|

市場調査レポート

商品コード

1750275

ベビースナックの世界市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)Baby Snacks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ベビースナックの世界市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年05月07日

発行: Global Market Insights Inc.

ページ情報: 英文 263 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

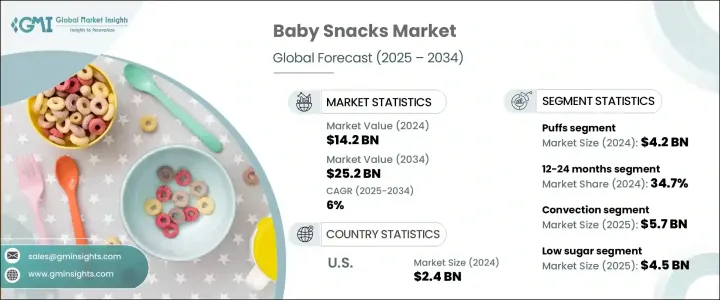

世界のベビースナックの市場規模は2024年に142億米ドルでしたが、栄養に対する保護者の意識の高まり(オーガニック・非遺伝子組み換え・アレルゲンフリー・タンパク質豊富な製品の人気拡大など)に後押しされ、6%のCAGRで成長し、2034年には252億米ドルに達すると予測されます。

利便性も重要な要素であり、親は子どもの発育のマイルストーンをサポートする、食べやすく持ち運び可能なスナックを求めています。市場では、人工添加物や保存料を使用しないクリーンラベル製品へのシフトが進んでいます。北米と欧州は、消費者の意識と購買力が高いことから市場をリードしています。しかし、アジア太平洋は、中国や日本のような国々における親の栄養意識の高まりに牽引され、これらの地域を凌駕すると予想されます。

デジタル小売の拡大は、これらの製品をこれまで以上に入手しやすくし、ベビースナック市場の状況を大きく変えています。eコマースは主要な流通チャネルとして台頭し、消費者直販モデルやサブスクリプション・ベースのサービスが現代の親たちの間で人気を集めています。これらの形態は、利便性を提供するだけでなく、カスタマイズされ、パーソナライズされたショッピング体験に対する需要の高まりにも対応しています。ミレニアル世代やZ世代の親が、品質に妥協することなく時間節約を求める中、オンライン・プラットフォームは、年齢や食事のニーズに合わせた健康志向のさまざまなベビースナックにシームレスにアクセスする方法を提供しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測期間 | 2025~2034年 |

| 当初の子女規模 | 142億米ドル |

| 市場規模の予測 | 252億米ドル |

| CAGR | 6% |

2024年、パフ入りスナック菓子分野は42億米ドルを占め、そのソフトで口溶けのよい食感が広く評価され、自力授乳に移行しつつある幼児に理想的です。メーカー各社は、栄養価の高い野菜を配合し、ナトリウム含有量を減らし、より冒険的な風味を試すようパフ製品を改良しています。その目的は、早期の味覚発達を促すと同時に、クリーンラベルで栄養価の高い食品を求める保護者の要望に応えることです。

ビスケットとクッキーの分野は2024年に35億米ドルと評価され、持続的な技術革新と栄養強化によって2034年には63億米ドルに達すると予測されます。各ブランドは、消化器系の健康と全体的な健康をサポートするために全粒穀物の使用を増やしながら、砂糖含有量を減らすことに注力しています。栄養価の向上に加え、製品デザインには人間工学に基づいた形状が採用され、成長期の乳幼児の手と目の協応や握力の向上を促しています。このような発達に役立つ機能は、栄養面だけでなく、スナック菓子をより幅広い幼児教育の一環とすることで付加価値を高めています。このような市場シフトの背景には、透明性、栄養、一口ごとの機能に対する消費者の期待の高まりがあります。

米国のベビースナックの2024年の市場規模は24億米ドルでした。米国市場の特徴は、積極的なイノベーションと消費者の細分化であり、親は便利で栄養価の高いスナックをますます求めるようになっています。FDAの監督により、製品開発プロセスは特に原材料とアレルギー表示に関する厳格なガイドラインを遵守しています。最近のガイドラインでは、製品中のアレルゲン暴露を制限することが奨励されています。マルチチャネル流通が普及しており、利便性と厳選された選択肢を重視するミレニアル世代の親たちの間でeコマース購読が顕著に伸びています。

世界のベビースナック市場における主要企業は、Nestle S.A.、Danone S.A.、Abbott Laboratories、The Hain Celestial Group、The Kraft Heinz Companyなどです。ベビースナック市場に参入している企業は、市場での地位を強化するためにいくつかの重要な戦略に注力しています。製品の革新が第一の焦点であり、各ブランドは進化する親子連れの嗜好に対応するため、新しい風味、食感、包装形態を開発しています。クリーンラベル製品に対する需要の高まりに対応し、オーガニックや天然成分を取り入れることに大きな重点が置かれています。環境意識の高い消費者にアピールするため、持続可能な包装ソリューションも採用されています。可処分所得の増加と都市化が新たな成長機会をもたらしているため、新興市場への進出は戦略的な動きです。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国(2021~2024年)

- 主要輸入国(2021~2024年)

注:上記の貿易統計は主要国のみに提供されます

- サプライヤーの情勢

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 親の健康意識の上昇により、オーガニックやアレルゲンフリーのベビーフードの需要が高まっています。

- 幼児期の栄養とベビースナックの発達上の利点についての認識が高まっています。

- 忙しい親のための、持ち運びやすく消費しやすいパッケージソリューションなど、利便性を重視した製品イノベーション

- 業界の潜在的リスク&課題

- ベビーフード製品には厳格な規制と安全基準があり、継続的な遵守が求められます

- 特にオーガニック製品やプレミアム製品の価格が高いため、一部の消費者にとっては購入が制限されます

- プライベートブランドや低価格ブランドとの熾烈な競合により、ブランドロイヤルティと市場シェアが脅かされています

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 製造・生産分析

- 製造プロセスの概要

- 原材料の調達・調合

- 加工・配合

- 押出・成形

- ベーキング/乾燥/フリーズドライ

- 品質管理・テスト

- 包装・保管

- 生産コスト分析

- 原材料費

- 人件費

- エネルギーコスト

- 梱包コスト

- 製造間接費

- コスト最適化戦略

- 製造施設分析

- 主要製造拠点

- 生産能力評価

- 施設拡張計画

- サプライチェーンの課題とソリューション

- 原材料調達

- サプライチェーン全体の品質管理

- 運輸・物流

- 在庫管理

- 品質管理と保証

- 品質基準と認証

- 試験方法と手順

- 品質管理システム

- 製造プロセスの概要

- 規制状況と基準

- 世界の規制枠組み

- 地域規制枠組み

- 北米

- FDA規制

- USDA基準

- 乳児用食品安全法

- 欧州

- 欧州食品安全機関(EFSA)

- 乳児用調製粉乳およびフォローアップ調製粉乳に関するEU指令

- 国別の規制

- アジア太平洋

- 中国食品薬品監督管理局

- 日本の食品衛生法

- その他の地域規制

- 世界のその他の地域

- 北米

- 食品安全基準と認証

- Haccp認証

- ISO 22000

- 食品安全のためのBRC世界スタンダード

- IFS食品基準

- ラベル・包装規制

- 成分開示要件

- 栄養成分表示

- アレルゲン情報

- 健康と栄養に関する主張

- 汚染物質および重金属規制

- 鉛の制限

- ヒ素の制限

- カドミウムと水銀の規制

- 農薬残留基準値

- コンプライアンスの課題と戦略

- 将来の規制動向とその影響

- 環境・社会・ガバナンス(ESG)分析

- 環境影響評価

- カーボンフットプリント分析

- 水の使用と管理

- 廃棄物の発生と管理

- 持続可能な調達慣行

- 社会的責任の実践

- 労働慣行と労働条件

- コミュニティの関与と支援

- 消費者の健康と栄養

- 倫理的なマーケティング慣行

- ガバナンスと倫理的配慮

- コーポレートガバナンス構造

- 倫理的なサプライチェーン管理

- 透明性と報告

- 汚職防止およびコンプライアンス対策

- 主要企業のESG実績のベンチマーク

- ESGリスク評価と軽減戦略

- ベビースナック業界における今後のESG動向

- 環境影響評価

- 消費者行動と市場動向の分析

- 消費者の嗜好と購買パターン

- 親の意思決定要因

- ブランドロイヤルティと乗り換え行動

- 価格感度分析

- 小児科医の推奨の影響

- 消費者の人口統計分析

- 年齢層分析

- 所得水準分析

- 地理的分布

- ライフスタイルと心理的セグメンテーション

- ベビースナックに対する消費者の認識

- 栄養価の認識

- 安全性と品質の認識

- 利便性

- 価格に見合った価値の認識

- 新たな消費者動向

- クリーンラベルの需要

- オーガニック・天然製品の人気

- アレルギーフリーおよび特別な食事要件

- 持続可能で倫理的な消費

- DX (デジタルトランスフォーメーション) が消費者エンゲージメントに与える影響

- 消費者フィードバック分析とその影響

- 消費者の嗜好と購買パターン

- 価格分析と経済的要因

- 価格動向分析

- 歴史的価格動向

- 現在の価格シナリオ

- 価格予測

- 価格に影響を与える要因

- 原材料費

- 生産・加工コスト

- 包装・ラベリング費用

- 流通・物流コスト

- 販売・促進費用

- 製品セグメント全体の価格戦略

- プレミアム製品とエコノミー製品

- オーガニック製品と従来型製品

- プライベートブランド製品とブランド製品

- 地域別の価格変動とその要因

- 価格と価値の関係分析

- 市場に影響を与える経済指標

- GDP成長率と消費者支出

- インフレと通貨変動

- 雇用率と可処分所得

- 出生率と人口動態の変化

- 価格動向分析

- 技術情勢とイノベーション分析

- ベビースナックの現在の技術動向

- 新興技術とその潜在的な影響

- 高度な処理技術

- 新しい保存方法

- スマートパッケージングソリューション

- デジタルサプライチェーン管理

- 製品イノベーションの動向

- クリーンラベル処方

- 植物食・ビーガンのオプション

- 機能性成分とスーパーフード

- 食感と感覚の革新

- 味と材料の革新

- 国際的・エスニック味覚プロファイル

- 高級オーガニック原料

- 砂糖と塩を減らした処方

- 天然保存料・添加物

- パッケージングの革新

- 持続可能な包装材料

- 賞味期限を延長したパッケージ

- 便利で分量をコントロールできるパッケージ

- スマートでアクティブなパッケージ

- 研究開発活動とイノベーションハブ

- 各地域の技術導入動向

- 将来の技術ロードマップ(2025~2033年)

- マーケティング戦略とブランド分析

- 現在のマーケティング情勢

- ブランドポジショニング戦略

- 標的顧客の内訳

- メッセージングと価値提案

- チャネル固有の戦略

- デジタルマーケティング戦略

- ソーシャルメディアマーケティング

- コンテンツマーケティング

- インフルエンサーとのパートナーシップ

- メールマーケティング

- モバイルマーケティング

- 従来のマーケティング手法

- 店頭プロモーション

- 印刷広告

- テレビとラジオ

- ダイレクトマーケティング

- 主要企業のブランド分析

- ブランドエクイティ評価

- ブランドの認識と認知度

- ブランドロイヤルティと顧客維持

- マーケティングツールとしてのパッケージ

- デザイン要素と視覚的な魅力

- 情報通信

- ブランドアイデンティティの強化

- 成功したマーケティングのケーススタディ

- 将来のマーケティング動向と戦略

- 現在のマーケティング情勢

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品種類別(2021~2034年)

- 主要動向

- パフ

- ビスケット・クッキー

- フルーツベースのスナック

- ヨーグルトドロップとフリーズドライスナック

- 野菜ベースのスナック

- 歯固めビスケットとラスク

- その他の種類のスナック

第6章 市場推計・予測:年齢別(2021~2034年)

- 主要動向

- 6~9ヶ月

- 9~12ヶ月

- 12~24ヶ月

- 24ヶ月以上

第7章 市場推計・予測:食材別(2021~2034年)

- 主要動向

- オーガニック

- 従来型

- 非遺伝子組み換え

- グルテンフリー

- アレルゲンフリー

第8章 市場推計・予測:栄養成分表示別(2021~2034年)

- 主要動向

- 高タンパク質

- 低糖

- 全粒穀物

- スーパーフード強化型

第9章 市場推計・予測:流通チャネル別(2021~2034年)

- 主要動向

- スーパーマーケット・ハイパーマーケット

- コンビニエンスストア・ドラッグストア

- ベビー用品専門店

- オンライン小売

- 消費者直販

- その他

第10章 市場推計・予測:販売チャネル別(2021~2034年)

- 主要動向

- B2B

- B2C

第11章 市場推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第12章 企業プロファイル

- Abbott Laboratories

- Amara Organic Foods

- Danone S.A.(Happy Baby Organics)

- Ella's Kitchen

- Hain Celestial Group(Earth's Best)

- Hero Group(Beech-Nut)

- Kewpie Corporation

- Little Bellies

- Little Freddie

- Nestle S.A.(Gerber)

- Plum Organics(Campbell Soup Company)

- Serenity Kids

- Sprout Foods、Inc.

- The Kraft Heinz Company

The Global Baby Snacks Market was valued at USD 14.2 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 25.2 billion by 2034, driven by increasing parental awareness of nutrition, with a preference for organic, non-GMO, allergen-free, and protein-rich products. Convenience is also a significant factor, with parents seeking easy-to-feed, portable snacks that support their children's developmental milestones. The market is experiencing a shift toward clean-label products, which are free from artificial additives and preservatives. North America and Europe lead the market due to high consumer awareness and purchasing power. However, the Asia Pacific region is expected to outpace these regions, driven by rising parental nutrition consciousness in countries like China and Japan.

The expansion of digital retail has significantly reshaped the baby snacks landscape, making these products more accessible than ever before. E-commerce has emerged as a key distribution channel, with direct-to-consumer models and subscription-based services gaining traction among modern parents. These formats not only offer convenience but also cater to the growing demand for curated and personalized shopping experiences. As millennial and Gen Z parents seek time-saving solutions without compromising on quality, online platforms provide a seamless way to access a variety of health-conscious baby snacks tailored to age and dietary needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.2 Billion |

| Forecast Value | $25.2 Billion |

| CAGR | 6% |

In 2024, the puffed snacks segment accounted for USD 4.2 billion, widely appreciated for their soft, melt-in-the-mouth texture, making them ideal for toddlers transitioning to self-feeding. Manufacturers are reformulating puff products to include nutrient-dense vegetables, reduce sodium content, and experiment with more adventurous flavor profiles. The goal is to encourage early palate development while aligning with parents' desire for clean-label, nutrient-rich foods.

The biscuits and cookies segment was valued at USD 3.5 billion in 2024 and is projected to reach USD 6.3 billion by 2034, driven by sustained innovation and nutritional enhancements. Brands are focusing on lowering sugar content while increasing the use of whole grains to support digestive health and overall wellness. In addition to nutritional upgrades, product design now includes ergonomic shapes that promote better hand-eye coordination and grip strength in growing infants. These developmental features add value beyond nutrition, making the snacks part of a broader early-learning journey. Altogether, these market shifts are driven by evolving consumer expectations for transparency, nutrition, and function in every bite.

U.S. Baby Snacks Market generated USD 2.4 billion in 2024. The U.S. market is characterized by aggressive innovation and consumer segmentation, with parents increasingly seeking both convenient and nutritious snacks. The FDA's oversight ensures product development processes adhere to strict guidelines, particularly concerning ingredients and allergy assertions. Recent guidelines have encouraged the restriction of allergen exposure in products. Multi-channel distribution is prevalent, with notable growth in e-commerce subscriptions among millennial parents who value convenience and curated choices.

Key players in the Global Baby Snacks Market include Nestle S.A., Danone S.A., Abbott Laboratories, The Hain Celestial Group, and The Kraft Heinz Company. Companies in the baby snacks market are focusing on several key strategies to strengthen their market position. Product innovation is a primary focus, with brands developing new flavors, textures, and packaging formats to meet the evolving preferences of parents and children. There is a significant emphasis on incorporating organic and natural ingredients, catering to the growing demand for clean-label products. Sustainable packaging solutions are also being adopted to appeal to environmentally conscious consumers. Expansion into emerging markets is a strategic move, as rising disposable incomes and urbanization present new growth opportunities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Base estimates and calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major importing countries, 2021-2024 (Kilo Tons)

Note: the above trade statistics will be provided for key countries only

- 3.4 Supplier landscape

- 3.5 Key news and initiatives

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for organic and allergen-free baby food options due to growing health-consciousness among parents.

- 3.6.1.2 Rising awareness about early childhood nutrition and developmental benefits of baby snacks.

- 3.6.1.3 Convenience-focused product innovations, such as easy-to-consume, on-the-go packaging solutions for busy parents.

- 3.6.2 Industry pitfalls and challenges

- 3.6.2.1 Stringent regulations and safety standards for baby food products, requiring continuous compliance.

- 3.6.2.2 High product pricing, especially for organic and premium options, limiting affordability for some consumers.

- 3.6.2.3 Intense competition from private label and budget-friendly brands, challenging brand loyalty and market share.

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Manufacturing and Production Analysis

- 3.10.1 Manufacturing process overview

- 3.10.1.1 Raw material procurement and preparation

- 3.10.1.2 Processing and formulation

- 3.10.1.3 Extrusion and shaping

- 3.10.1.4 Baking/drying/freeze-drying

- 3.10.1.5 Quality control and testing

- 3.10.1.6 Packaging and storage

- 3.10.2 Production cost analysis

- 3.10.2.1 Raw material costs

- 3.10.2.2 Labor costs

- 3.10.2.3 Energy costs

- 3.10.2.4 Packaging costs

- 3.10.2.5 Manufacturing overheads

- 3.10.2.6 Cost optimization strategies

- 3.10.3 Manufacturing facilities analysis

- 3.10.3.1 Key manufacturing locations

- 3.10.3.2 Production capacity assessment

- 3.10.3.3 Facility expansion plans

- 3.10.4 Supply chain challenges and solutions

- 3.10.4.1 Raw material sourcing

- 3.10.4.2 Quality control throughout supply chain

- 3.10.4.3 Transportation and logistics

- 3.10.4.4 Inventory management

- 3.10.5 Quality control and assurance

- 3.10.5.1 Quality standards and certifications

- 3.10.5.2 Testing methods and procedures

- 3.10.5.3 Quality management systems

- 3.10.1 Manufacturing process overview

- 3.11 Regulatory landscape and standards

- 3.11.1 Global regulatory framework

- 3.11.2 Regional regulatory frameworks

- 3.11.2.1 North america

- 3.11.2.1.1 Fda regulations

- 3.11.2.1.2 Usda standards

- 3.11.2.1.3 Baby food safety act

- 3.11.2.2 Europe

- 3.11.2.2.1 European food safety authority (efsa)

- 3.11.2.2.2 Eu directive on infant formula and follow-on formula

- 3.11.2.2.3 Country-specific regulations

- 3.11.2.3 Asia-pacific

- 3.11.2.3.1 China food and drug administration

- 3.11.2.3.2 Japan food sanitation law

- 3.11.2.3.3 Other regional regulations

- 3.11.2.4 Rest of the world

- 3.11.2.1 North america

- 3.11.3 Food safety standards and certifications

- 3.11.3.1 Haccp certification

- 3.11.3.2 Iso 22000

- 3.11.3.3 Brc global standard for food safety

- 3.11.3.4 Ifs food standard

- 3.11.4 Labeling and packaging regulations

- 3.11.4.1 Ingredient disclosure requirements

- 3.11.4.2 Nutritional labeling

- 3.11.4.3 Allergen information

- 3.11.4.4 Health and nutrition claims

- 3.11.5 Contaminant and heavy metal regulations

- 3.11.5.1 Lead limits

- 3.11.5.2 Arsenic limits

- 3.11.5.3 Cadmium and mercury regulations

- 3.11.5.4 Pesticide residue limits

- 3.11.6 Compliance challenges and strategies

- 3.11.7 Future regulatory trends and their implications

- 3.12 Environmental, social, and governance (esg) analysis

- 3.12.1 Environmental impact assessment

- 3.12.1.1 Carbon footprint analysis

- 3.12.1.2 Water usage and management

- 3.12.1.3 Waste generation and management

- 3.12.1.4 Sustainable sourcing practices

- 3.12.2 Social responsibility practices

- 3.12.2.1 Labor practices and working conditions

- 3.12.2.2 Community engagement and support

- 3.12.2.3 Consumer health and nutrition

- 3.12.2.4 Ethical marketing practices

- 3.12.3 Governance and ethical considerations

- 3.12.3.1 Corporate governance structures

- 3.12.3.2 Ethical supply chain management

- 3.12.3.3 Transparency and reporting

- 3.12.3.4 Anti-corruption and compliance measures

- 3.12.4 Esg performance benchmarking of key players

- 3.12.5 Esg risk assessment and mitigation strategies

- 3.12.6 Future esg trends in the baby snacks industry

- 3.12.1 Environmental impact assessment

- 3.13 Consumer behavior and market trends analysis

- 3.13.1 Consumer preferences and purchasing patterns

- 3.13.1.1 Parental decision-making factors

- 3.13.1.2 Brand loyalty and switching behavior

- 3.13.1.3 Price sensitivity analysis

- 3.13.1.4 Influence of pediatrician recommendations

- 3.13.2 Demographic analysis of consumers

- 3.13.2.1 Age group analysis

- 3.13.2.2 Income level analysis

- 3.13.2.3 Geographic distribution

- 3.13.2.4 Lifestyle and psychographic segmentation

- 3.13.3 Consumer perception of baby snacks

- 3.13.3.1 Nutritional value perception

- 3.13.3.2 Safety and quality perception

- 3.13.3.3 Convenience factor

- 3.13.3.4 Value for money perception

- 3.13.4 Emerging consumer trends

- 3.13.4.1 Clean label demand

- 3.13.4.2 Organic and natural preferences

- 3.13.4.3 Allergen-free and special diet requirements

- 3.13.4.4 Sustainable and ethical consumption

- 3.13.5 Impact of digital transformation on consumer engagement

- 3.13.6 Consumer feedback analysis and implications

- 3.13.1 Consumer preferences and purchasing patterns

- 3.14 Pricing analysis and economic factors

- 3.14.1 Pricing trends analysis

- 3.14.1.1 Historical price trends

- 3.14.1.2 Current pricing scenario

- 3.14.1.3 Price forecast

- 3.14.2 Factors affecting pricing

- 3.14.2.1 Raw material costs

- 3.14.2.2 Production and processing costs

- 3.14.2.3 Packaging and labeling costs

- 3.14.2.4 Distribution and logistics costs

- 3.14.2.5 Marketing and promotion costs

- 3.14.3 Pricing strategies across product segments

- 3.14.3.1 Premium vs. Economy products

- 3.14.3.2 Organic vs. Conventional products

- 3.14.3.3 Private label vs. Branded products

- 3.14.4 Regional price variations and factors

- 3.14.5 Price-value relationship analysis

- 3.14.6 Economic indicators impacting the market

- 3.14.6.1 Gdp growth and consumer spending

- 3.14.6.2 Inflation and currency fluctuations

- 3.14.6.3 Employment rates and disposable income

- 3.14.6.4 Birth rates and demographic shifts

- 3.14.1 Pricing trends analysis

- 3.15 Technological landscape and innovation analysis

- 3.15.1 Current technological trends in baby snacks

- 3.15.2 Emerging technologies and their potential impact

- 3.15.2.1 Advanced processing technologies

- 3.15.2.2 Novel preservation methods

- 3.15.2.3 Smart packaging solutions

- 3.15.2.4 Digital supply chain management

- 3.15.3 Product innovation trends

- 3.15.3.1 Clean label formulations

- 3.15.3.2 Plant-based and vegan options

- 3.15.3.3 Functional ingredients and superfoods

- 3.15.3.4 Texture and sensory innovations

- 3.15.4 Flavor and ingredient innovations

- 3.15.4.1 Global and ethnic flavor profiles

- 3.15.4.2 Premium and organic ingredients

- 3.15.4.3 Reduced sugar and salt formulations

- 3.15.4.4 Natural preservatives and additives

- 3.15.5 Packaging innovations

- 3.15.5.1 Sustainable packaging materials

- 3.15.5.2 Extended shelf-life packaging

- 3.15.5.3 Convenient and portion-controlled packaging

- 3.15.5.4 Smart and active packaging

- 3.15.6 R&d activities and innovation hubs

- 3.15.7 Technology adoption trends across regions

- 3.15.8 Future technology roadmap (2025-2033)

- 3.16 Marketing strategies and brand analysis

- 3.16.1 Current marketing landscape

- 3.16.1.1 Brand positioning strategies

- 3.16.1.2 Target audience segmentation

- 3.16.1.3 Messaging and value propositions

- 3.16.1.4 Channel-specific strategies

- 3.16.2 Digital marketing strategies

- 3.16.2.1 Social media marketing

- 3.16.2.2 Content marketing

- 3.16.2.3 Influencer partnerships

- 3.16.2.4 Email marketing

- 3.16.2.5 Mobile marketing

- 3.16.3 Traditional marketing approaches

- 3.16.3.1 In-store promotions

- 3.16.3.2 Print advertising

- 3.16.3.3 Television and radio

- 3.16.3.4 Direct marketing

- 3.16.4 Brand analysis of key players

- 3.16.4.1 Brand equity assessment

- 3.16.4.2 Brand perception and awareness

- 3.16.4.3 Brand loyalty and customer retention

- 3.16.5 Packaging as a marketing tool

- 3.16.5.1 Design elements and visual appeal

- 3.16.5.2 Information communication

- 3.16.5.3 Brand identity reinforcement

- 3.16.6 Successful marketing case studies

- 3.16.7 Future marketing trends and strategies

- 3.16.1 Current marketing landscape

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Puffs

- 5.3 Biscuits and cookies

- 5.4 Fruit-based snacks

- 5.5 Yogurt drops and freeze-dried snacks

- 5.6 Vegetable-based snacks

- 5.7 Teething biscuits and rusks

- 5.8 Other snack types

Chapter 6 Market Estimates and Forecast, By Age Group 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 6-9 Months

- 6.3 9-12 Months

- 6.4 12-24 Months

- 6.5 Above 24 Months

Chapter 7 Market Estimates and Forecast, By Ingredient Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Organic

- 7.3 Conventional

- 7.4 Non-GMO

- 7.5 Gluten-free

- 7.6 Allergen-free

Chapter 8 Market Estimates and Forecast, By Nutritional Content, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 High protein

- 8.3 Low sugar

- 8.4 Whole grain

- 8.5 Superfood-enriched

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Supermarkets and hypermarkets

- 9.3 Convenience stores and drugstores

- 9.4 Specialty baby stores

- 9.5 Online retail

- 9.6 Direct-to-consumer

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Sales Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 B2B

- 10.3 B2C

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Abbott Laboratories

- 12.2 Amara Organic Foods

- 12.3 Danone S.A. (Happy Baby Organics)

- 12.4 Ella's Kitchen

- 12.5 Hain Celestial Group (Earth's Best)

- 12.6 Hero Group (Beech-Nut)

- 12.7 Kewpie Corporation

- 12.8 Little Bellies

- 12.9 Little Freddie

- 12.10 Nestle S.A. (Gerber)

- 12.11 Plum Organics (Campbell Soup Company)

- 12.12 Serenity Kids

- 12.13 Sprout Foods, Inc.

- 12.14 The Kraft Heinz Company