|

市場調査レポート

商品コード

1750283

発電所用重負荷ガスタービンの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Power Plants Heavy Duty Gas Turbine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 発電所用重負荷ガスタービンの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月08日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

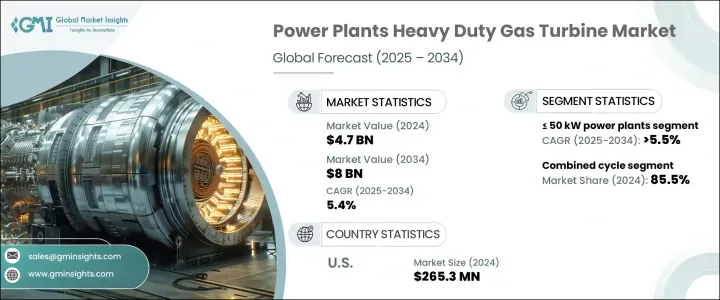

2024年の世界の発電所用重負荷ガスタービン市場規模は47億米ドルで、CAGR 5.4%で成長し2034年には80億米ドルに達すると推定されます。

信頼性の高いオンデマンドエネルギー源へのシフトが進行しているため、大手電力会社や公共機関はガスベースの発電への投資を増やしています。この市場は、急速な工業化と世界のエネルギー需要を背景に、ピーク負荷とベース負荷のエネルギー・ソリューションに対する需要の高まりとともに勢いを増しています。エネルギー安全保障への関心の高まりは、天然ガス探査と貿易活動の活発化と相まって、市場をさらに形成しています。さらに、各国がエネルギー・インフラの効率向上を目指す中、デジタル技術とスマート・グリッド・ソリューションの統合が採用を加速しています。低排出ガスと大規模プラントの資本支出削減の推進が、ガスタービン・ベースの発電への移行を後押ししています。

大型ガスタービンは、運転の柔軟性と環境コンプライアンスを維持しながら高出力を生み出す能力で支持されています。これらのタービンは、空気の圧縮、燃料の混合、点火という高度なプロセスを経て機能し、その結果、高圧ガスがタービンブレードを猛烈な速度で回転させ、驚くべき発電性能を発揮します。この業界は、特に最近導入された貿易関税により、アルミニウム、鉄鋼、特殊合金などの主要な投入材料のコストが上昇し、逆風に直面しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 47億米ドル |

| 予測金額 | 80億米ドル |

| CAGR | 5.4% |

50 kW未満の発電所向け大型ガスタービン分野は、分散型エネルギーシステムでの採用増加により、2034年までCAGR 5.5%以上で成長すると予測されます。これらのコンパクトなユニットは、信頼性の高い自家発電を必要とする産業や遠隔地の施設に不可欠であることが証明されています。その柔軟性、運用効率、コンパクトな設置面積は、グリッド接続が制限されていたり、一貫性がない分散型電力ネットワークに理想的です。産業施設が、二酸化炭素排出量を最小限に抑えながら、中断のない電力を確保する費用対効果の高い方法を模索する中、こうした低容量タービンの魅力はますます強まっています。

技術面では、ガスタービンと蒸気タービンを利用して同じ燃料源から最大限のエネルギーを引き出すコンバインドサイクルシステムの優れた効率性が原動力となり、コンバインドサイクル部門の2024年のシェアは85.5%に達しました。これらのシステムは、排出量を大幅に削減し、燃料使用量を最適化することで、環境目標や厳しい規制基準に適合しています。クリーンエネルギー発電へのシフトにより、電力会社や独立系発電事業者は従来の石炭発電所を段階的に廃止し、より持続可能な代替案として複合サイクルソリューションを採用するようになっています。

米国の大型ガスタービン市場の2024年の市場規模は2億6,530万米ドルで、信頼性が高くクリーンな電力に対する同国の需要加速を反映しています。急速な工業化、人工知能データセンターのようなエネルギー集約型部門の台頭、石炭から天然ガスへの広範な移行が、この成長の主な要因です。シェールガスの利用可能性が高まったことで、天然ガス大国としての米国の地位はさらに強化され、ガスタービン事業の安定したサプライチェーンが可能になりました。

市場の主要企業には、Wartsila、Siemens Energy、GE Vernova、Vericor、MAN Energy Solutions、Flex Energy Solutions、Nanjing Steam Turbine Motor(Group)、Solar Turbines、川崎重工業、Capstone Green Energy Holdings、Baker Hughes、三菱重工業、Doosan Enerbility、Rolls Royce、Bharat Heavy Electricals、Destinus Energy、Ansaldo Energia、Harbin Electricなどがあります。市場での存在感を高めるため、企業はいくつかの戦略に注力しています。これには、タービンの性能を最適化し、運転休止時間を短縮するデジタルアップグレードや遠隔監視ソリューションによるサービスポートフォリオの拡大が含まれます。各企業は、公共施設や産業施設に柔軟に導入できるよう、モジュール式タービン設計に投資しています。エネルギープロバイダーとの戦略的提携や長期供給契約は、市場での地位固めに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業の市場シェア分析

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 50kW未満

- 50kW~500kW以上

- 500kW~1MW

- 1MW~30MW以上

- 30MW~70MW以上

- 70MW~200MW以上

- 200MW以上

第6章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- オープンサイクル

- 複合サイクル

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- オランダ

- フィンランド

- ギリシャ

- デンマーク

- ルーマニア

- ポーランド

- スウェーデン

- アジア太平洋

- 中国

- オーストラリア

- 日本

- 韓国

- インドネシア

- タイ

- マレーシア

- バングラデシュ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- オマーン

- エジプト

- トルコ

- バーレーン

- イラク

- ヨルダン

- 南アフリカ

- ナイジェリア

- アルジェリア

- ケニア

- ガーナ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- ペルー

- チリ

第8章 企業プロファイル

- Ansaldo Energia

- Baker Hughes

- Bharat Heavy Electricals

- Capstone Green Energy Holdings

- Destinus Energy

- Doosan Enerbility

- Flex Energy Solutions

- GE Vernova

- Harbin Electric

- Kawasaki Heavy Industries

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Nanjing Steam Turbine Motor(Group)

- Rolls Royce

- Siemens Energy

- Solar Turbines

- Vericor

- Wartsila

The Global Power Plants Heavy Duty Gas Turbine Market was valued at USD 4.7 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 8 billion by 2034, driven by the ongoing shift toward reliable, on-demand energy sources is prompting major utilities and public sector bodies to increase investments in gas-based power generation. This market is gaining momentum with the rising demand for peak-load and base-load energy solutions, driven by rapid industrialization and global energy needs. The growing focus on energy security, combined with increasing natural gas exploration and trade activity, is further shaping the market. Additionally, as countries look to enhance the efficiency of their energy infrastructure, integrating digital technologies and smart grid solutions is accelerating adoption. The push for lower emissions and reduced capital expenditure on large-scale plants supports the transition toward gas turbine-based generation.

Heavy-duty gas turbines are favored for their ability to produce high power outputs while maintaining operational flexibility and environmental compliance. These turbines function through an advanced process of air compression, fuel mixing, and ignition, resulting in high-pressure gases that spin turbine blades at intense speeds, delivering remarkable power generation performance. The industry has faced some headwinds, particularly due to trade tariffs introduced recently, which raised the cost of key input materials such as aluminum, steel, and specialized alloys.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.7 Billion |

| Forecast Value | $8 Billion |

| CAGR | 5.4% |

The <= 50 kW power plants heavy-duty gas turbine segment is forecasted to grow at a CAGR of over 5.5% through 2034, driven by its increasing adoption in decentralized energy systems. These compact units are proving vital for industries and remote facilities that require reliable, on-site power generation. Their flexibility, operational efficiency, and compact footprint make them ideal for distributed power networks where grid connectivity is limited or inconsistent. As industrial facilities seek cost-effective ways to ensure uninterrupted power while minimizing carbon output, the appeal of these lower-capacity turbines continues to strengthen.

On the technology front, the combined cycle segment held 85.5% share in 2024, driven by the superior efficiency of combined cycle systems, which utilize gas and steam turbines to extract maximum energy from the same fuel source. These systems significantly cut emissions and optimize fuel usage, aligning with environmental goals and stringent regulatory standards. The shift toward clean energy generation prompts utilities and independent power producers to phase out conventional coal plants and adopt combined cycle solutions as a more sustainable alternative.

United States Heavy Duty Gas Turbine Market was valued at USD 265.3 million in 2024, reflecting the country's accelerating demand for reliable and clean electricity. Rapid industrialization, the rise of energy-intensive sectors like artificial intelligence data centers, and the widespread transition from coal to natural gas are key contributors to this growth. The increasing availability of shale gas has further strengthened the U.S. position as a natural gas powerhouse, enabling stable supply chains for gas turbine operations.

Leading companies in the market include Wartsila, Siemens Energy, GE Vernova, Vericor, MAN Energy Solutions, Flex Energy Solutions, Nanjing Steam Turbine Motor (Group), Solar Turbines, Kawasaki Heavy Industries, Capstone Green Energy Holdings, Baker Hughes, Mitsubishi Heavy Industries, Doosan Enerbility, Rolls Royce, Bharat Heavy Electricals, Destinus Energy, Ansaldo Energia, Harbin Electric, and others. To enhance market presence, companies are focusing on several strategies. These include expanding their service portfolios through digital upgrades and remote monitoring solutions, which optimize turbine performance and reduce operational downtime. Firms invest in modular turbine designs for flexible deployment across utility and industrial sites. Strategic collaborations with energy providers and long-term supply agreements are helping solidify market positions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiatives

- 4.4 Company market share analysis, 2024

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 50 kW

- 5.3 > 50 kW to 500 kW

- 5.4 > 500 kW to 1 MW

- 5.5 > 1 MW to 30 MW

- 5.6 > 30 MW to 70 MW

- 5.7 > 70 MW to 200 MW

- 5.8 > 200 MW

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 Open cycle

- 6.3 Combined cycle

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Russia

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.3.7 Finland

- 7.3.8 Greece

- 7.3.9 Denmark

- 7.3.10 Romania

- 7.3.11 Poland

- 7.3.12 Sweden

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Indonesia

- 7.4.6 Thailand

- 7.4.7 Malaysia

- 7.4.8 Bangladesh

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Kuwait

- 7.5.5 Oman

- 7.5.6 Egypt

- 7.5.7 Turkey

- 7.5.8 Bahrain

- 7.5.9 Iraq

- 7.5.10 Jordan

- 7.5.11 South Africa

- 7.5.12 Nigeria

- 7.5.13 Algeria

- 7.5.14 Kenya

- 7.5.15 Ghana

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Peru

- 7.6.4 Chile

Chapter 8 Company Profiles

- 8.1 Ansaldo Energia

- 8.2 Baker Hughes

- 8.3 Bharat Heavy Electricals

- 8.4 Capstone Green Energy Holdings

- 8.5 Destinus Energy

- 8.6 Doosan Enerbility

- 8.7 Flex Energy Solutions

- 8.8 GE Vernova

- 8.9 Harbin Electric

- 8.10 Kawasaki Heavy Industries

- 8.11 MAN Energy Solutions

- 8.12 Mitsubishi Heavy Industries

- 8.13 Nanjing Steam Turbine Motor (Group)

- 8.14 Rolls Royce

- 8.15 Siemens Energy

- 8.16 Solar Turbines

- 8.17 Vericor

- 8.18 Wartsilä