線維筋痛症治療市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)

Fibromyalgia Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750276

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

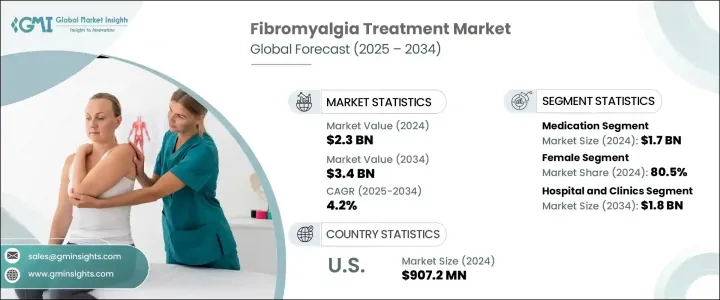

世界の線維筋痛症治療市場は、2024年には23億米ドルと評価され、神経化学的不均衡や中枢性感作を含む線維筋痛症の複雑な病態生理の理解が深まることにより、4.2%のCAGRで成長し、2034年には34億米ドルに達すると推定されています。

定量的な感覚検査や慢性疼痛症候群のバイオマーカーの開発など、診断方法の進歩により、早期かつ正確な診断が向上しています。機能的MRIやプロテオーム解析を含む技術の統合は、特定の疼痛経路を特定し、治療戦略を調整するのに役立つため、市場の成長を後押ししています。

さらに、人工知能(AI)を搭載したプラットフォームやデジタルヘルス技術を取り入れることで、症状の追跡と管理が強化され、より個別化された治療アプローチが可能になりました。神経調節やバイオフィードバックといった非侵襲的治療へのシフトは、ホリスティックな枠組みが受け入れられつつあることを示しています。製薬企業、学術機関、臨床医による業界を超えた協力体制が先進的な治療薬の開発に拍車をかけ、治療アプローチと治療結果の方向性を変えています。この市場には、慢性疼痛、疲労、線維筋痛症の関連症状の管理を目的とした、鎮痛薬や抗うつ薬などの薬物療法や代替療法を含む、薬物療法と非薬物療法が含まれます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 23億米ドル |

| 市場規模予測 | 34億米ドル |

| CAGR | 4.2% |

疼痛、疲労、その後の症状管理に関する患者の期待の高まりにより、薬物療法セグメントは2024年に17億米ドルを創出しました。薬理学的アプローチに対する需要が高まっていることが、薬物療法分野が市場を独占している理由です。主な薬剤クラス別には、抗うつ薬、抗けいれん薬、鎮痛薬などがあり、患者のQOL向上に貢献しています。このセグメントの成長を支えているのは、新薬やその改良品の発売であり、線維筋痛症に特化してFDAに承認された最初の薬剤のひとつであるプレガバリンなど、既存薬の販売承認の拡大でもあります。

男女別では、線維筋痛症治療市場は男性と女性に分けられます。女性セグメントは2024年に80.5%という大きな市場シェアを占めています。この疾患は女性に偏って発症するため、女性セグメントは市場シェアを表しています。米国国立生物工学情報センター(NCBI)が報告しているように、線維筋痛症候群は女性優位性が高く、症例の80%~96%を占めています。これらの違いは、ホルモンの要因、痛みの感じ方の違い、神経系の機能の違いなどに基づいて説明されています。

米国の線維筋痛症治療市場は、その質の高いヘルスケアシステム、高い疾患有病率、広範な製薬産業により、2024年には9億720万米ドルと評価されました。デュロキセチン、ミルナシプラン、プレガバリンなどのFDA承認薬が処方箋を独占しています。認知度向上プログラムや保険適用により、患者の治療意欲はさらに高まっています。新たな動向としては、診断のための遠隔医療や、より個別化された医療へのシフトが挙げられます。新たな治療アプローチのための臨床研究には、認知行動療法やライフスタイルの変化など、医薬品以外の選択肢も含まれます。

世界の線維筋痛症治療業界で事業を展開する主要企業には、アボット・ラボラトリーズ、アッヴィ、アムニール・ファーマシューティカルズ、アストラゼネカ、コロラド線維筋痛症センター、イーライリリー・アンド・カンパニー、ルパン、メイヨー・クリニック、ノバルティス、ファイザー、サン・ファーマシューティカルズ、テバ・ファーマシューティカルズ、ザ・ジェネラル・ホスピタル・コーポレーション、UTヘルス・オースティン、ヴィアトリス、ザイダス・ライフサイエンシズなどがあります。市場での足場を固めるため、線維筋痛症治療分野の企業は研究開発への積極的な投資を通じてイノベーションを重視しています。これには、患者の服薬アドヒアランスと治療効果を高めるための製剤化、投与レジメンの最適化、ドラッグデリバリー技術の向上などが含まれます。また、多くの大手企業は学術機関や研究機関と戦略的提携を結び、次世代治療の発見と商業化を加速させています。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 線維筋痛症の有病率の世界的な上昇

- 線維筋痛症の診断・治療オプションに関する意識の高まり

- 疼痛管理を目的とした医薬品療法の進歩

- 業界の潜在的リスクと課題

- 高度な線維筋痛症治療の高額な費用

- 線維筋痛症向けに特に承認された有効な薬剤の入手制約

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 将来の市場動向

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業別の市場シェア分析

- 主要企業の競合分析

- 競合ポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:治療の種類別(2021~2034年)

- 主要動向

- 薬剤

- 抗うつ薬

- 抗けいれん薬

- 鎮痛剤

- 筋弛緩剤

- その他の治療薬

- 治療

- 理学療法

- 作業療法

- その他の治療法

第6章 市場推計・予測:男女別(2021~2034年)

- 主要動向

- 男性

- 女性

第7章 市場推計・予測:最終用途別(2021~2034年)

- 主要動向

- 病院

- 専門クリニック

- その他の用途

第8章 市場推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- AbbVie

- Amneal Pharmaceuticals

- AstraZeneca

- Colorado Fibromyalgia Center

- Eli Lilly and Company

- Lupin

- Mayo Clinic

- Novartis

- Pfizer

- Sun Pharmaceutical

- Teva Pharmaceutical

- The General Hospital Corporation

- UT Health Austin

- Viatris

- Zydus Lifesciences

目次

The Global Fibromyalgia Treatment Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 3.4 billion by 2034, driven by a deeper understanding of fibromyalgia's complex pathophysiology, including neurochemical imbalances and central sensitization. Advances in diagnostic methods, such as quantitative sensory testing and the development of biomarkers for chronic pain syndromes, have improved early and accurate diagnosis. Integrating technology, including functional MRI and proteomic analysis, helps in identifying specific pain pathways and tailoring treatment strategies, thereby boosting market growth.

Additionally, incorporating artificial intelligence (AI)-powered platforms and digital health technologies has enhanced symptom tracking and management, enabling more personalized care approaches. The shift towards non-invasive treatments, such as neuromodulation and biofeedback, indicates a growing acceptance of holistic frameworks. Cross-industry collaboration among pharmaceutical companies, academic institutions, and clinical practitioners has catalyzed the development of advanced therapeutics, changing the course of treatment approaches and outcomes. The market encompasses pharmaceutical and non-pharmacological treatments aimed at managing chronic pain, fatigue, and associated symptoms of fibromyalgia, including medications like analgesics and antidepressants, as well as alternative therapies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 4.2% |

The medication segment generated USD 1.7 billion in 2024 due to increased patient expectations regarding pain, fatigue, and subsequent symptom management. Demand is rising for pharmacological approaches, which explains why the medication segment dominates the market. Key drug classes include antidepressants, anticonvulsants, and analgesic drugs that help patients enjoy a better quality of life. The growth in this segment is supported by the launch of new drugs and their reformulations, along with increased marketing authorizations of existing ones, such as pregabalin, one of the first FDA-approved drugs specifically for fibromyalgia.

Based on gender, the fibromyalgia treatment market is divided into male and female segments. The female segment accounted for a significant market share of 80.5% in 2024. The female segment represents a market share, as the condition disproportionately affects women. As reported by the National Center for Biotechnology Information (NCBI), fibromyalgia syndrome has a high female predominance, comprising 80%-96% of cases. These differences have been explained based on hormonal factors, greater pain perception, and variations in the functions of the nervous system.

U.S. Fibromyalgia Treatment Market was valued at USD 907.2 million in 2024 due to its quality healthcare system, high disease prevalence, and extensive pharmaceutical industry. FDA-approved drugs such as duloxetine, milnacipran, and pregabalin dominate the prescription landscape. Patients are further motivated to seek treatment due to awareness programs and insurance coverage. Emerging trends include telemedicine for diagnosis and a shift toward a more personalized approach to medicine. Clinical research for new therapy approaches includes non-pharmaceutical options such as cognitive behavioral therapy and lifestyle changes.

Major players operating in the Global Fibromyalgia Treatment Industry include Abbott Laboratories, AbbVie, Amneal Pharmaceuticals, AstraZeneca, Colorado Fibromyalgia Center, Eli Lilly and Company, Lupin, Mayo Clinic, Novartis, Pfizer, Sun Pharmaceutical, Teva Pharmaceutical, The General Hospital Corporation, UT Health Austin, Viatris, and Zydus Lifesciences. To strengthen their market foothold, companies in the fibromyalgia treatment sector are emphasizing innovation through robust investments in research and development. This includes advancing drug formulations, optimizing dosage regimens, and improving delivery technologies to increase patient adherence and therapeutic effectiveness. Many leading firms are also forming strategic alliances with academic institutions and research organizations to accelerate the discovery and commercialization of next-generation treatments.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of fibromyalgia globally

- 3.2.1.2 Rising awareness about fibromyalgia diagnosis and treatment options

- 3.2.1.3 Advances in pharmaceutical therapies targeting pain management

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced fibromyalgia treatments

- 3.2.2.2 Limited availability of effective medications specifically approved for fibromyalgia

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021-2034 ($ Mn)

- 5.1 Key trends

- 5.2 Medication

- 5.2.1 Antidepressants

- 5.2.2 Anticonvulsants

- 5.2.3 Analgesics

- 5.2.4 Muscle relaxants

- 5.2.5 Other medications

- 5.3 Therapy

- 5.3.1 Physical therapy

- 5.3.2 Occupational therapy

- 5.3.3 Other therapies

Chapter 6 Market Estimates and Forecast, By Gender, 2021-2034 ($ Mn)

- 6.1 Key trends

- 6.2 Male

- 6.3 Female

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AbbVie

- 9.3 Amneal Pharmaceuticals

- 9.4 AstraZeneca

- 9.5 Colorado Fibromyalgia Center

- 9.6 Eli Lilly and Company

- 9.7 Lupin

- 9.8 Mayo Clinic

- 9.9 Novartis

- 9.10 Pfizer

- 9.11 Sun Pharmaceutical

- 9.12 Teva Pharmaceutical

- 9.13 The General Hospital Corporation

- 9.14 UT Health Austin

- 9.15 Viatris

- 9.16 Zydus Lifesciences

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日