|

市場調査レポート

商品コード

1750285

ジオポリマーセメント市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Geopolymer Cement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ジオポリマーセメント市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月16日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

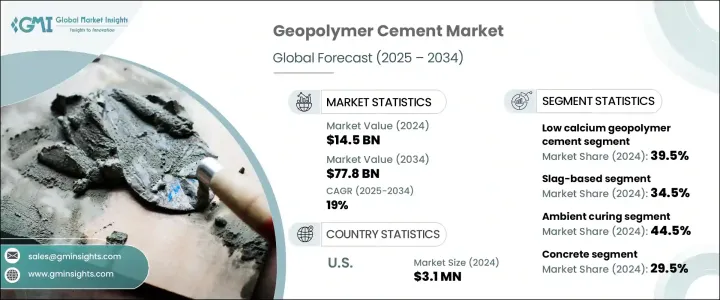

ジオポリマーセメントの世界市場規模は2024年に145億米ドルとなり、CAGR 19%で成長し、2034年には778億米ドルに達すると予測されています。

建設業界が環境に配慮した慣行へとシフトする中、低排出材料の魅力は高まり続けています。この動向は、気候変動と闘い、進化する環境規制を遵守する緊急性が高まっていることが大きく影響しています。各国政府がより厳しい持続可能性規制を導入する中、建設業界は従来の建設資材に代わる、よりクリーンで高性能な資材を積極的に求めています。ジオポリマーセメントは、従来のポルトランドセメントに比べて二酸化炭素排出量を最大90%削減する低カーボンフットプリントという点で際立っています。より持続可能な解決策を提供するだけでなく、優れた機械的・化学的特性も備えているため、インフラ開発において好ましい選択肢となっています。各分野における脱炭素化の推進は、長期的なエコロジー目標をサポートする革新的な材料への需要を促しており、ジオポリマーセメントは、エネルギー効率とバージン原料への依存度の低減という点でその要求に合致しています。

規制による圧力に加え、世界の都市化の進展が、耐久性が高く費用対効果の高い建材の必要性に拍車をかけています。世界各地、特に新興経済諸国では開発が加速しており、交通網、商業スペース、住宅プロジェクトへの投資が急増しています。ジオポリマーセメントは、現代建築の技術的・環境的要求を満たすものとして、市場の支持を集めています。ジオポリマーセメントは、極端な気象条件への耐性と長持ちする耐久性を備えているため、特に応力の大きい用途に適しています。持続可能な建築基準やグリーン建築の奨励策の採用が増加していることも、市場の拡大をさらに後押ししています。産業界や政府が循環経済の目標に沿った信頼性の高い代替品を求める中、ジオポリマーセメントはトップランナーとして台頭しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 145億米ドル |

| 予測金額 | 778億米ドル |

| CAGR | 19% |

フライアッシュや高炉スラグのような産業廃棄物を活用することで、全体的な生産コストを削減します。ジオポリマーセメントは、フライアッシュや高炉スラグのような産業廃棄物を活用することで、製造時のエネルギー消費を最小限に抑えながら、全体的な製造コストを削減します。これらの原材料は、他の産業プロセスから調達されることが多く、持続可能性の目標をサポートするクローズド・ループ・システムを作り出しています。この材料は、生産コストが低いだけでなく、耐熱性や耐薬品性にも優れているため、幅広い建設ニーズに対して経済的にも環境的にも実行可能な選択肢となっています。

2024年には、低カルシウムジオポリマーセメントが世界売上高の39.5%を占め、最も高い市場シェアを獲得しました。このタイプは主にフライアッシュに由来し、強い耐熱性、化学的安定性、環境への影響の低減が認められています。これらの特性により、過酷な条件下で高い性能を必要とする用途に好んで使用されています。原料面では、フライアッシュベースのセグメントとスラグベースのセグメントを合わせたシェアは、市場全体の34.5%に達しました。これらの材料は容易に入手できるだけでなく、優れた圧縮強度と長期耐久性を発揮します。これらの材料の利用は、埋立廃棄物や温室効果ガス排出の削減に貢献し、世界の持続可能性目標に合致しています。

硬化技術はジオポリマーセメントの性能と適用性に大きく影響します。2024年には、常温硬化が44.5%の市場シェアを占め、支配的な地位を占めています。この方法は、必要なエネルギーが少なく、工程が簡略化されているため、一般的な建設やメンテナンス作業に適しています。時間に制約のあるプロジェクトや構造的に要求の厳しいプロジェクトでは、強度を高め、硬化時間を短縮できる熱硬化が好まれます。どちらの技術も、プロジェクトの仕様に応じた柔軟性を提供し、この材料の適用分野を広げています。

用途別では、コンクリートが29.5%のシェアで市場をリードしています。ジオポリマーコンクリートは、優れた強度、低い収縮率、高い耐薬品性を備えており、大規模プロジェクトに最適な材料となっています。ジオポリマーコンクリートはグリーンビルディング基準に適合しているため、LEED認証や同様の持続可能性を求める請負業者や開発業者にとって魅力的な材料となっています。2024年には、建築・建設セクターが市場全体の34.5%を占め、最大の最終用途産業となりました。住宅、商業、工業の各分野で広く使用されていることから、この材料の適応性が浮き彫りになり、環境意識の高い建築慣行における重要性が高まっています。

地域別では、米国が2024年に310万米ドルとなり、世界シェアの80%以上を占める主要市場に浮上しました。同国の強い地位は、インフラ投資の増加、厳格な環境ガイドライン、持続可能な開発へのコミットメントの高まりによって支えられています。また、フライアッシュやスラグなどの原材料への容易なアクセスも、国内生産と採用を支え、サプライチェーンの課題を軽減し、炭素への影響を低減しています。米国市場は、持続可能な建築材料に関する有利な政策と技術の進歩により成長を続けています。

ジオポリマーセメント市場の主要企業は、配合を改良し製品性能を向上させるための研究開発に多額の投資を行っています。独自の技術や次世代の製造方法に注力することで、これらの企業は一貫した品質を提供し、用途の柔軟性を高めることを目指しています。流通網を拡大しながら技術革新に努めることで、多様な顧客ニーズに対応し、進化する世界情勢の中で競合優位性を維持しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 市場イントロダクション

- トランプ政権の関税の影響- 構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)注:上記の貿易統計は主要国についてのみ提供されます

- 主要輸出国

- 主要輸入国

- 業界バリューチェーン分析

- 利益率分析

- 製品概要

- ジオポリマーの化学と形成

- ポルトランドセメントとの比較

- 環境へのメリットと二酸化炭素排出量

- 機械的特性と性能特性

- 耐久性と耐性

- 設定時間と作業性

- 制限と課題

- 市場力学

- 市場促進要因

- 環境規制と持続可能性への取り組み

- 特に新興経済国におけるインフラ開発の拡大

- 従来のセメントに比べて、CO2排出量とエネルギー消費量の削減など、コスト面で有利です

- 市場抑制要因

- 石炭や鉄鋼などの主要産業の操業が衰退しています

- 特定のアプリケーションにおける技術的な制限により、より広範な使用が制限されます

- 請負業者と建設業者の意識と技術的知識の欠如

- 市場機会

- 環境に優しい建築資材への注目が高まっています

- 耐久性と高性能を兼ね備えたインフラストラクチャソリューションに対する需要が高まっています

- ジオポリマー配合における技術的進歩

- 市場の課題

- 標準化と認証の問題

- 既存のセメントタイプとの競合

- 従来のセメントに比べてコスト競争力があります

- 市場促進要因

- 業界への影響要因

- 成長可能性分析

- 業界の潜在的リスク&課題

- 規制の枠組みと基準

- 建築基準法および建設基準

- 環境規制

- 炭素価格設定と排出量取引

- グリーンビルディング認証

- 廃棄物利用政策

- 製造プロセス分析

- 原材料の準備

- アルカリ活性剤の製造

- 混合と配合

- 硬化方法

- 品質管理手順

- 原材料分析と調達戦略

- 価格分析

- 持続可能性と環境影響評価

- PESTEL分析

- ポーターのファイブフォース分析

第4章 競合情勢

- 市場シェア分析

- 戦略枠組み

- 合併と買収

- ジョイントベンチャーとコラボレーション

- 新製品開発

- 拡大戦略

- 競合ベンチマーキング

- ベンダー情勢

- 競合ポジショニングマトリックス

- 戦略的ダッシュボード

- 特許分析とイノベーション評価

- 新規参入者の市場参入戦略

- 調査開発集約度分析

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- カルシウム不足ジオポリマーセメント

- 高カルシウムジオポリマーセメント

- リン酸ベースのジオポリマーセメント

- ケイ酸塩系ジオポリマーセメント

- その他

第6章 市場推計・予測:原材料別、2021年~2034年

- 主要動向

- フライアッシュベース

- クラスFフライアッシュ

- クラスCフライアッシュ

- その他のフライアッシュタイプ

- スラグベース

- 粉砕高炉スラグ(GGBFS)

- その他のスラグの種類

- メタカオリンベース

- 天然アルミノケイ酸塩ベース

- 赤泥ベース

- ハイブリッドおよびブレンドシステム

- その他

第7章 市場推計・予測:硬化方法別、2021年~2034年

- 主要動向

- 常温硬化

- 熱硬化

- 蒸気硬化

- その他

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- コンクリート

- 生コンクリート

- プレキャストコンクリート

- その他の具体的な用途

- モルタルとグラウト

- プレキャスト要素

- ブロックとレンガ

- パネルとスラブ

- パイプと柱

- その他のプレキャスト要素

- 舗装とオーバーレイ

- 修理と修復

- 廃棄物の封入と固定化

- その他の用途

第9章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 建築・建設

- 住宅用

- 商業用

- 産業

- インフラストラクチャー

- 道路と橋

- ダムと水管理

- 空港と港

- その他のインフラ

- 石油・ガス

- 鉱業

- 海洋および水中建設

- 原子力および廃棄物管理

- その他

第10章 市場推計・予測:パフォーマンス属性別、2021年~2034年

- 主要動向

- 高強度

- 耐薬品性

- 耐火性

- 低収縮

- 急速硬化

- その他のパフォーマンス属性

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第12章 企業プロファイル

- Alchemy Geopolymer Solutions、LLC

- Banah UK Ltd.

- BASF SE

- CEMEX S.A.B. de C.V.

- Ceratech Inc.

- Concrete Canvas Ltd.

- Dow Chemical Company

- GCP Applied Technologies Inc.

- Geobeton Pty Ltd.

- Geopolymer Products

- Geopolymer Solutions、LLC

- Halliburton

- Imerys S.A.

- Kiran Global Chems Limited

- LafargeHolcim Ltd.

- Metna Co.

- Milliken Infrastructure Solutions、LLC

- Nu-Core

- PCI Augsburg GmbH

- Pyromeral Systems

- Reno Refractories、Inc.

- Rocla Pty Limited

- Schlumberger Limited

- Sika AG

- Siloxo Pty Ltd.

- Tech-Crete Processors Ltd.

- Uretek Worldwide

- Wagners

- Wollner GmbH

- Zeobond Pty Ltd.

The Global Geopolymer Cement Market was valued at USD 14.5 billion in 2024 and is estimated to grow at a CAGR of 19% to reach USD 77.8 billion by 2034. As the construction industry shifts toward environmentally responsible practices, the appeal of low-emission materials continues to grow. This trend is largely influenced by the increasing urgency to combat climate change and comply with evolving environmental regulations. As governments introduce stricter sustainability mandates, industries are actively seeking cleaner, high-performance alternatives to traditional construction materials. Geopolymer cement stands out in this regard due to its low carbon footprint, generating up to 90% fewer carbon emissions compared to conventional Portland cement. It offers not only a more sustainable solution but also superior mechanical and chemical properties, making it a preferred choice in infrastructure development. The push for decarbonization across sectors is driving demand for innovative materials that support long-term ecological goals, and geopolymer cement fits the bill with its energy efficiency and reduced reliance on virgin raw materials.

In addition to regulatory pressures, rising global urbanization is fueling the need for durable and cost-effective building materials. As development accelerates in various parts of the world, especially in growing economies, investment in transport networks, commercial spaces, and residential projects is surging. Geopolymer cement is gaining market traction as it meets both the technical and environmental demands of modern construction. Its resistance to extreme weather conditions and long-lasting durability make it particularly suitable for high-stress applications. The increasing adoption of sustainable building codes and incentives for green construction is further supporting market expansion. As industries and governments seek reliable alternatives that align with circular economy goals, geopolymer cement is emerging as a frontrunner.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.5 Billion |

| Forecast Value | $77.8 Billion |

| CAGR | 19% |

Cost efficiency plays a crucial role in the material's growing popularity. Geopolymer cement leverages industrial waste products like fly ash and blast furnace slag, which reduces the overall production cost while also minimizing energy consumption during manufacturing. These raw materials are often sourced from other industrial processes, creating a closed-loop system that supports sustainability goals. Alongside its lower production expenses, the material delivers excellent resistance to heat and chemicals, making it an economically and environmentally viable option for a wide range of construction needs.

In 2024, low calcium geopolymer cement captured the highest market share, accounting for 39.5% of global revenue. This type is primarily derived from fly ash and is recognized for its strong thermal resistance, chemical stability, and reduced environmental impact. These attributes make it a preferred choice in applications requiring high performance under extreme conditions. On the raw material front, the combined share of fly ash-based and slag-based segments reached 34.5% of the total market. These materials are not only readily accessible but also deliver excellent compressive strength and long-term durability. Their utilization contributes to reducing landfill waste and greenhouse gas emissions, aligning with global sustainability targets.

Curing techniques significantly influence the performance and applicability of geopolymer cement. In 2024, ambient curing held the dominant position, with a market share of 44.5%. This method is favored for its low energy requirement and simplified process, which makes it ideal for general construction and maintenance work. For time-sensitive or structurally demanding projects, heat curing is preferred as it enhances strength and reduces setting time. Both techniques offer flexibility depending on project specifications, broadening the material's applicability across sectors.

From an application perspective, concrete led the market with a 29.5% share. Geopolymer concrete offers excellent strength, low shrinkage, and high chemical resistance, making it a go-to material for large-scale projects. Its compliance with green building standards adds to its appeal among contractors and developers seeking LEED certifications or similar sustainability credentials. The building and construction sector represented the largest end-use industry in 2024, holding 34.5% of the total market. Its widespread use in residential, commercial, and industrial settings highlights the material's adaptability and growing importance in eco-conscious construction practices.

Regionally, the United States emerged as the leading market, valued at USD 3.1 million in 2024 and accounting for over 80% of the global share. The country's strong position is supported by rising infrastructure investment, strict environmental guidelines, and a growing commitment to sustainable development. Easy access to raw materials such as fly ash and slag also supports domestic production and adoption, reducing supply chain challenges and lowering carbon impact. The US market continues to grow due to favorable policies and technological advancements in sustainable building materials.

Leading companies in the geopolymer cement market are investing heavily in research and development to refine formulations and improve product performance. By focusing on proprietary technologies and next-generation manufacturing methods, these players aim to deliver consistent quality and enhance application flexibility. Their efforts to innovate while expanding distribution networks are enabling them to address varied customer needs and maintain a competitive edge in an evolving global landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research Methodology

- 1.2 Research Objectives

- 1.3 Market Definition and Scope

- 1.4 Market Segmentation

- 1.5 Data Sources

- 1.5.1 Primary Research

- 1.5.2 Secondary Research

- 1.6 Market Estimation Approach

- 1.7 Research Assumptions and Limitations

- 1.8 Base Year and Forecast Period

Chapter 2 Executive Summary

- 2.1 Market Snapshot

- 2.2 Segment Highlights

- 2.3 Competitive Landscape Snapshot

- 2.4 Regional Market Outlook

- 2.5 Key Market Trends

- 2.6 Future Market Outlook

Chapter 3 Industry Insights

- 3.1 Market Introduction

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets.

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Industry value chain analysis

- 3.5 Profit margin analysis

- 3.6 Product overview

- 3.6.1 Geopolymer chemistry & formation

- 3.6.2 Comparison with Portland cement

- 3.6.3 Environmental benefits & carbon footprint

- 3.6.4 Mechanical properties & performance characteristics

- 3.6.5 Durability & resistance properties

- 3.6.6 Setting time & workability

- 3.6.7 Limitations & challenges

- 3.7 Market dynamics

- 3.7.1 Market drivers

- 3.7.1.1 Environmental regulations and sustainability initiatives.

- 3.7.1.2 Growing infrastructure development, particularly in emerging economies.

- 3.7.1.3 Cost advantages over traditional cement, including reduced CO2 emissions and energy consumption.

- 3.7.2 Market restraints

- 3.7.2.1 Declining operations in key industries like coal and steel.

- 3.7.2.2 Technical limitations in certain applications, restricting wider use.

- 3.7.2.3 Lack of awareness and technical knowledge among contractors and builders.

- 3.7.3 Market opportunities

- 3.7.3.1 Increasing focus on green building materials.

- 3.7.3.2 Rising demand for durable and high-performance infrastructure solutions.

- 3.7.3.3 Technological advancements in geopolymer formulations.

- 3.7.4 Market challenges

- 3.7.4.1 Standardization and certification issues.

- 3.7.4.2 Competition from established cement types.

- 3.7.4.3 Cost competitiveness with conventional cement.

- 3.7.1 Market drivers

- 3.8 Industry impact forces

- 3.8.1 Growth potential analysis

- 3.8.2 Industry pitfalls & challenges

- 3.9 Regulatory framework & standards

- 3.9.1 Building codes & construction standards

- 3.9.2 Environmental regulations

- 3.9.3 Carbon Pricing & Emissions Trading

- 3.9.4 Green building certifications

- 3.9.5 Waste material utilization policies

- 3.10 Manufacturing process analysis

- 3.10.1 Raw material preparation

- 3.10.2 Alkaline activator production

- 3.10.3 Mixing & formulation

- 3.10.4 Curing methods

- 3.10.5 Quality control procedures

- 3.11 Raw material analysis & procurement strategies

- 3.12 Pricing analysis

- 3.13 Sustainability & environmental impact assessment

- 3.14 Pestle analysis

- 3.15 Porter's five forces analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Market share analysis

- 4.2 Strategic framework

- 4.2.1 Mergers & acquisitions

- 4.2.2 Joint ventures & collaborations

- 4.2.3 New product developments

- 4.2.4 Expansion strategies

- 4.3 Competitive benchmarking

- 4.4 Vendor landscape

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Patent analysis & innovation assessment

- 4.8 Market entry strategies for new players

- 4.9 Research & development intensity analysis

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Low calcium geopolymer cement

- 5.3 High calcium geopolymer cement

- 5.4 Phosphate-based geopolymer cement

- 5.5 Silicate-based geopolymer cement

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Raw Material Source, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Fly Ash-Based

- 6.2.1 Class F fly ash

- 6.2.2 Class C fly ash

- 6.2.3 Other fly ash types

- 6.3 Slag-Based

- 6.3.1 Ground granulated blast furnace slag (GGBFS)

- 6.3.2 Other slag types

- 6.4 Metakaolin-based

- 6.5 Natural aluminosilicate-based

- 6.6 Red mud-based

- 6.7 Hybrid & blended systems

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Curing Method, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Ambient curing

- 7.3 Heat curing

- 7.4 Steam curing

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Concrete

- 8.2.1 Ready-mix concrete

- 8.2.2 Precast concrete

- 8.2.3 Other concrete applications

- 8.3 Mortar & grouts

- 8.4 Precast elements

- 8.4.1 Blocks & bricks

- 8.4.2 Panels & slabs

- 8.4.3 Pipes & columns

- 8.4.4 Other precast elements

- 8.5 Pavements & overlays

- 8.6 Repair & rehabilitation

- 8.7 Waste encapsulation & immobilization

- 8.8 Other applications

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Building & construction

- 9.2.1 Residential

- 9.2.2 Commercial

- 9.2.3 Industrial

- 9.3 Infrastructure

- 9.3.1 Roads & bridges

- 9.3.2 Dams & water management

- 9.3.3 Airports & ports

- 9.3.4 Other infrastructure

- 9.4 Oil & gas

- 9.5 Mining

- 9.6 Marine & underwater construction

- 9.7 Nuclear & waste management

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Performance Attribute, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 High strength

- 10.3 Chemical resistance

- 10.4 Fire resistance

- 10.5 Low shrinkage

- 10.6 Rapid setting

- 10.7 Other performance attributes

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 Alchemy Geopolymer Solutions, LLC

- 12.2 Banah UK Ltd.

- 12.3 BASF SE

- 12.4 CEMEX S.A.B. de C.V.

- 12.5 Ceratech Inc.

- 12.6 Concrete Canvas Ltd.

- 12.7 Dow Chemical Company

- 12.8 GCP Applied Technologies Inc.

- 12.9 Geobeton Pty Ltd.

- 12.10 Geopolymer Products

- 12.11 Geopolymer Solutions, LLC

- 12.12 Halliburton

- 12.13 Imerys S.A.

- 12.14 Kiran Global Chems Limited

- 12.15 LafargeHolcim Ltd.

- 12.16 Metna Co.

- 12.17 Milliken Infrastructure Solutions, LLC

- 12.18 Nu-Core

- 12.19 PCI Augsburg GmbH

- 12.20 Pyromeral Systems

- 12.21 Reno Refractories, Inc.

- 12.22 Rocla Pty Limited

- 12.23 Schlumberger Limited

- 12.24 Sika AG

- 12.25 Siloxo Pty Ltd.

- 12.26 Tech-Crete Processors Ltd.

- 12.27 Uretek Worldwide

- 12.28 Wagners

- 12.29 Wollner GmbH

- 12.30 Zeobond Pty Ltd.