environmental regulations on plastic use

- 3.7.2.2 Limited barrier properties for perishable goods

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Cups

- 5.3 Tubs

- 5.4 Trays

- 5.5 Jars

- 5.6 Lids

- 5.7 Other containers

Chapter 6 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Polypropylene (PP)

- 6.3 Polyethylene (PE)

- 6.3.1 High-density polyethylene (HDPE)

- 6.3.2 Low-density polyethylene (LDPE)

- 6.4 Polystyrene (PS)

- 6.5 Polyethylene terephthalate (PET)

- 6.6 Polyvinyl chloride (PVC)

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Production Process, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Thermoforming

- 7.3 Injection molding

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Food

- 8.2.1 Dairy products

- 8.2.2 Ready-to-eat meals

- 8.2.3 Bakery & confectionery

- 8.2.4 Meat, poultry & seafood

- 8.3 Beverages

- 8.4 Personal care & cosmetics

- 8.5 Household products

- 8.6 Electrical & electronics

- 8.7 Pharmaceuticals & nutraceuticals

- 8.8 Industrial

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ALPLA Group

- 10.2 Akshar Plastic

- 10.3 Amcor Plc

- 10.4 Berry Global Inc.

- 10.5 Borouge

- 10.6 Chemco Plast

- 10.7 Cosmo Films

- 10.8 Double H Plastics

- 10.9 EVCO Plastics

- 10.10 Greiner Packaging International GmbH

- 10.11 ILIP S.r.l.

- 10.12 IPL Plastics Inc.

- 10.13 Mold-Masters

- 10.14 Paccor

- 10.15 Prabhoti Plastic Industries

- 10.16 SABIC

- 10.17 SP International Industries Pvt. Ltd.