真空コンタクタ市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Vacuum Contactor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750290

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

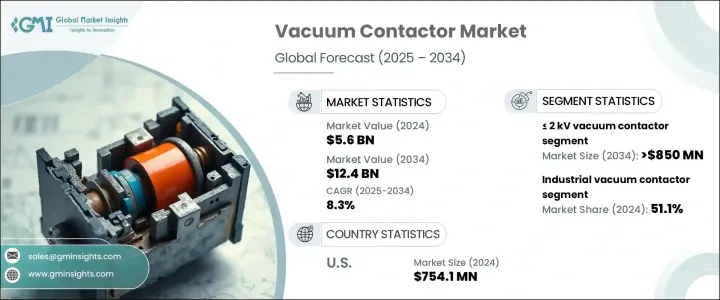

真空コンタクタの世界市場規模は、2024年に56億米ドルとなり、電力インフラへの投資の増加、エネルギー効率の高いソリューションへの需要の高まり、スマートグリッドシステムの展開拡大などを背景に、CAGR 8.3%で成長し、2034年には124億米ドルに達すると予測されています。

産業界や公益事業体が、最新のエネルギーネットワークを支える信頼性の高い高性能スイッチングソリューションを求め続けているため、真空コンタクタの需要は勢いを増しています。技術の進歩に加え、自動化へのシフトや、電力ミックスにおける再生可能エネルギーの割合の増加が加わり、市場拡大のための強固な基盤が形成されつつあります。

この成長の主な要因の1つは、ミッションクリティカルな環境において信頼性の高い配電を保証する、安全で耐久性のある高速スイッチングデバイスに対するニーズの高まりです。真空コンタクタは、低メンテナンス、高い電気耐久性、コンパクトな設計などの利点を備えており、さまざまな産業用およびユーティリティ用途に適しています。特に、アーク放電のリスクを最小限に抑えなければならない中電圧環境では、機器の安全性に対する意識が高まっているため、真空コンタクタの使用は拡大しています。さらに、各分野で電化が進み、運用信頼性が重視されるようになったことで、エンドユーザーは、老朽化した電気機械式コンタクタを含むことが多い既存システムのアップグレードを進めています。この移行は、近代化された電気インフラを促進する有利な規制やインセンティブによってさらに後押しされています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 56億米ドル |

| 予測金額 | 124億米ドル |

| CAGR | 8.3% |

同市場は、2 kV未満、2 kV~5 kV、5 kV~10 kV、10 kV以上など、定格電圧別にセグメント化されています。このうち、<=2 kVのセグメントは2034年までに8億5,000万米ドルを超えると予測されています。このセグメントは、コンパクトな環境でエネルギー効率の高いシステムの導入が増加しているため、特に人気があります。この電圧範囲の真空コンタクタは、信頼性が高く、設置面積が小さく、最小限のメンテナンスが重要な要件であるスペースが限られた環境に適しているため、好まれています。

最終用途の観点から、市場は商業、工業、公益事業に分類されます。2024年の市場は、産業分野が51.1%のシェアを占めました。この優位性は、エネルギー効率基準の厳格化と、生産施設や処理装置における信頼性の高い故障処理装置へのニーズの高まりに起因しています。さらに、特に開発途上地域における工業生産能力の拡大が、幅広い用途への真空コンタクタ展開の新たな機会を生み出しています。

地域別では米国が市場成長に大きく貢献しており、2022年の評価額は6億9,220万米ドル、2023年には7億2,090万米ドル、2024年には7億5,410万米ドルに達します。同国では、特に再生可能エネルギーと電気自動車の分野でインフラ開発のペースが高まっており、真空コンタクタの採用が拡大しています。国内送電網の近代化と産業部門の運用効率向上を目指す官民の取り組みが、製品需要を加速させています。さらに、性能の中断を防ぎつつ運用コストを下げることに重点を置くことで、利害関係者は従来の代替品ではなく真空コンタクタを選択するようになっています。

競合情勢は中程度にまとまっており、上位5社が世界市場シェアの約40%を占めています。これらの企業には、広範な製品ポートフォリオと確立されたサービスネットワークを持つ大手多国籍企業が含まれます。これらの企業は、研究開発への継続的な投資に加え、地域的なパートナーシップや真空コンタクタへのスマート機能の統合により、市場での強力な足場を維持しています。これらの企業は、製品の寿命を延ばし、エネルギー損失を低減し、遠隔診断をサポートする技術にますます注力しており、デジタル化とスマートエネルギーシステムの幅広い動向と一致しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- モータースターター

- トランス

- コンデンサ

- 原子炉

- 抵抗負荷

- その他

第6章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 2 kV未満

- 2kV~5kV以上

- 5kV~10kV以上

- 10kV以上

第7章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 商業用

- 産業

- ユーティリティ

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ロシア

- ドイツ

- スペイン

- イタリア

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- インドネシア

- マレーシア

- タイ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- イラン

- エジプト

- 南アフリカ

- ナイジェリア

- トルコ

- モロッコ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第9章 企業プロファイル

- ABB

- Datsons Electronics

- Eaton

- EAW Relaistechnik

- ElectronTubes

- GREENSTONE

- Hansen Electric

- HIITIO New Energy

- Kunshan GuoLi Electronic Technology

- Liyond

- LS ELECTRIC

- Mitsubishi Electric Corporation

- Pentagon Switchgears

- Rockwell Automation

- Schneider Electric

- Schrack Technik

目次

The Global Vacuum Contactor Market was valued at USD 5.6 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 12.4 billion by 2034, driven by increasing investments in power infrastructure, rising demand for energy-efficient solutions, and expanding deployment of smart grid systems. As industries and utilities continue to seek reliable, high-performance switching solutions that support modern energy networks, the demand for vacuum contactors is gaining momentum. Technological advancements, combined with a shift toward automation and the rising share of renewable energy in the power mix, are creating a robust foundation for market expansion.

One of the major factors contributing to this growth is the increasing need for safe, durable, and fast-switching devices that ensure reliable power distribution in mission-critical environments. Vacuum contactors offer advantages such as low maintenance, high electrical endurance, and compact designs that make them suitable for a variety of industrial and utility applications. Their use is expanding due to heightened awareness of equipment safety, especially in medium-voltage environments, where arc flash risks must be minimized. Additionally, the growth in electrification across sectors and an increasing emphasis on operational reliability are pushing end users to upgrade existing systems, which often include aging electromechanical contactors. This transition is further supported by favorable regulations and incentives that promote modernized electrical infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.6 Billion |

| Forecast Value | $12.4 Billion |

| CAGR | 8.3% |

The market is segmented by voltage rating, including <= 2 kV, > 2 kV to 5 kV, > 5 kV to 10 kV, and > 10 kV. Among these, the <= 2 kV segment is forecast to exceed USD 850 million by 2034. This segment is particularly popular due to the increasing deployment of energy-efficient systems in compact environments. Vacuum contactors in this voltage range are favored for their reliability, smaller footprint, and suitability for space-constrained settings where minimal maintenance is a key requirement.

In terms of end use, the market is classified into commercial, industrial, and utility sectors. The industrial segment dominated the market in 2024 with a share of 51.1%. This dominance can be attributed to stricter energy efficiency standards and the growing need for dependable fault-handling equipment in production facilities and processing units. Moreover, expanding industrial manufacturing capacities, particularly in developing regions, are creating new opportunities for vacuum contactor deployment across a wide range of applications.

Regionally, the United States has emerged as a significant contributor to market growth, with valuations of USD 692.2 million in 2022, USD 720.9 million in 2023, and USD 754.1 million in 2024. The increasing pace of infrastructure development in the country, especially in renewable energy and electric vehicle sectors, is leading to greater adoption of vacuum contactors. Public and private sector initiatives aimed at modernizing the national grid and enhancing operational efficiency in industrial sectors are accelerating product demand. Moreover, the focus on lowering operational costs while ensuring uninterrupted performance is prompting stakeholders to choose vacuum contactors over conventional alternatives.

The competitive landscape is moderately consolidated, with the top five players accounting for approximately 40% of the global market share. These include leading multinational corporations with extensive product portfolios and well-established service networks. Their continued investments in R&D, combined with regional partnerships and integration of smart features into vacuum contactors, are helping them maintain a strong foothold in the market. These companies are increasingly focusing on technologies that enhance product longevity, reduce energy losses, and support remote diagnostics, aligning with the broader trends in digitalization and smart energy systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 Motor starter

- 5.3 Transformer

- 5.4 Capacitor

- 5.5 Reactor

- 5.6 Resistive loads

- 5.7 Others

Chapter 6 Market Size and Forecast, By Voltage, 2021 - 2034 ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 ≤ 2 kV

- 6.3 > 2 kV to 5 kV

- 6.4 > 5 kV to 10 kV

- 6.5 > 10 kV

Chapter 7 Market Size and Forecast, By End Use, 2021 - 2034 ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 Commercial

- 7.3 Industrial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 ('000 Units & USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Russia

- 8.3.4 Germany

- 8.3.5 Spain

- 8.3.6 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.4.6 Indonesia

- 8.4.7 Malaysia

- 8.4.8 Thailand

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Iran

- 8.5.4 Egypt

- 8.5.5 South Africa

- 8.5.6 Nigeria

- 8.5.7 Turkey

- 8.5.8 Morocco

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Datsons Electronics

- 9.3 Eaton

- 9.4 EAW Relaistechnik

- 9.5 ElectronTubes

- 9.6 GREENSTONE

- 9.7 Hansen Electric

- 9.8 HIITIO New Energy

- 9.9 Kunshan GuoLi Electronic Technology

- 9.10 Liyond

- 9.11 LS ELECTRIC

- 9.12 Mitsubishi Electric Corporation

- 9.13 Pentagon Switchgears

- 9.14 Rockwell Automation

- 9.15 Schneider Electric

- 9.16 Schrack Technik

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日