脳卒中治療薬市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Stroke Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750282

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

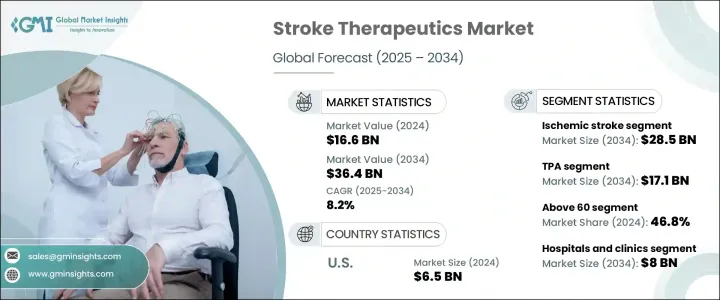

世界の脳卒中治療薬市場は、2024年には166億米ドルと評価され、肥満、高血圧、座りがちなライフスタイル、糖尿病などの慢性疾患などのリスク要因の蔓延の増加と相まって、高齢者人口の増加に後押しされ、CAGR 8.2%で成長し、2034年には364億米ドルに達すると推定されます。

高齢者層は特に脳卒中に罹患しやすいため、先進的な医薬品治療に対する需要が高まっています。同時に、公衆衛生意識の高まりや早期診断・予防に関する政府の取り組み強化により、治療薬の採用が加速しています。

製薬企業は研究開発に投資し、臨床転帰を改善するために設計された新規の生物製剤、遺伝子治療薬、標的薬に注力しています。個別化医療は、より正確で効果的な治療アプローチを可能にする重要な分野となりつつあります。脳卒中治療薬には、抗血小板薬や抗凝固薬から血栓溶解薬や神経保護薬に至るまで、医薬品が含まれます。虚血性脳卒中と出血性脳卒中の両方の予後を改善することを目的とした新たな治療薬が開発パイプラインに加わり、研究開発に対する多額の資金援助が開発パイプラインの拡充に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 166億米ドル |

| 予測金額 | 364億米ドル |

| CAGR | 8.2% |

虚血性脳卒中は、脳への血管が閉塞して起こるもので、治療薬市場を独占しています。この分野は2024年に131億米ドルを生み出し、2034年には285億米ドルに達し、CAGR 8.1%で成長すると予測されています。虚血性脳卒中が世界全体の症例の大半を占めることを考えると、この需要動向は引き続き堅調です。高コレステロール、心房細動、糖尿病など、脳卒中に寄与する疾患の有病率が上昇しているため、より効果的な治療法の必要性が高まっています。特に血栓溶解療法や抗血小板剤開発における薬剤の革新は、生存率や回復転帰の改善に役立っています。

年齢層別に見ると、2024年には60歳以上が46.8%と最大のシェアを占める。脳卒中のリスクは、血管の健康状態の低下や一般的な併存疾患により、加齢とともに著しく増加します。加齢は神経血管の反応性にも影響するため、高齢者は治療介入の重要な層となります。ヘルスケアインフラの継続的な改善と加齢に焦点を当てた健康への取り組みが、2034年まで同分野の成長を維持すると予想されます。

米国脳卒中治療薬2024年の市場規模は65億米ドルで、高度なヘルスケアシステム、高い研究開発集約度、強力な医薬品プレゼンスに支えられています。幹細胞治療やAIによる診断統合など、急速なイノベーションが米国のリーダーシップを強化。精密医療とデジタルヘルスプラットフォームへの注目の高まりにより、早期発見と治療効果の向上がさらに進んでいます。官民の強固な協力体制が、臨床試験とパイプライン開発の拡大に拍車をかけています。

Lupin、Pfizer、Boehringer Ingelheim、Sanofi、Genentech、Novartis、Bayer、AstraZeneca、第一三共、Johnson &Johnson Services、Cadrenal Therapeutics、Prestige Consumer Healthcare、Merck、Eisai、Bristol-Myers Squibbなどの主要企業は、積極的な成長戦略を採用しています。これには、臨床パイプラインの拡大、研究開発パートナーシップの形成、画期的新薬の規制当局による承認の追求、標的療法を提供するための個別化医療の探求などが含まれます。多くの企業がAIプラットフォームや生物製剤の革新に投資し、治療の提供と患者の転帰を最適化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 脳卒中発症例の増加

- 医薬品開発の進歩

- 意識の高まりと早期診断

- 脳卒中調査への投資と政府資金の増加

- 業界の潜在的リスク&課題

- 厳格な規制承認

- 副作用と安全性の懸念

- 促進要因

- 成長可能性分析

- 規制情勢

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:脳卒中タイプ別、2021年~2034年

- 主要動向

- 虚血性脳卒中

- 出血性脳卒中

- その他の脳卒中タイプ

第6章 市場推計・予測:薬剤クラス別、2021年~2034年

- 主要動向

- 組織プラスミノーゲン活性化因子(TPA)

- 抗血小板薬

- 抗凝固薬

- その他の薬剤クラス

第7章 市場推計・予測:年齢別、2021年~2034年

- 主要動向

- 40歳未満

- 41歳~59歳

- 60歳以上

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 外来手術センター(ASC)

- リハビリセンター

- 研究・学術機関

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AstraZeneca

- Bayer

- Boehringer Ingelheim

- Bristol-Myers Squibb(BMS)

- Cadrenal Therapeutics

- Daiichi Sankyo

- Eisai

- Genentech

- Johnson &Johnson Services

- Lupin

- Merck

- Novartis

- Pfizer

- Prestige Consumer Healthcare

- Sanofi

目次

The Global Stroke Therapeutics Market was valued at USD 16.6 billion in 2024 and is estimated to grow at a CAGR of 8.2% to reach USD 36.4 billion by 2034, fueled by the rising elderly population, coupled with increased prevalence of risk factors like obesity, hypertension, sedentary lifestyles, and chronic illnesses such as diabetes. An aging demographic is especially susceptible to stroke, leading to greater demand for advanced pharmaceutical treatments. At the same time, increased public health awareness and stronger government initiatives around early diagnosis and prevention are accelerating the adoption of therapeutics.

Pharmaceutical firms invest in research and development, focusing on novel biologics, gene therapies, and targeted drugs designed to improve clinical outcomes. Personalized medicine is becoming a key area of interest, allowing for more precise and effective treatment approaches. Stroke therapeutics includes medications, from antiplatelet agents and anticoagulants to thrombolytics and neuroprotective drugs. Substantial financial backing for R&D is helping expand the development pipeline, with new therapies aimed at improving outcomes for both ischemic and hemorrhagic stroke types.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.6 Billion |

| Forecast Value | $36.4 Billion |

| CAGR | 8.2% |

Ischemic stroke, which occurs when a blood vessel to the brain is blocked, dominates the therapeutic market. This segment generated USD 13.1 billion in 2024 and is forecasted to hit USD 28.5 billion by 2034, growing at a CAGR of 8.1%. Given that ischemic strokes account for the majority of total cases globally, this demand trajectory remains strong. The rising prevalence of contributing conditions like high cholesterol, atrial fibrillation, and diabetes continues to push the need for more effective treatments. Drug innovations, especially in thrombolytic therapy and antiplatelet development, are helping improve survival rates and recovery outcomes.

When segmented by age group, individuals aged 60 and above have the largest share at 46.8% in 2024. The risk of stroke significantly increases with age due to declining vascular health and common comorbidities. Aging also affects neurovascular responsiveness, making seniors a key demographic for therapeutic intervention. The ongoing improvement of healthcare infrastructure and age-focused health initiatives are expected to sustain segment growth through 2034.

United States Stroke Therapeutics Market was valued at USD 6.5 billion in 2024, supported by advanced healthcare systems, high R&D intensity, and strong pharmaceutical presence. Rapid innovations, including stem cell therapies and AI-based diagnostic integration, reinforce the country's leadership. The growing focus on precision medicine and digital health platforms is further enhancing early detection and improving treatment efficacy. Robust public and private sector collaboration is fueling the expansion of clinical trials and pipeline development.

Key players such as Lupin, Pfizer, Boehringer Ingelheim, Sanofi, Genentech, Novartis, Bayer, AstraZeneca, Daiichi Sankyo, Johnson & Johnson Services, Cadrenal Therapeutics, Prestige Consumer Healthcare, Merck, Eisai, and Bristol-Myers Squibb are adopting aggressive growth strategies. These include expanding clinical pipelines, forming R&D partnerships, pursuing regulatory approvals for breakthrough drugs, and exploring personalized medicine to deliver targeted therapies. Many invest in AI platforms and biologics innovation to optimize treatment delivery and patient outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising stroke incidence cases

- 3.2.1.2 Advancement in drug development

- 3.2.1.3 Growing awareness and early diagnosis

- 3.2.1.4 Rising investment in stroke research and government funding

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Strict regulatory approvals

- 3.2.2.2 Side effects and safety concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Stroke Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Ischemic stroke

- 5.3 Hemorrhagic stroke

- 5.4 Other stroke types

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Tissue plasminogen activators (TPA)

- 6.3 Antiplatelet agents

- 6.4 Anticoagulants

- 6.5 Other drug classes

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Below 40

- 7.3 41-59

- 7.4 above 60

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Ambulatory surgical centers (ASCs)

- 8.4 Rehabilitation centers

- 8.5 Research and academic institutions

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AstraZeneca

- 10.2 Bayer

- 10.3 Boehringer Ingelheim

- 10.4 Bristol-Myers Squibb (BMS)

- 10.5 Cadrenal Therapeutics

- 10.6 Daiichi Sankyo

- 10.7 Eisai

- 10.8 Genentech

- 10.9 Johnson & Johnson Services

- 10.10 Lupin

- 10.11 Merck

- 10.12 Novartis

- 10.13 Pfizer

- 10.14 Prestige Consumer Healthcare

- 10.15 Sanofi

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日